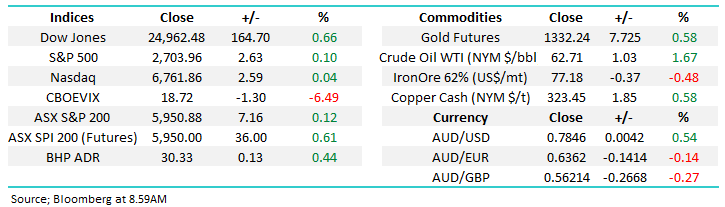

Volatility soars at ground level as the overall market steadies nicely (CYB, WEB, OZL)

The ASX200 has now recovered around half of its losses since our early January high and US stocks are trading within 6% of their all-time high, as we expected the recent volatility / yield tantrum is rapidly becoming a distant memory. Following decent gains by US stocks overnight we are set to challenge the important psychological 6000 level this morning

· Overall, we believe it’s just a matter of time before the local market punches through and heads towards fresh 2018 highs – our ASX200 target into March / April is ~6250.

Our view at the start of 2018 remains intact and will remain the core to our investment decisions until further notice:

1. Stocks would have a ”warning style” correction for a short-term buying opportunity in early 2018 – this obviously occurred and we bought aggressively.

2. Many global indices will make fresh all-time highs between now and April before its time to get off the stock market express and reassess.

Today’s report focuses on 3 of our stocks that have experienced large market swings over recent times to clarify our current thoughts on these holdings.

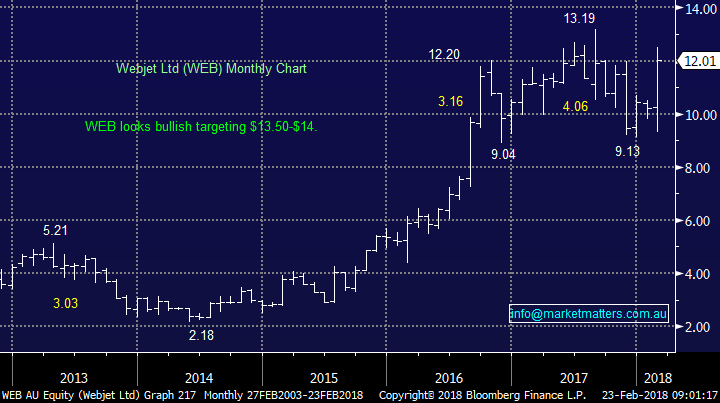

1 Webjet (WEB) $13.01

WEB soared over +16% yesterday following their half-year results which showed a +55% increase in transactional value (TTV). Importantly net profit came in +45% with the key driver being its Webeds segment. WEB has maintained its guidance of $3bn TTV value and we still feel it’s the best stock in the sector at current levels.

As of the 16th of this month WEB had a significant short-position of almost 7% which may underpin the stocks rally towards fresh all-time highs.

We are bullish WEB medium-term targeting the $13.50 area i.e. over +10% higher.

Webjet (WEB) Monthly Chart

2 OZ Minerals (OZL) $9.39

OZL enjoyed a solid day yesterday rallying over 5% following its simply excellent profit report on all levels spearheaded by a 72% surge in profits to the best level since 2011. Also, the dividend came in well above analysts’ estimates and the copper / gold miner is now yielding ~2.1% pa fully franked. The market had been concerned about future growth for Oz Minerals given the shorter life span of their Prominent Hill mine, however after being on the conference call yesterday, I’m confident that Prominent Hill can be extended, and Carapateena will provide a very good runway for future growth.

We remain bullish OZL targeting a break of $10 while the stock can hold above $9.30.

OZ Minerals (OZL) Daily Chart

The Australian resources sector is highly correlated to the Emerging Markets Index (EEM) which is arguably our favourite market at this point in time. While we expect further consolidation of the coming weeks we are overall bullish targeting ~10% further gains over coming months.

This supports our bullish view on OZL plus our other holdings within the sector.

Emerging Markets (EEM) Weekly Chart

3 CYBG (CYB) $5.20

CYB has corrected sharply from its late 2017 high, a pullback of almost 14% and we’ve seen some reasonable profits in our Growth Portfolio become losses – never a nice taste! The question is clearly what now?

