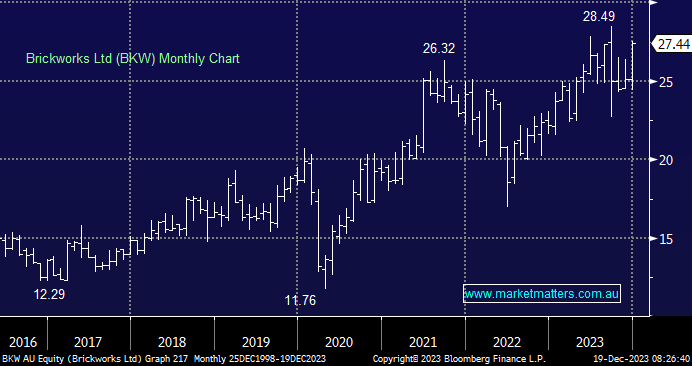

BKW held its AGM last month, with the key takeouts being a 10% reduction in property trust valuation in 1H24, although there is still a strong rental uplift anticipated, 1Q24 Australian and US building product earnings (EBITDA) are set to increase compared to last year as cost pressures finally start to subside. Similar to CSR, valuation is the issue after the stock’s +24% advance in 2023. Also, with BKW, we always have the valuation complexity of its 26.13% stake in Soul Patts (SOL), a quality holding but one that has a major bearing on BKW’s share price.

- We can see BKW making new highs into 2024, but the risk/reward isn’t compelling at this stage.

MM is cautiously bullish about BKW around $27.50

Add To Hit List