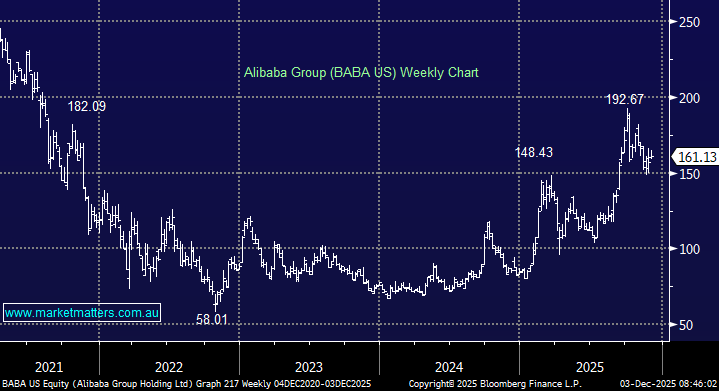

Investing in Chinese tech stocks relative to their US counterparts has been a recipe for underperformance in recent years. From the heady days in 2020, BABA’s share price has almost halved, it’s earnings multiple has gone from 25x to an average of 13x, and while a recent rally from lows has pushed the multiple back up to 19x, we think BABA still represents strong absolute and relative value around current prices.

There are multiple parts to the BABA business, that are at different stages of their evolution;

- China E-Commerce (Core Cash Engine) which includes: Taobao, Tmall, 1688, Ele.me (food delivery). The cohort is expected to generate ~50% of Alibaba’s revenue in FY26, although recent performance has been on the weaker side as the company pushes to gain market share in China’s brutal instant-delivery segment.

- International Digital Commerce which includes: Lazada (SEA), AliExpress (Europe/LatAm), Trendyol (Turkey), likely to contribute around ~15% of revenue in FY26. This segment is expanding strongly in emerging markets, producing 33% YoY growth in FY25.

- Cloud Intelligence, which includes: Alibaba Cloud and DingTalk. This is the fastest-growing segment with AI-driven services delivering triple-digit growth and is expected to contribute ~15% of group revenue in FY26, underpinned by CN¥380 billion of investment in cloud & AI infrastructure over the next three years. By 2030, this division is likely to be more than 20% of revenue.

To put some context around BABA’s earnings power, in FY25 revenue was $US137bn, producing a net profit of $US22bn relative to its market capitalisation of $US383bn. Compared to Microsoft (MSFT US), a $US3.6 trillion company which produced a profit of $US100bn in FY25, it’s around 1/10th the size, but produces 1/5th of its earnings.

FY26 will be a year of heavy investment, which will impact earnings. On consensus numbers, net profit will be down 29% despite top-line revenue growth of ~7%. This investment should start to pay off in FY27 an beyond, where earnings are forecast to compound at +25% growth YoY out to FY29.

There is a leap of faith required here, however our confidence firmed following their quarterly update in November. We’ve been waiting for Alibaba’s big AI investments to show up in the numbers, and that’s starting to happen. Cloud revenue last quarter was up +34% YoY, up from +26% growth in the prior quarter. They’ve poured RMB120B in AI capex over the last four quarters, and the early return profile is looking encouraging. Importantly, this is the business the market cares most about.

Overall, we’re seeing accelerating growth in cloud with strong AI adoption, and early signs that years of heavy investment are starting to pay off. For now, the benefits are being offset by its aggressive push into China’s hyper-competitive fast delivery system, which has been crimping the stock performance for now, and why BABA’s earnings multiple has risen to 19x even when the stock price remains ~50% below its prior peak.

- To remain bullish on Alibaba, we need to believe in their approach, which is favouring long-term growth at the expense of near-term earnings. Ultimately, we think this will pay off, though patience is still warranted, and there are certainly risks around this strategy.

All said, we believe Alibaba represents a legitimate growth stock that is being priced more on near-term headwinds versus long-term upside. We own BABA in the International Equities Portfolio and would be comfortable buying at current levels.