Iron ore sell off not enough to hold ASX back (NCM, IFL, FMG)

WHAT MATTERED TODAY

Momentum continues to carry the market higher with another day which saw solid intraday buying, pushing the market within 0.5% of an all-time high. Banks were the beneficiaries again – the Big 4 added 14pts to the move today. On the flip side, iron ore names were whacked for a second consecutive day with more brokers turning on the commodity – Morgan Stanley this time saying the top looks to be in place. Vale were also given permission to restart production at some of their processing operations but it will be a drop in the ocean for the wider iron ore market.

Flash PMI data from around the world came in overnight, further bolstering rate cut expectations. The ECB is the next central bank up to the plate with their decision out tonight. The RBA governor Philip Lowe was also speaking today and traders became more confident of another cut before the year is out. The stars are already starting to align for the WBC economist who just yesterday added an extra cut in to take their forecast to 0.5% by February next year.

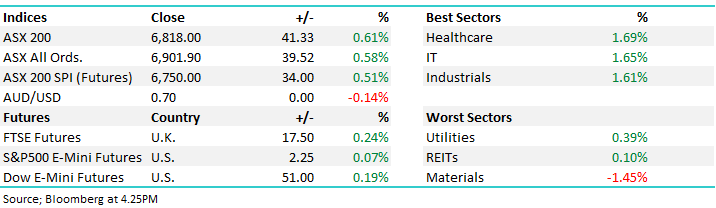

Overall, the ASX 200 added +41pts today or +0.61% to 6818. Dow Futures are trading up 51pts / 0.19%.

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE;

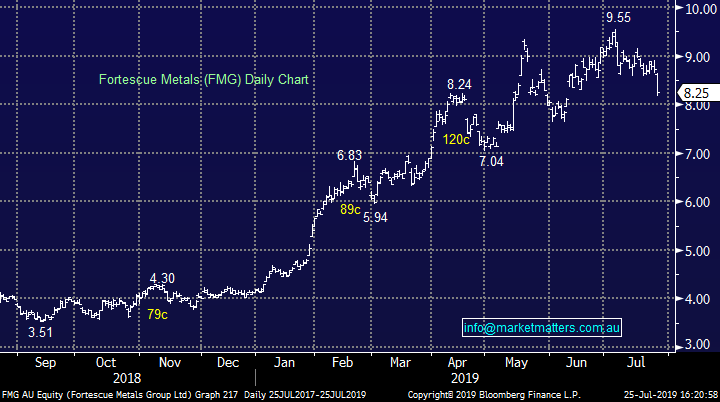

Fortescue (FMG) -5.5%; quarterly today came with huge expectation given the rally in the iron ore price so far this year, and Fortescue put up a valiant effort but just fell short of the lofty expectations. Iron ore production stormed home in the 4th quarter with record shipments of 46.6mt for the lower grade ore miner, taking the full year to 167.7Mt, bang in the middle of guidance – slightly below last year but as expected given the impact of cyclones. Their new West Pilbara Fines, Fortescue’s new higher grade ore, accounted for 10% of shipments. This is expected to grow to around 20% of the company’s total over the next few years. This was just one reason the discount FMG received for their ore fell to 13% after peaking close to 45% late last year – the other being the global shortage of ore following the Vale disaster. Fortescue still have a net debt figure of $US 2.1b, but this number is well below the peak and very manageable if iron ore remains elevated.

Part of the reason for today’s tumble was general iron ore equity selling given the comments from a number of analysts calling the top of iron ore. The other part was some softer guidance from Fortescue. They expect costs to rise substantially in FY20 as all miners start to feel the pinch of higher costs that come with a commodity boom, but production will increase ~3%. We like Fortescue from marginally lower levels. We would look to accumulate stock below $8.

Fortescue (FMG) Chart

Newcrest mining (NCM) -0.68%; June quarter rounds out the year for Newcrest with total gold production rising 6% helped by a record final quarter for the company’s biggest project, Cadia. The realised gold price slipped around 3%, but this was more than offset in the margins by a 12% fall in costs. Growth options for Newcrest remain strong, however they are experiencing some delays to the PNG project Wafi-Golpu. PNG is a notoriously difficult country to keep to a timeline in mining projects, and the market shouldn’t be taking this delay personally. The company is also working on a stake in Canadian mine Red Chris as well as a feasibility study into a Cadia expansion which should help the company deliver production growth for years to come.

