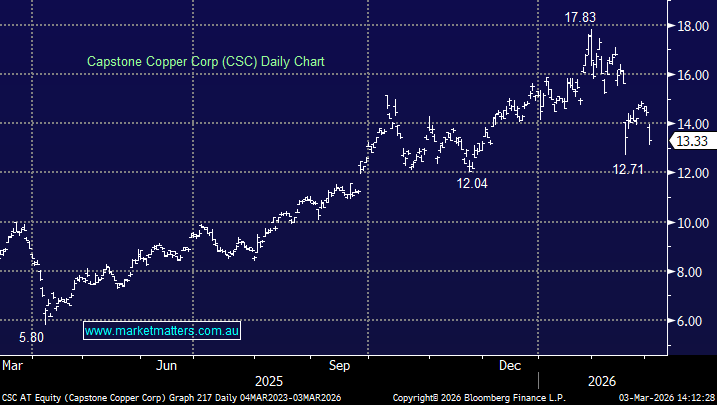

Capstone Copper (CSC) plunges ~8% Following EPS Miss

Canadian based, ASX dual-listed, copper miner Capstone Copper (CSC) tumbled ~8% after delivering disappointing fourth quarter earnings update:

- Revenue $685mn, +53% YoY, estimates $659.5mn.

- Adjusted EPS 10c vs 4c YoY, Bloomberg Estimates were 13c.

- Adjusted EBITDA $308mn, +79% YoY, estimates $311mn.

- Copper production 58,273 tonnes, +8% YoY.

Released production guidance of 200,000 to 230,000 lbs at C1 Cash Cost guidance of $2.45-2.75 reflected largely stable production with additional growth expected in 2027 tied to Mantoverde Optimized, a return to higher copper grades at Mantos Blancos, and normalized throughput at Mantoverde and Pinto Valley.

We continue to prefer Sandfire Resources (SFR)n for pure copper exposure and BHP Group (BHP) for a more diversified option.

MM is neutral towards Capstone Copper Corp (CSC)

Add To Hit List