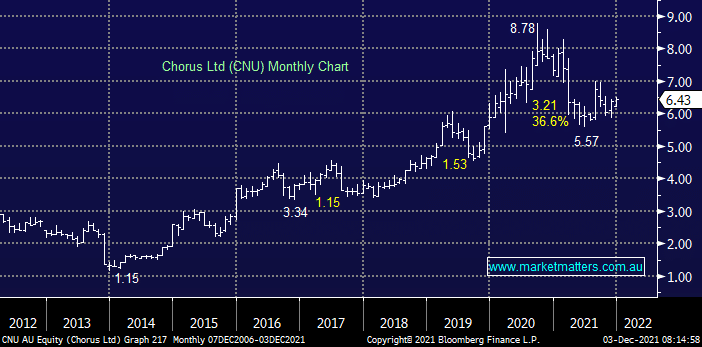

NZ based fixed line infrastructure business CNU has struggled over the last 12-months, the stocks 36% decline now has it forecast to yield 4.8% which is clearly attractive but further capital losses should not be discounted. The company has experienced a drop in revenue due to weaker market conditions plus increased competition from other fibre and wireless networks – not a great combination. The $6 area seems about fair value for CNU but we see far better opportunities elsewhere.

MM is neutral CNU

Add To Hit List