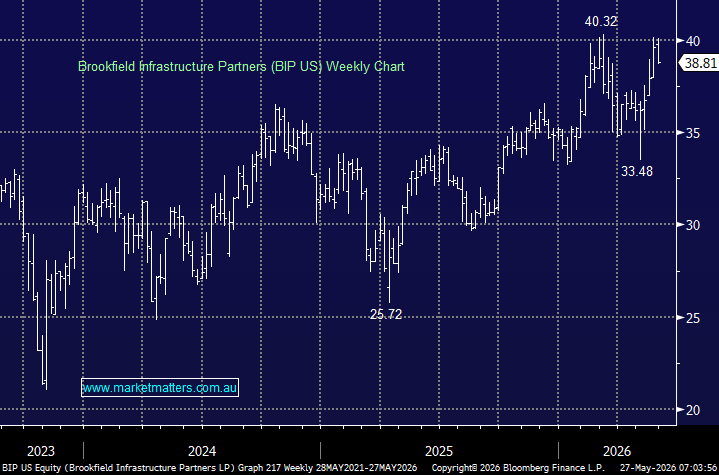

We are increasingly positive on infrastructure as an asset class, and Brookfield Infrastructure Partners (BIP) is one of the highest-quality global operators in the space.

BIP owns and operates a diversified portfolio of essential infrastructure assets across utilities, transport, midstream energy and data infrastructure. These include assets such as electricity transmission, regulated utilities, gas networks, toll roads, rail, ports, pipelines, telecom towers and data centres – a pure-play global owner and operator of infrastructure assets that generate stable cash flows, underpinned by contractual and regulatory frameworks. That is exactly the type of exposure we want more of in portfolios.

The appeal of infrastructure is that it can provide a different return profile to traditional equities. Many assets have high barriers to entry, long useful lives, essential-service characteristics and revenues linked to inflation, regulation or long-term contracts. In an environment where inflation may remain structurally higher than the pre-COVID period, and where equity markets are becoming more concentrated in technology, infrastructure can provide useful diversification.

Brookfield is a standout operator in this area. The broader Brookfield ecosystem gives BIP significant advantages, including deal flow, operational expertise, access to capital, global relationships and credibility with institutional investors. Brookfield Asset Management sits at the centre of the broader Brookfield ecosystem, managing listed affiliates including Brookfield Infrastructure, Brookfield Renewable and Brookfield Business Partners, which supports scale and fundraising, though it also adds structural complexity.

This is an important point. BIP is not just a passive owner of infrastructure assets. It is part of a much larger global asset management machine with deep experience in buying, improving and recycling assets. Brookfield’s broader infrastructure platform has over US$255bn in assets under management, giving it a scale advantage that few listed infrastructure investors can match.

- The recent operating performance has been solid. In the March quarter, BIP reported funds from operations of US$709m, up 10% on the prior year. Growth was supported by a stronger base business performance, with the data and midstream segments notable contributors.

The long-term thematic appeal is also clear. Infrastructure sits at the intersection of several major investment trends: electrification, energy security, digitalisation, AI-related data demand, supply chain reconfiguration and decarbonisation. BIP has exposure to many of these themes, but through hard assets rather than early-stage technology risk.

Consensus is very positive on the stock, with around 80% of analysts rating the stock a Buy, with a 12-month consensus target price of ~US$44, implying 11% upside, before distributions. The stock has performed well, with a last-twelve-month return of about 28%.

- The income profile is attractive, but not the only reason to own it. BIP offers a distribution yield of around 4.5–5%, with consensus expecting distributions to continue growing over the coming years, with revenue set to rise from around US$16.9bn in FY26 to US$27.5bn by FY28, while EBITDA is expected to increase from around US$4.7bn to US$5.6bn over the same period. However, the issue is valuation.

BIP is a high-quality business, but it is not obviously cheap, trading around 25x FY26 EV/EBITDA, falling to roughly 21x by FY28. That is not excessive for a premium infrastructure operator if growth is delivered, but it does leave less margin for error. Infrastructure assets are long-duration in nature, which means valuations can be sensitive to bond yields and the cost of capital.

There is also complexity to consider. Brookfield’s model relies on acquiring assets, improving returns, recycling capital and using scale to access opportunities that others cannot. That has created significant value over time, but it also means investors need to be comfortable with leverage, asset sales, related-party relationships and the broader Brookfield corporate structure.

The challenge for MM is not quality; it is valuation. We like the asset class, we like the operator, and we like the long-term thematic exposure. However, after a strong run, BIP looks more fairly valued than cheap.

- For now, BIP goes on the Hitlist as a high-quality infrastructure candidate, with the risk/reward improving back under $US37.