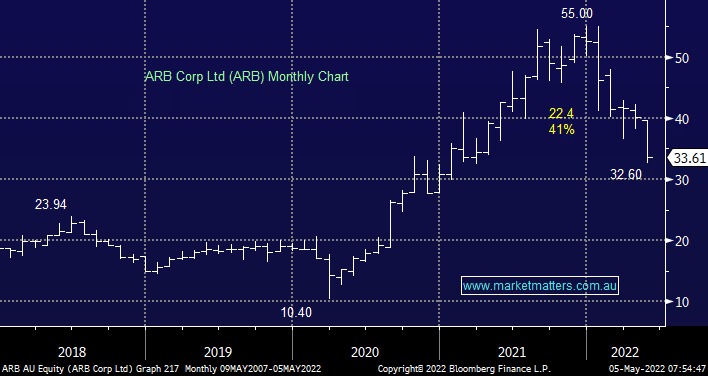

On Wednesday 4-wheel drive accessories business ARB disappointed investors with its latest trading update which showed a slowdown in sales over the 3rd quarter. The company is struggling with staff like many businesses post COVID plus the huge and mounting new car back-log looks set to see sales growth slow further, lastly for good measure the increase costs of commodities is squeezing materials and margins i.e. when it rains it pours! We like ARB – it’s close to being my favourite retailer – but as we’ve seen recently stocks that deliver weak results continue to slide, hence a little more downside wouldn’t surprise. From a valuation perspective, it’s now on 21.9x FY22 earnings which is cheap compared to it’s 5 year average of 27.5x.

MM is neutral ARB here, but would become interested ~$30

Add To Hit List