Bank Valuations and the RBA rate cut

The following report is an extract of the MarketMatters Income Report that was published on June 5. Click here to get access to the full report and more

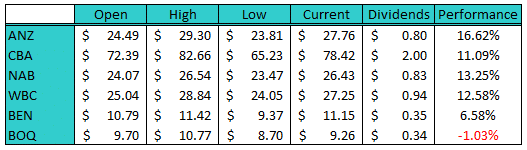

2019 to date has been a better year for the banks, and May in particular was a very strong month thanks to: 1. The election result 2. Tweaks to loan serviceability standards 3. The expectation of lower interest rates. The below table looks at the performances from the banks (including the regionals) calendar year to date.

2018 was a year when banks looked to bottom on numerous occasions but went onto make new lower lows on what felt like a continuous stream of bad news. While the recent rally from the lows has been encouraging, the obvious question is, does the move have legs?

Yesterday’s rate cut and the expectation of more to come is an overall positive for equity valuations across the board including banks, it’s certainly a positive for the property market however there is one main negative for the banking stocks that is worth considering. Banks margins have been under pressure and when interest rates fall, it’s harder for them to do anything about it. ANZ yesterday dropped rates by 0.18% and Westpac cut by 0.20% v the 0.25% cut from the RBA to help protect margins, while CBA, & NAB passed the cut on in full. If both CBA and NAB are to protect margins, they now need to recover the cut from depositors, which is ultimately bad news for savers.

Using CBA as a quick example, at last update they had $77B in transaction deposits paying an average interest rate of 0.76%, $180B in savings deposits paying an average rate of 1.14% and there were $221B in investment accounts (term deposits etc.) which paid an average rate of 2.53%. The combined funding from these sources was $478B (in 1H19) compared to home loans of $462B. It seems unlikely they can recover anything meaningful from the $77B sitting in transaction accounts with that impost likely to move onto those with investment accounts, while those with savings accounts paying an average of 1.14% will likely see their rate drop by the full amount. For CBA to protect margins it seems likely that most of the brunt will be felt by rates on investment deposits which would need to fall by 25 bps * (77+221)/221 = 33 bps. This appears achievable.

So, while yesterday’s rate cut is a positive for the market generally, it’s clearly a negative for savers and it could be a negative for bank margins if banks can’t re-price deposits. In theory, a 0.25% re-pricing across the deposit book seems achievable, however if the RBA cut again, the task becomes more difficult.

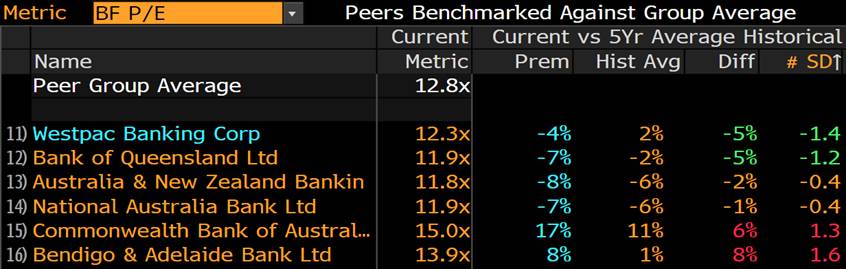

Turning to valuations, banks collectively now trade on 12.8x with 4 of 6 lenders in Australia still trading below historical multiples as shown below. CBA is now most expensive relative to the sector (+17%) but also relative to itself (+11%). Westpac & BOQ are 5% cheap while Bendigo is 8% expensive based on 5 year averages.

Peer Group Comparison

2018 was a year when banks looked to bottom on numerous occasions but went onto make new lower lows on what felt like a continuous stream of bad news. While the recent rally from the lows has been encouraging, the obvious question is, does the move have legs?

Yesterday’s rate cut and the expectation of more to come is an overall positive for equity valuations across the board including banks, it’s certainly a positive for the property market however there is one main negative for the banking stocks that is worth considering. Banks margins have been under pressure and when interest rates fall, it’s harder for them to do anything about it. ANZ yesterday dropped rates by 0.18% and Westpac cut by 0.20% v the 0.25% cut from the RBA to help protect margins, while CBA, & NAB passed the cut on in full. If both CBA and NAB are to protect margins, they now need to recover the cut from depositors, which is ultimately bad news for savers.

