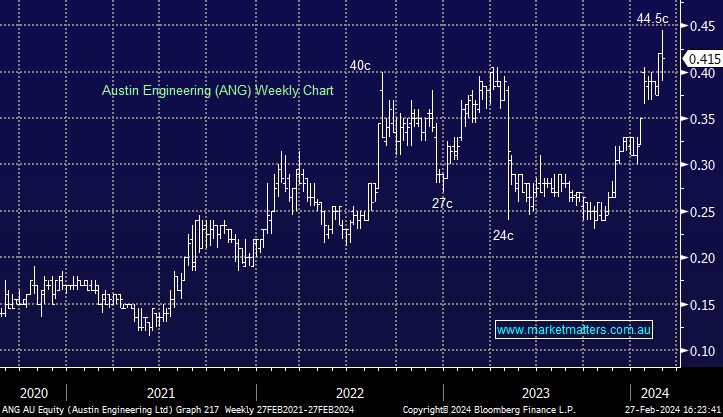

ANG -1.19%: a choppy day for the mining equipment company, Austin came in near the top of recent guidance on the 1H. Revenue grew 26% to $143.6m, while EBIT jumped 82% to $16.8m on higher margins. We spoke to the company today, some key takeaways:

- The company has added capacity and demand is filling the new supply

- Maintec acquisition is performing well

- Guidance for FY24 Rev $310-330m & NPAT $31-33m, around 7% & 12% above consensus at the respective midpoints.

- Order book at record levels provides clear visibility for near-term earnings.

- Dividends have been reinstated, paying 0.4cps fully franked. ANG is confident they will be debt free in this FY.

A very good result from Austin, shares were strong leading into the report though which meant a lot of it was in the price. This is one we continue to like but want to see some heat come out first.

MM is bullish ANG

Add To Hit List