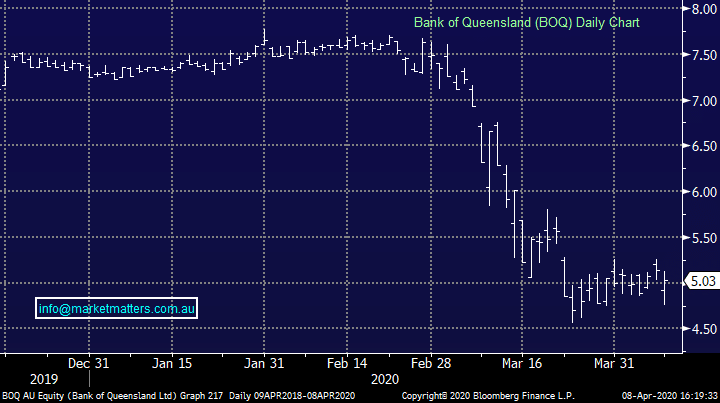

Bank of Queensland (BOQ) first half result disappoints in a tough market

Bank of QLD (BOQ) -2.14%: Released their 1H20 results today while they took APRA’s advice and deferred a decision on their dividend. In terms of the result itself they delivered cash profit of $151M for the half which was 1% lower than 2H19. Lower income and higher expenses were largely offset by a lower bad debt charge. In terms of tier 1 capital, that sits at 9.9% of risk weighted assets which compares with the guidance range of 9% to 9.5%. As we said, the interim dividend was deferred because APRA wants to understand their capital position in a yet-to-be-determined stressed scenario.

Interestingly, BOQ did provide a scenario of stress under COVID-19 that included: 1. 3% decline in GDP in 2020 followed by a recovery in 2021. 2. 8.5% unemployment in 2020 reducing to 6.5% in 2021; and 3. 5% decline in property prices. This is not a scenario they have discussed with APRA – it actually seems a bit optimistic to me - and BOQ does not yet know what stressed scenario APRA would require for the purpose of determining future dividend payments, but they will soon no doubt. In terms of outlook the main aspect to catch my attention was a large increase in the bad debt charge. The forecast is 60 bps of loans in 2H20, giving a 2H20 bad debt charge of $141M, which far exceeds the outcome from BOQ’s stress test. We remain neutral BOQ and see better opportunity towards the higher quality members of the sector Bank of QLD (BOQ) Chart