At MM, we believe the backdrop for active management has dramatically improved over the last few years and the dynamics that have driven that improvement remain in place. When interest rates were at record lows, the support for the broad market was significant – the macro backdrop was helping to lift all boats. That has clearly changed, quite dramatically, and there will be stocks & sectors that handle the transition better than others.

Our job at MM is to identify those areas and direct our subscribers into the parts of the market that have tailwinds, and avoid the areas with obvious headwinds.

- One sector that we believe has meaningful tailwinds, that are likely to persist for years to come, is uranium.

The global energy mix is changing as decarbonisation is one of, if not, the most dominant investment theme for the next decade. We believe Nuclear energy will become a larger slice of the energy mix, and we are seeing tangible evidence of this occurring. Uranium is traded primarily on term contracts, and so far this year nearly 100m pounds have been contracted. That is the highest amount of contracted Uranium in over a decade.

- The Spot Uranium price is ~US52.93/lb as at 30th April, up from $US28.90/lb in 2021, although it is little changed over the past 12 months, meaning the various stocks & ETFs that are exposed to Uranium have experienced a similar fate.

According to Bank of America, there will be a shortage of uranium through to 2035 as demand intensifies with around ~100 reactors expected to be built or extended in the next few years.

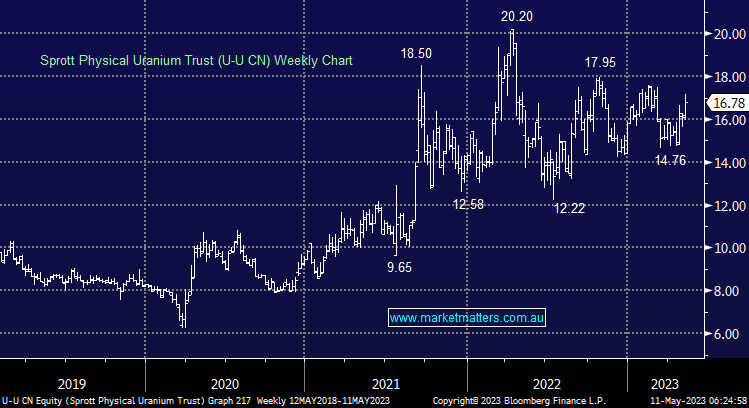

The Sprott Physical Uranium Trust (U-U-CN) is the world’s largest Physical Uranium Fund, buying and storing uranium on behalf of its investors. It now holds assets of US$3.3bn and is traded on the Toronto Stock Exchange. In MM’s view, this is the purest way of investing in physical uranium.

MM is bullish uranium over the coming years

Add To Hit List