- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

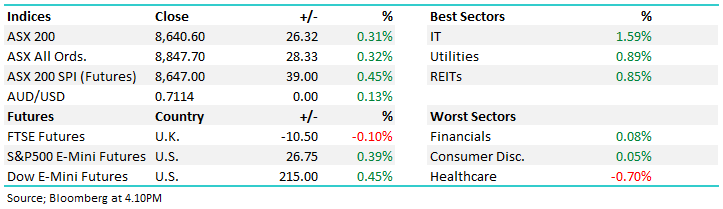

The ASX 200 closed up in a decent session, shrugging off the RBA’s move and the immediate Iran-related volatility and instead refocusing on underlying fundamentals. With the RBA firmly in the rear-view mirror following Tuesday’s hike, attention has shifted squarely to tonight’s US Federal Reserve decision. Tech and real estate led the charge, with growth stocks clawing back recent losses as bond yields settled and seven of eleven sectors finished higher — the kind of broad participation that hints at improving conviction in a wobbled market.

- ASX 200: 8,640 / +26pts / +0.31%

- AUD/USD: 0.7114 / flat / +0.13%

- Best sectors: IT +1.59%, Utilities +0.89%, REITs +0.85%

- Worst sectors: Financials +0.08%, Consumer Discretionary +0.05%, Healthcare −0.70%.

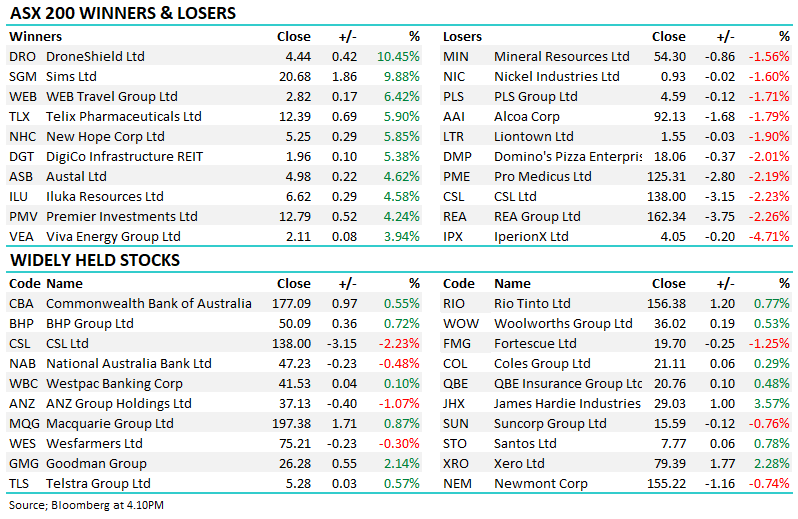

- DroneShield (DRO) +10.45% was the session’s best performer in the ASX 200, continuing to attract flows as the defence and national security theme gains momentum.

- Sims Ltd (SGM) +9.88% surged after guiding FY26 underlying EBIT of $350–$400 million ~25% above consensus, driven by strong non-ferrous metal prices and explosive growth in its Sims Lifecycle Services division tied to AI infrastructure demand.

- WEB Travel Group (WEB) +6.42% was one of the stronger moves of the day without a specific catalyst, likely a technical bounce after being among the harder-hit consumer discretionary names through the recent sell-off.

- Telix Pharmaceuticals (TLX) +5.90% continued its recovery from earlier weakness around the FDA resubmission process. The stock is now +15% on the week — a sharp reversal for a name that had been aggressively sold.

- New Hope Coal (NHC) +5.85% bounced strongly as the energy trade found renewed interest, with Viva Energy (VEA) +3.94% and Ampol (ALD) +2.37% also firming.

- Humm Group +6.1% rallied after the Takeovers Panel declared “unacceptable circumstances” relating to misleading disclosures around Credit Corp’s takeover proposal.

- Macquarie Group (MQG) +0.87% after Reuters reported it had withdrawn from bidding for a stake in Kuwait’s oil pipeline network valued at up to $US7 billion — investors welcomed the reduced geopolitical exposure.

- Premier Investments (PMV) +4.24% was a pleasant surprise among consumer discretionary names — a sector under significant pressure since the RBA hiked.

- BHP (BHP) +0.72% edged higher after confirming Brandon Craig as its next chief executive from July 1, replacing Mike Henry after six and a half years in the role. Fortescue (FMG) −1.25% drifted lower, underperforming the broader sector.

- Xero (XRO) +2.28% and NextDC (NXT) +3.55% led the technology recovery as rate-sensitive growth names found their footing with bond yields stabilising. Goodman Group (GMG) +2.14% led the real estate sector.

- ANZ (ANZ) −1.07% was the notable drag among the banks following Goldman Sachs’ downgrade to neutral. Commonwealth Bank (CBA) +0.55% to $177.09 and Westpac (WBC) +0.10% both edged higher, while NAB −0.48% also slipped, giving back some of Tuesday’s outperformance.

- Gold miners struggled as bullion dipped with Ramelius Resources (RMS) −1.22%, Westgold Resources (WGX) −1.12% and Genesis Minerals (GMD) −0.64% all lower, while Northern Star (NST) +1.40% managed a modest bounce.

- CSL (CSL) −2.23% was a notable loser among the large caps despite CSL Seqirus announcing a multi-year PAHO flu vaccine tender win for Latin America — the market appears focused on broader healthcare sector rotation rather than the positive news flow.

- Oil eased to around $US102.50/bbl — Brent still up nearly 70% year-to-date despite the modest pullback on the Iraqi pipeline news.

- Gold was around 5,000/oz at our close.

- Asian markets: China −0.6%, Hong Kong +0.1%, Nikkei +2.7%

- Futures: FTSE −0.10%, S&P 500 E-Mini +0.39%, Dow E-Mini +0.45%