We like NCM, and gold exposure here despite the rally. Gold will be supported in low interest rate environment, and MM have the unpopular view that the AUD will see some buying around these levels also providing a tailwind to NCM. We own Newcrest

Newcrest (NCM) Chart

Broker moves;

- Iluka Downgraded to Neutral at UBS; PT A$10.60

- Iluka Downgraded to Neutral at Credit Suisse; PT A$10

- Iluka Downgraded to Negative at Evans & Partners; PT A$9.50

- Eclipx Downgraded to Neutral at Citi; PT A$1.56

- Beach Energy Downgraded to Neutral at Citi; PT A$2.06

- Credit Corp Downgraded to Hold at Blue Ocean; PT A$27

- McPherson’s Downgraded to Hold at CCZ Statton; PT A$1.76

- St Barbara Downgraded to Underperform at Macquarie; PT A$3

- St Barbara Cut to Underperform at Credit Suisse; PT A$2.76

- St Barbara Downgraded to Hold at Argonaut Securities; PT A$3.21

- St Barbara Upgraded to Buy at Canaccord; PT A$4.10

- Evolution Downgraded to Underperform at Macquarie; PT A$4.20

- Evolution Downgraded to Sell at Canaccord; PT A$4.05

- Computershare Downgraded to Underperform at Macquarie; PT A$15

- SeaLink Rated New Sector Perform at RBC; PT A$3.75

- NAB Downgraded to Hold at Morningstar

- Goodman Group Downgraded to Sell at Goldman; PT A$12.32

- Vicinity Centres Upgraded to Buy at Goldman; PT A$2.76

- Pacific Energy Downgraded to Hold at Baillieu Ltd; PT A$0.98

- Tabcorp Downgraded to Equal-weight at Morgan Stanley; PT A$4.70

- Rio Tinto Downgraded to Underperform at Credit Suisse; PT A$92

OUR CALLS

We sold nib Holdings (NHF) in the Growth Portfolio for a solid 47% profit today.

We also sold Netflix (NFLX) in the International Portfolio overnight as it broke through our $US 310 limit – opening at $US 310.51

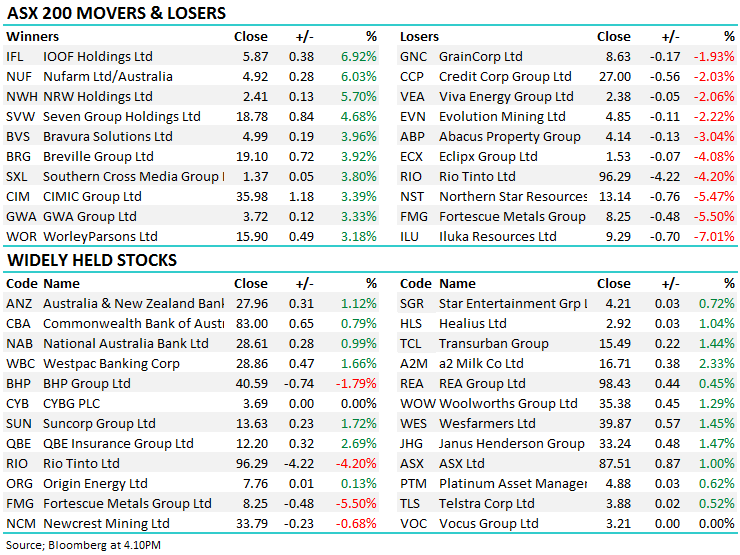

Major Movers Today – IOOF (IFL) rallied on an impressive jump in FUMA – up 18.7% on the prior year. The bulk coming from their ANZ Wealth acquisition, but a ~6% organic growth is far better than expected.

Have a great night

James, Harry the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 25/07/2019

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report not with standing any error or omission including negligence