Finally – the banks find some love! (BHP, NAB, QBE, MQG)

A better day for the Aussie Banks today with an obvious rotation out of the recently HOT commodity stocks into the beaten down financials – the BIG 4 contributing +22pts of the gains on the index while Macquarie also chimed in after they reconfirmed guidance. Elsewhere, the rotation out the commodity plays was aggressive early on however buying into weakness soon followed with the likes of BHP and RIO finishing well up off session lows, although still in the red. The gold stocks copped it on the chin as money flowed elsewhere, while the Insurers were higher despite the US Hurricane, however unconvincingly so.

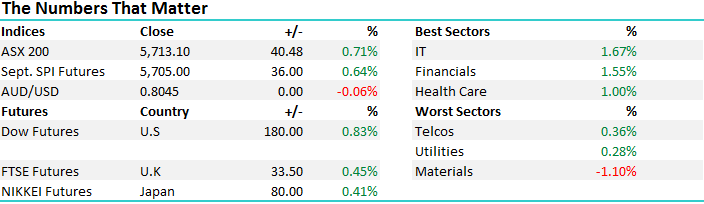

In terms of the broader market today, the IT sector led the way courtesy of decent buying in Seek (SEK) and CarSales (CRZ) while the selling was concentrated in the Material stocks which lost -1.10% - an overall range of +/- 53 points, a high of 5723, a low of 5669 and a close of 5713, off -40pts or -0.71%.

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

Macquarie (MQG); were out this morning pre-market and reconfirmed guidance of flat earnings saying they expect 1H18 earnings to be up on this time last year, and broadly in line with 2H17. The main reason is performance fees so it looks like the millionaires factory (haven’t heard that in a while!) has started the year off pretty well. Normally we see a second half skew so although the company saying earnings will be flat, expect the market to second guess this, double their first half numbers and assume 5% growth! All up, we’re not keen on MQG at current levels as discussed in the AM report today. The stock closed up +2.96% to $85.15.

Macquarie Daily Chart

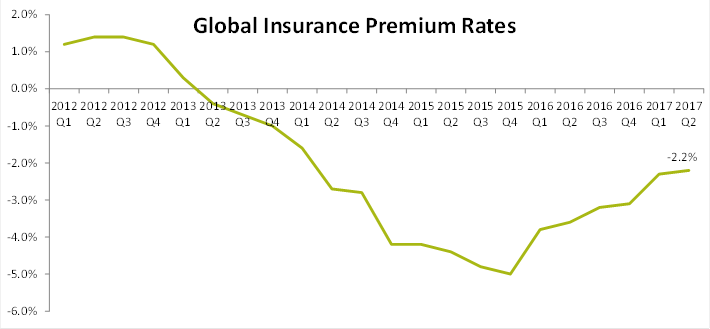

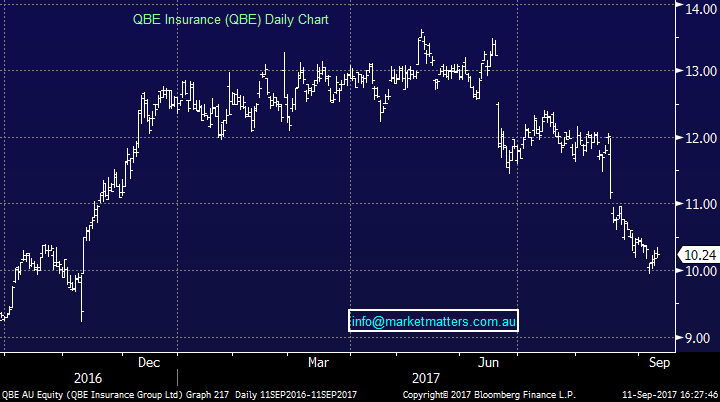

QBE; obviously a stock in the cross hairs at the moment with Hurricanes, weakness in their earnings and the macro backdrop moving against them, however looking forward we expect things to be brighter. Firstly, global premium rates are still declining, but are improving and heading in the right direction as shown recently in this chart…

Secondly, US interest rate expectations as priced by the market are a long way off where the FED is guiding to. Although we expect the Fed to be proven ‘optimistic’ in their assumptions, we think the market remains too pessimistic and some middle ground will be found. Higher US interest rates and a higher US currency at some point will both prove supportive of QBE. The stocks closed up +0.59% today to $10.24

QBE Daily Chart

…and finally, the big rotation from resources to banks played out today as MM has been suggesting now for the past week or so. We think now is the time to be overweight the banking sector using resource exposures as a funding vehicle. Using NAB and BHP as examples here to illustrate.

NAB Daily Chart

BHP Daily Chart – weakness early however decent buying off the lows

Have a great night

The Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 05/06/2017. 5.00PM.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports.

If you rely on a Report, you do so at your own risk. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here