Income Report: Where to put money coming out of Term Deposits? (MXT, MOT, PCI, NBI, XARO AXW)

Market Matters Income Report 16th October 2019

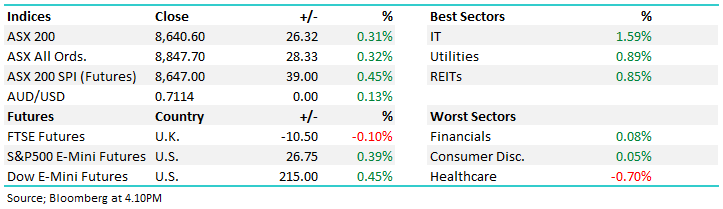

A strong session overnight and that has filtered into decent buying across the Australian market today. Major strength coming from the more defensive consumer staples and healthcare sectors with the risk on IT and Material sectors are actually in the red, not what you’d expect on a day where the market is up +60pts. A heap of mining news out today with Oz Minerals and RIO out with quarterly production figures, both were okay. Elsewhere, Challenger Group Financial (CGF) delivered a better than feared Q1 performance report with the stock trading up +7% at time of writing. There is a lot of negativity in the market on this stock and less bad news is clearly very positive relative to market positioning – this could run further.

Overall, the ASX 200 is currently trading up +60pts or +0.90% to 6711.

ASX 200 Chart

The Income Portfolio was down marginally, off -0.15% in the week against the backdrop of the ASX200 Accumulation index which traded around +0.9% higher. The portfolio was dragged by another -5% fall in Perpetual (PPT) while stalwart GMA added more than 6%. The portfolio is still tracking well, currently up +2.11% financial year to date, versus its absolute return benchmark of +1.44%. Since inception the portfolio is up +18.90% vs the benchmark of +12.36%

For those interested in investing for income in a low rate environment, Market Matters manages the investments for the Market Matters Active Income portfolio offered under Praemium SMA. The portfolio is based on the MM Income Portfolio. The SMA has now passed its first anniversary and performance has remained sound, the September update can be viewed – HERE

A look at listed income funds

The most common question / query we’re getting across the desk is where to put money coming out of term deposits so income levels can be sustained and lifestyles can be defended. The answer depends on risk, timeframe and an individual’s tolerance for volatility. As a quick example, if we look at the volatility in returns of the MM Income Portfolio that holds around 50% in more defensive income securities v the Growth Portfolio which is largely all shares, the volatility is around 40% less, which makes sense given the composition of assets.

In recent times, we’ve seen a large increase in the number of listed investment funds tapping into the search for alternative yield – by that we essentially mean yield not from cash, but also not from shares or property. The most recent fund pounding the pavement is a big one from private equity goliath KKR – we’ll look at this and others below.

Currently, we hold two listed investment trusts in the portfolio, namely MXT & NBI, while we’re planning to add an additional income security into the portfolio, although still contemplating what equity position to trim.

1 KKR Credit Income Fund (KKC) New Offer : This is live with the general offer now available, however the broker firm closed early (10thOctober) plus they have up-scaled the deal to be $925m from the original $825m, clearly significant demand for these sort of offerings at present. This is a more diversified credit fund meaning that they focus across the credit spectrum investing in strategies / portfolios of loans, bonds, fixed and floating rate notes around the globe which includes both traded and private credit – clearly a very broad church. They target a net return of 6-8%p.a. although the actual income target pa is 4-6% and that is through a market cycle. Right now, we’re at a low point in terms of yields so the concept of through a market cycle would imply that 4% is a more realistic goal at this point.

What we like: Big robust global manager, strong demand should see a reasonable aftermarket, realistic return objective & alignment

What we don’t: We prefer a more targeted approach like some of the funds below, fees are fairly high for a credit product – when base fee, expense recovery, RE & indirect costs included, it equates to around ~1.2%, plus there is a performance fee. Fee’s could end up being around ~1.5% for a credit product in a low rate environment. When net target return is 6-8%, and fees are 1.5%, it means they are investing in credit delivering 7.5-9.5% return potential while they’re incentivized to deliver through a performance fee. This implies a higher risk exposure in our view

2 Metrics Credit Partners (MXT) $2.06: This is a more concentrated / targeted fund that we hold in MM Income Portfolio after buying in the IPO 2 years ago at $2. When they listed, they were the first sort of listed vehicle tapping an alternative style income market, in this case being domestic corporate loans, so sitting alongside, or in place of banks, lending to Australian corporates. Over that time, MXT has been a consistent performer, have stayed true to label and led the charge into an asset class that retail investors generally couldn’t access. They target the cash rate plus 3.25% and have over delivered versus that benchmark.

