Author: james Carter

With reporting season now in full swing and volatility high in both indices and individual stocks, it’s important to keep a close eye on events as opportunities present themselves. Last night we witnessed strong moves from both the American and European Indices, our preferred scenario is still for fresh 2015 highs from these and Japanese Indices. However the recent significant weakness in the local banking sector is likely to put a lid on the ASX200 at around ~5650.

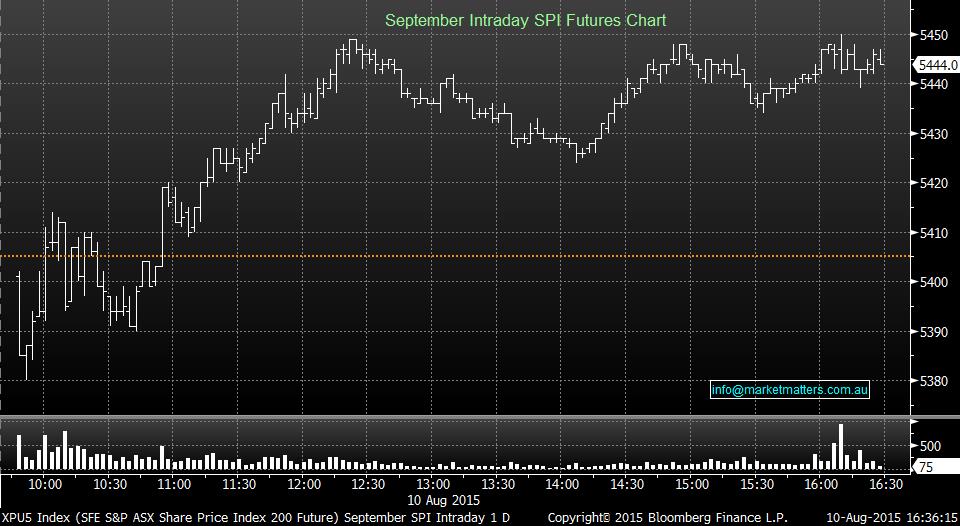

• A good start to the weak was witnessed in the ASX200 today, ending just off its day’s highs, up 34 points (+0.6%) at 5,505.

• The Banking sector contributed to today’s performance, clawing some of its losses from last week. National Australia Bank (NAB) rallied 1.5% at $33.32, while Commonwealth Bank (CBA) closed 1% higher at $82.20 – earlier this morning; CBA noted it will comment on capital requirements when it releases its Annual Results this Wednesday.

• Investors welcomed JB Hi-Fi’s (JBH) FY15 annual result, by rallying 10.6% higher at $21.69 after reporting its net profit in the top end of its guidance.

• Ansell (ANN) however, disappointed and ended 16% lower at $20.84 with currency moves being the culprit of its earnings. ANN today had its biggest one day fall in 28 years after losing ~18% at one stage.

• G8 Education (GEM) lost 1.3% at $3.09 after reporting its earnings just shy of analysts’ estimates. GEM is currently at play in the bid for rival group Affinity Education (AFJ).

• Bendigo Bank (BEN) lifted its profit; however it was below analysts’ consensus, losing 2.6% at $12.63 in trade today.

“Don’t Panic” CBA is following our Path

- The ASX 200 was described as being decimated yesterday; today it was totally obliterated and thrown to the wolves. The index finished down 135 points (2.4%) to 5,475.

- The banks were the catalyst once again with the unexpected early return of Australia New Zealand Bank (ANZ) to the boards. ANZ finished down 7.5% ($2.44) to $30.14 after the placement of shares was completed over night. Interestingly the shares traded well below the settlement price of the placement ($30.95). Commonwealth Bank (CBA) finished worst of the lot as the market began to believe that it would be the next one to raise funds. CBA finished down 3.8% ($3.25) to $81.30.

- A day after RIO Tinto (RIO) reported, the stock finished down, but was immune somewhat to the rest of the contagion, and finished down 28c to $53.27. However BHP Billiton (BHP) finished a lot weaker, down 76c (2.9%) to $25.93.