Using CBA as a quick example, at last update they had $77B in transaction deposits paying an average interest rate of 0.76%, $180B in savings deposits paying an average rate of 1.14% and there were $221B in investment accounts (term deposits etc.) which paid an average rate of 2.53%. The combined funding from these sources was $478B (in 1H19) compared to home loans of $462B. It seems unlikely they can recover anything meaningful from the $77B sitting in transaction accounts with that impost likely to move onto those with investment accounts, while those with savings accounts paying an average of 1.14% will likely see their rate drop by the full amount. For CBA to protect margins it seems likely that most of the brunt will be felt by rates on investment deposits which would need to fall by 25 bps * (77+221)/221 = 33 bps. This appears achievable.

So, while yesterday’s rate cut is a positive for the market generally, it’s clearly a negative for savers and it could be a negative for bank margins if banks can’t re-price deposits. In theory, a 0.25% re-pricing across the deposit book seems achievable, however if the RBA cut again, the task becomes more difficult.

Turning to valuations, banks collectively now trade on 12.8x with 4 of 6 lenders in Australia still trading below historical multiples as shown below. CBA is now most expensive relative to the sector (+17%) but also relative to itself (+11%). Westpac & BOQ are 5% cheap while Bendigo is 8% expensive based on 5 year averages.

Peer Group Comparison

The last income note that looked at bank valuation was back in December 2018 (click here) and we concluded that 2019 would be a year of outperformance for the sector, and that’s certainly played out to date. At the time the sector was trading on 10.9x with NAB trading on just 9.9x. Looking above, the move higher in the sector has all been driven by P/E expansion rather than earnings expansion, or in other words, traders are getting more upbeat about the backdrop for bank earnings, however the analyst community hasn’t amended their thinking (yet). That’s typical with analysts’ generally following share prices at turning points.

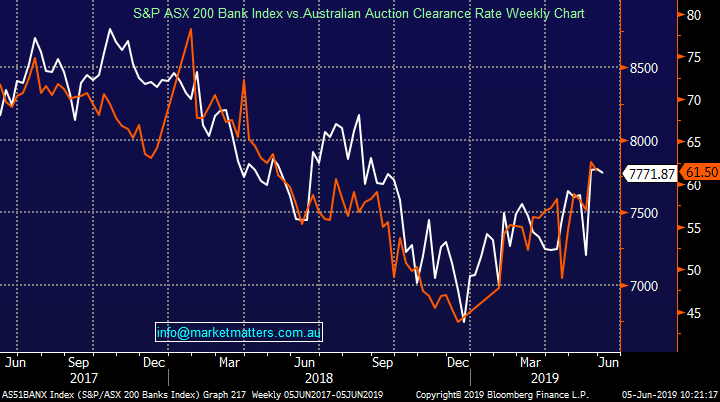

One useful indicator for bank share prices is Auction Clearance Rates, which have started to tick up from a low base. The chart below tracks the banking index with auction clearance rates and the correlation is high.

ASX Bank Index (White) v Auction Clearance Rate (Orange)

The last income note that looked at bank valuation was back in December 2018 (click here) and we concluded that 2019 would be a year of outperformance for the sector, and that’s certainly played out to date. At the time the sector was trading on 10.9x with NAB trading on just 9.9x. Looking above, the move higher in the sector has all been driven by P/E expansion rather than earnings expansion, or in other words, traders are getting more upbeat about the backdrop for bank earnings, however the analyst community hasn’t amended their thinking (yet). That’s typical with analysts’ generally following share prices at turning points.

One useful indicator for bank share prices is Auction Clearance Rates, which have started to tick up from a low base. The chart below tracks the banking index with auction clearance rates and the correlation is high.

ASX Bank Index (White) v Auction Clearance Rate (Orange)