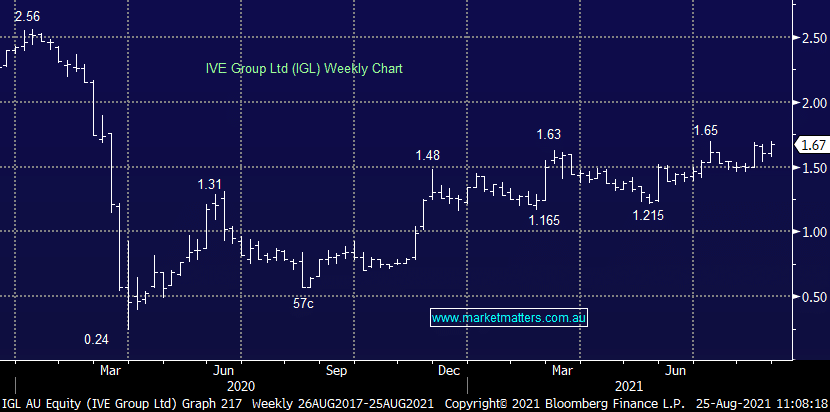

IVE Group (IGL)much improved after tough FY21

FY21 Result: a tough environment for the integrated marketing business over the previous 12 months, but they have emerged in a good position, meeting expectations at the FY21 result. Revenues were marginally lower while EBITDA (ex-jobkeeper) was up slightly, both as expected. Cost control has been the key for IVE Group, setting them up for stronger returns as more work starts to feed in. Importantly, IGL has been able to de-lever with net debt now below EBITDA, as well as undertaking a share buyback and pay dividends. While no guidance was provided, the company talked to revenue growth and with improved operating leverage this should be expected to drop down to stronger earnings. IGL was trading +1.23% higher at the time of writing.

MM remains bullish IGL

Add To Hit List