Our feeling is BREXIT will sort itself out and will become just like many “economic disasters” and eventual outcome being ‘not too bad’. Rising interest rates in the UK will help CYB plus of course it’s an overseas earner which we like at MM. European stocks have underperformed during the recent “bounce” in global equities but we believe they will play some catch up over March / April.

We thought the companies trading update was ok earlier in the week but the market has clearly focused on the negative i.e. a slight fall in net interest margin. Importantly we feel the bank is cheap trading on a price to book value of less than 1x with a significant amount of costs to come out of the business.

Technically the stock looks great value around the $5.15 region and we are tempted to increase our holding.

CYBG (CYB) Weekly Chart

Conclusion (s)

No major change, at this stage we are comfortable with our short-term bullish call targeting new all-time highs from a number of global indices in the next few months.

On the stock level we continue to like WEB and OZL targeting higher prices while we are considering averaging CYB under $5.20.

*Watch for alerts.

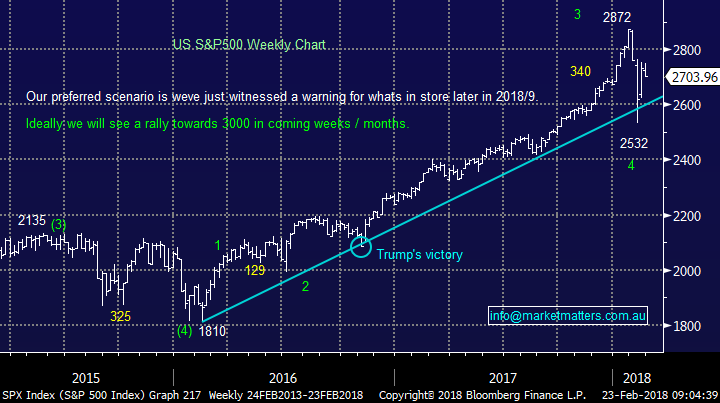

Global Indices

US Stocks

Our target area for the recent aggressive weakness by US stocks was reached and to-date has been rejected strongly. Assuming over the next few days / weeks the S&P500 can trade around current levels in a calmer fashion a test of all-time highs looks a strong possibility.

US S&P500 Weekly Chart

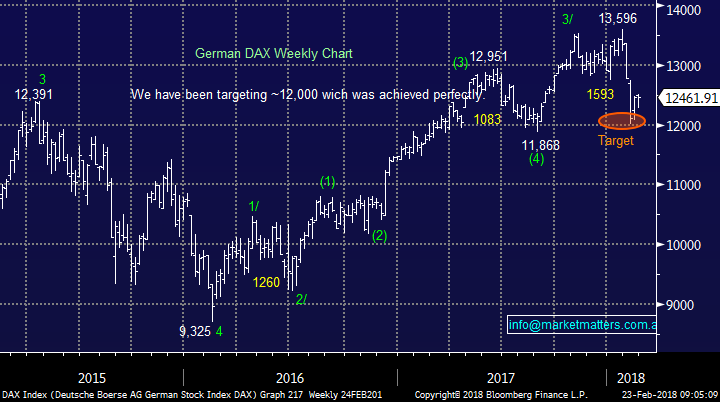

European Stocks

No major change we are now targeting around the 14,000-area for the German DAX before we will turn bearish i.e. a rally from here of over 10%! However, at this stage European equities have not embraced the global “bounce” by stocks but we believe they will moving forward.

German DAX Weekly Chart

Asian Stocks

Similarly, to western global indices the Hang Seng corrected over 10% and looks good from a risk / reward perspective under 30,000.

The more time the market can spend between 31,000 and 32,000 the stronger it will become.

Hang Seng Weekly Chart

Overnight Market Matters Wrap

· The SPI is up circa 0.7% as the DJIA added 0.7% while the S&P 500 and NASDAQ were close to flat.

· Asian and European stocks were mostly lower after the Fed yesterday released minutes of their recent meeting which indicated tighter monetary policy.

· The US jobs market continues to strengthen as the number of people applying for unemployment benefits fell to a 45 year low.

· Most metals on the LME were weaker apart from copper, while iron resumed trading in China a touch lower and oil rallied 1%.

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 23/02/2018. 9:15AM

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports.

If you rely on a Report, you do so at your own risk. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here