CB is one of the world’s largest listed insurance groups, headquartered in Switzerland with global operations across property & casualty, accident & health and life insurance. It serves both commercial and consumer clients across more than 50 countries, with a strong skew to higher-quality commercial and specialty lines. With a market cap of the $US127bn, Chubb is ~6 times larger than QBE.

This is a high-quality operator, consistently delivering industry-leading underwriting margins. The group’s ability to price risk, exit unattractive segments and maintain discipline through the cycle has seen it produce one of the lowest combined ratios in global insurance, insulating earnings during periods of elevated catastrophe and claims inflation. We suspect this is why Berkshire Hathaway owns 8% of the company (worth around $US10.2bn) while GQG Partners also own nearly 3% (worth around $US3.5bn).

NB: A combined ratio is the Loss Ratio + Expense ratio. The way to interpret that number is: Below 100% = Underwriting profit, above 100% = Underwriting loss.

Chubb had a combined ratio (2025) of 81.2%, indicating strong underwriting profitability (meaning the company paid out about $81.20 in claims and expenses for every $100 of premiums earned).

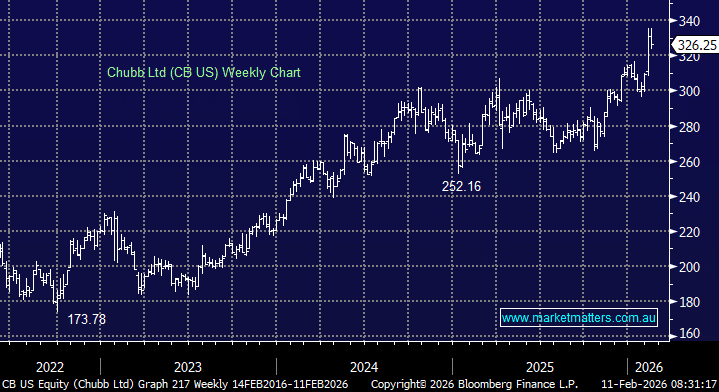

FY25 results (out last week) again highlighted ongoing strength, with revenue of ~$US52bn and strong growth in operating income driven by premium increases and rising investment income. Earnings (EPS) of $7.52 beat the consensus of $6.77, and higher interest rates continue to flow through the portfolio as maturing bonds are reinvested at materially higher yields, providing a medium-term tailwind even if US rates fall further. Management was positive about growth in 2026 across geographies and product lines, targeting double-digit EPS growth (vs. consensus 10%) along with double-digit tangible book value growth.

Unlike many insurers, Chubb is profitable across the cycle, generates excess capital and returns it consistently to shareholders via dividends and buybacks (they bought back $1.0bn in 2025). The balance sheet remains conservative, with ample flexibility to absorb large loss events without compromising capital returns.

Valuation remains reasonable for a business of this quality, trading around ~12x forward earnings and ~1.7x book. That represents a premium to the US sector, but one we think is justified given earnings stability, underwriting consistency and capital discipline.

- We see Chubb as a lower beta (0.45) core defensive holding within global equities – less exciting than growth stocks, but highly effective at preserving and steadily growing capital through uncertain markets. The recent purchase of Chubb is to broaden the earnings base of the Portfolio, adding some lower beta, defensive positioning to complement the portfolio’s growth skew at a time when equities have run hot.