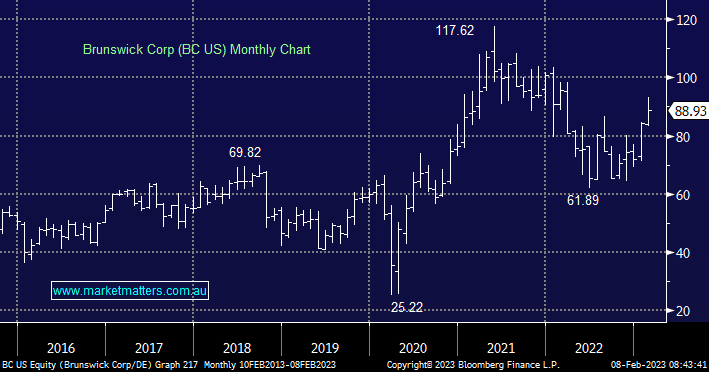

The world’s largest consumer marine company behind brands such as Mercury, Boston Whaler & Sea Ray, released FY22 results during the week and the share price reacted favourably, up 6.78% since last week’s portfolio report. This $US6.5bn company reported FY22 sales of $US6.8bn, growth of 16.5% on FY21 and underlying operating earnings of $1,048bn, up 18.3% for the year. While they were coming off a lower base and their guidance for FY23 is more subdued, (sales $US6.8-$US7.2bn) they have done an exceptional job of managing the complexities of supply chains, inflation, and consumer markets, while they seem well-positioned for the year ahead.

Trading on just 8.7x consensus earnings, there is not a lot of upside captured in this multiple. While there is clearly uncertainty around what discretionary spending will be in the year ahead, and the wider than normal guidance provided by the company is reflective of that, the conference call following their results had an optimistic tone, particularly in their outlook for higher-cost fibreglass boats (relative to lower cost aluminium boats), while the growth in larger outboard engines is exciting – you need only look around the bays in Sydney Harbour to see the huge shift in preferred propulsion for larger vessels with 2,3,4 and sometimes 5 Mercury outboards adorning the transom.