There has been considerable focus on the Hybrid market in recent days given the move by Swiss regulators to completely wipe out the value of ~$US17bn of risker Credit Suisse notes, which are referred to as CoCos (Contingent Convertibles). Today we’ll revisit what this means for our hybrid holdings in the Market Matters Income Portfolio. NB: Legal action is now underway focussed on the regulator for taking this action.

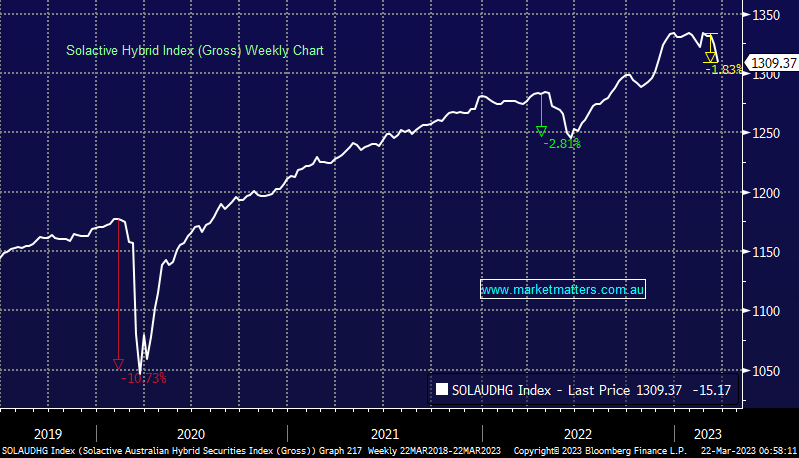

Firstly, a look at the Solactive Hybrid Index which provides important insight into how the broader Hybrid market has performed during this recent test (click here to read more about this index). The index has fallen ~2% from its recent high set in February. When prices fall, yields increase, with the average spread (which is the margin in excess of the 90-day bank bill rate on ASX major bank 5-year hybrids) moving from a very low 2.2% out to just under 3% – which is more aligned with historical levels. At times of more severe stress such as the pandemic, margins increased to 7.34% while yields on risker issuers like Macquarie & Challenger moved out by more.

As we wrote yesterday (click here), Australian Hybrids have many different features to European Hybrids and are generally lower risk. This is reflected by lower yields, less volatility, and more certainty in the future return of capital. Importantly, while these are traded securities and changes in perceived risk in the market, relative pricing, duration, supply & demand, structure, and a number of other factors have a bearing on prices, the key aspect to focus on is the financial health of the underlying company, in our case, highly regulated, stress tested and incredibly well capitalised Australian Banks, with rating agency Fitch overnight reaffirming as much.

- We remain comfortable with the financial health of the Australian banking system

The table below looks at the performance dynamics of our held positions, aimed at providing some clear context and understanding of the moves we are witnessing. While these cover our held positions, they are indicative of major bank hybrids across the market.

While hybrids are risker than cash and higher-ranking bonds, and there is always a higher element of risk in a security offering higher returns, we continue to believe the risk/reward dynamics across the hybrid securities of regulated Australian companies (banks & insurers) remain solid. We will remain vigilant as always, but we are not concerned with the implications of this week’s events overseas on our allocation to Hybrids in this portfolio.

For more information on hybrids, there are useful resources on the Market Matters Website:

Understanding Hybrids – Click Here

Hybrid Securities: A deep dive with an expert who manages over $1 billion in ASX-listed Hybrids – Webinar – Click Here

The journey when holding Hybrids – Click Here

Best Hybrids now interest rates are rising – Click Here

I’m confused by Hybrids – Click Here