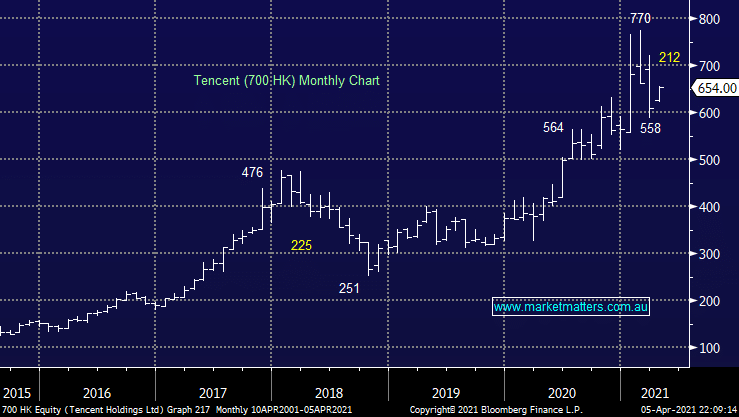

A confluence of factors sent Asia’s largest technology company down nearly 30% in 2021 making it one of the poorest performers on a global scale. The Hong Kong based goliath counts micro messaging & purchasing ap WeChat as a key asset which has more than 1.2bn users and processes a similar number of daily transactions.

After the recent correction, Tencent trades on an Est P/E of ~34x which is not onerous given it’s delivered close to 30% pa earnings growth over the past 5 years.

While this is clearly a volatile stock, MM views this pullback as one to buy.

MM is bullish Tencent (700 HK)

Add To Hit List