4 sleeps until Christmas

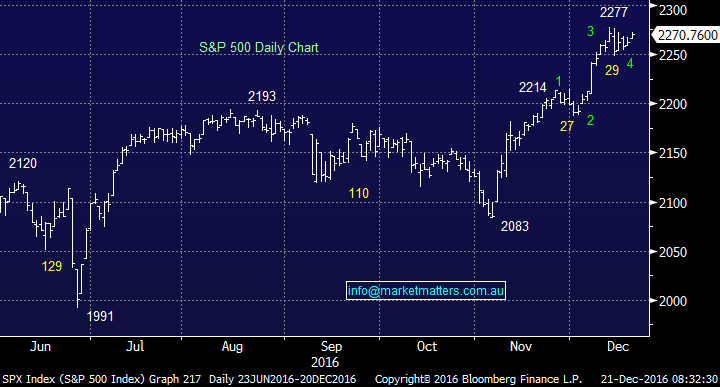

Both the news flow and the markets are slowing down for the festive season. US stocks were up again last night and remain on track to rally ~2% to fresh to all-time highs as we have been targeting - the Dow is flaunting with the psychological 20,000 level. Impressively, the S&P500 remains up close to 9% since Donald Trump was elected, an event most people were touting as potentially a big concern for stocks.

The rally in stocks since the US election leads us into our thought for the morning and more importantly, for 2017 - "be open minded". Who would have thought back in January that Origin Energy (ORG)would rally 43%, while Blackmores (BKL) would fall 52%, or South32 (S32) would rally 148%, while TPG Telecom (TPM) would fall 33%.

Today, Bellamy's (BAL) returns onto the market, amid speculation around its long term future - we are still giving this one a wide berth. Also Automotive Solutions (4WD) lists today at 12.30pm, this should be an interesting one for a sign of market confidence.

US S&P500 Daily Chart

Yesterday the local market continued with its seasonal strength, rallying 29-points to test the 5600 level, with the banks leading the way. This morning, the SPI futures are pointing to a break of this year’s high, above 5611. We continue to target ~5700 before the year is out.

ASX200 Daily Chart

This morning we have highlighted the stocks within the MM portfolio which are approaching our ideal sell levels while hopefully not giving them "the kiss of death":

WBC - Looking to take profit ~$33.

TCL - Looking to take profit ~$10.80

WFD - Looking to take profit over $9.50.

VTG - We are looking to take profit ~$3.40.

Summary

No change, we remain short-term bullish stocks but are still planning to reduce exposure during the end of December.

* Please watch for alerts.

Overnight Market Matters Wrap

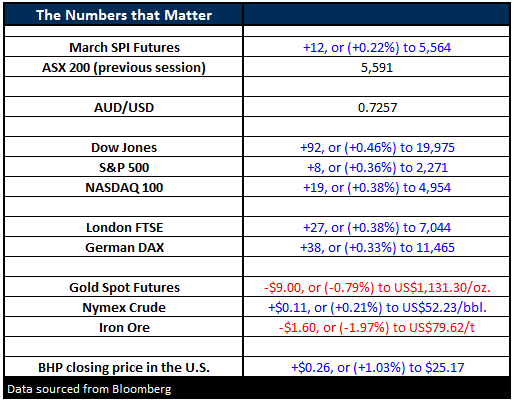

- The US markets edged higher overnight, with the Dow ending its day up 92 points (+0.46%) to 19,975 and the S&P 500 up 8 points (+0.36%) to 2,271.

- Gold futures lost some of its lustre overnight, last traded down 0.79% to US$1,131.30/oz. while Crude oil gains 0.21% to US$52.23/bbl.

- The major miners are expected to recover some or all of yesterday’s losses, with BHP in the US closing at an equivalent of 1% higher at $25.17 from Australia’s previous close.

- The ASX 200 is expected to test the 5,620 level this morning, as indicated by the March SPI Futures.

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 211/12/2016. 8.30AM

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports.

If you rely on a Report, you do so at your own risk. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here