What we like: A specialist manager that was first mover in the space, now a lot more copy-cat funds although newer funds typically have wider mandates. Realistic performance target, Good fee structure of 0.66%, no performance fee.

What we don’t: Given the underlying exposure is corporate loans, pricing them is difficult so NTA may not be reflective of actual realizable value

MCP Master Income Trust (MXT) Chart

3 MCP Income Opportunities Trust (MOT) $2.06: After the success of MXT, Metrics came back to market with another offering in May of this year which we described at the time as being MXT’s riskier cousin. The fund invests in a number of different sub trusts with the underlying investments being higher risk credit described as sub investment grade. They pay higher yield but come with a higher level of risk. The manager has more discretion in MOT than they do in MXT to take advantage of opportunities as they arise, however less structure means returns rely more heavily on the Portfolio Manager getting it right. There is a bunch of risk management limitations in MXT that are not in MOT and as a consequence the risk is higher and so to the targeted returns, 7% p.a. income (plus a few % capital growth to get the 8-10% total return target).

What we like: A higher risk, higher return offering from a quality manager with a good track record, distributions will not be topped up by capital if there is a shortfall in income from loans.

What we don’t: High fees with annual management fee of 1.45% and a pretty aggressive +15.38% performance fee over RBA + 6% benchmark. Worth noting that with the RBA rates below 1%, the performance fee will be paid before the income target of 7% is hit and distributed. On the flipside, if the RBA raise rates this becomes a more challenging task and given the broad structure of the trust and discretion of the Manager it could push them to take more risk to achieve performance targets.

MCP Income Opportunities Trust (MOT) Chart

4 Perpetual Credit Income Trust (PCI) $1.13: lower risk than the MOT outlined above and a more traditional credit offering. As a consequence, the return target is aligned with that risk / return profile. The trust focusses on investment grade assets in the high yield Australian corporate loan market and the global high yield bond market – it’s sort of a cross between MXT and NBI which we touch on below. The fund targets a return of the RBA cash rate plus 3.25%, which is the same target held by MXT.

What we like: Realistic return objective, reasonable fee structure of 0.88% (although higher than MXT), good diversifier for those looking for income that is not heavily aligned to equity markets

What we don’t: We prefer to separate funds out into specific strategies

Perpetual Credit Income Trust (PCI) Chart

5 NB Global Income Trust (NBI) $2.08: NBI invests in global bond markets, holding a very diverse portfolio of overseas bonds. They are a very well credentialed US manager and have delivered what they set out to achieve since listing in 2018. The MM Income Portfolio bought these on listing and continue to hold them in the portfolio. They target a return of 5.25% per annum.

What we like: Very diversified portfolio of global bonds, they only do global bonds in the portfolio, Fee structure of 0.85% with no performance

What we don’t: Having a fixed return objective becomes more difficult (relative to floating) as rates drop, potentially forces more risk taking.

NB Global Income Trust (NBI) Chart

6 Gryphon Capital Income Trust (GCI) $2.07: GCI invests is residential mortgage backed securities (RMBS), which in simple terms is a security that is underpinned by a bunch of housing loans. They are a specialist manager in this area of the market with a good track record. Income and capital preservation the key here and it’s hard to fault this security, they’ve delivered what they set out to do since listing with low overall volatility. They target income return of RBA Cash + 3.50% (net of fees), Management cost of 0.96% with no performance

What we like: A good portfolio diversifier generally only available in unlisted managed funds.

What we don’t: Exposure to residential mortgages when the bulk of local investors are already very long banks and domestic property

7 ActiveX Ardea Bond Fund (XARO) $26.47: This is a relative valuation strategy targeting high quality government bonds with 70+% exposure in Australia. They actively manage exposures through buying relatively cheap bonds and selling relatively expensive bonds, therefore eliminating risks around interest rate duration which is obviously a major consideration when investing in bonds at this low point for global interest rates. The managers have a strong track record over the past 10 years, they manage around $13b across fixed income markets and many well-known Australian Institutions invest with them. They target a return of CPI +2% however have done significantly better over time, they charge 0.50% pa management.

What we like: A very well credentialed active fixed income manager, trading in Government Bonds, relative value strategy removing interest rate risk , very defensive and low risk

What we don’t: Return objective is on the low side however the risk is equally low

We plan to add the XARO into the MM Income Portfolio with a 7.5% weighting, although we need to trim an equity position to do so

Ardea Active X Bond (XARO) Chart

Conclusion

Of the funds above, we hold NBI, MXT and plan to buy XARO today. We like all three.

We like PCI and GCI, but less so than the funds above

We are less keen on KCC & MOT due to high fees & return targets implying higher risk exposures

Have a great day

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.