Best Sector – Information Technology

Yesterday, ANZ Bank stunned investors by announcing a $3bn capital raising (through share placement and share purchase plan), basically to keep APRA happy – it’s obvious which “tail is wagging the dog”. Although ANZ made noises to the effect of no capital raising over recent weeks, on the surface it looks smart to have acted before rivals, Commonwealth Bank (CBA) and Westpac Bank (WBC). The result yesterday was aggressive selling in the ‘slower’ two banks, as the market discounted them in anticipation of future capital raisings. The noises in today’s press are not particularly positive “too small, too expensive and unfair to mums & dads”, but nobody is saying bad market timing. At MarketMatters, we have been predicting this correction in our local banking sector and see it as an excellent opportunity for long term investors.

- The ASX 200 was decimated today, finishing the day down 64 points (1.2%) to 5610 after the Australia New Zealand Bank (ANZ) announced a A$3bn capital raising.

- The Banking Sector, as you would imagine, was hit hard. Commonwealth Bank (CBA) closed down $2.82 (3.3%) to $84.55, National Australia Bank closed down 75c (2.2%) to $33.59 and Westpac (WBC) closed down $1.05 (3.0%) to $33.44.

- The ANZ’s tune seems to have changed given they blasted the market back in May for concentrating too much on capital raisings. Today they were the last to announce a capital raising of $2.5bn through institutions and $500m from retail investors. ANZ was in a trading halt today until this issue is completed.

- The mining sector tried hard to compensate, but it was a losing battle. BHP Billiton (BHP) finished up 20c to $26.69 and RIO Tinto (RIO) finished up 57c to $53.55. Fortescue Metals (FMG) had a quiet but up day finishing up 3c to 41.91 as the iron ore price continued to improve.

Best Sector – Information Technology

Worst Sector –Energy

Yesterday, Fortescue Metals (FMG), one of our trading positions, rallied over 6% on rumours of asset sales to the Chinese. At one stage the shares were up over 10%, prior to FMG informing the market it was “open to discussions to commercial discussions but no agreement has been made at this time”. FMG has been a brilliantly run business over recent years, slashing its costs, hence giving confidence to any suitor that they will survive as Iron Ore plunges, down around 70% in around 5 years – see chart 2.

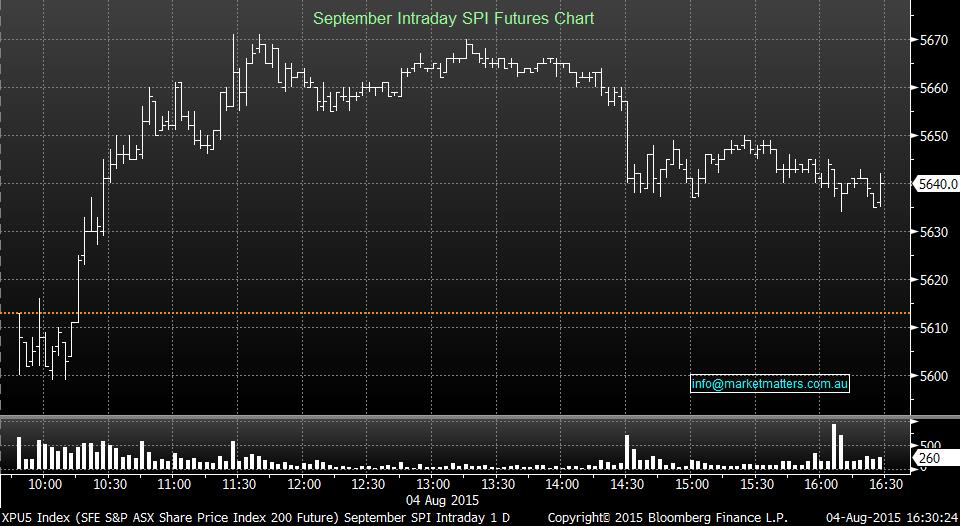

• A weak and choppy session today in the ASX 200, opening on its highs of 5,700 and reach its day’s low of 5,640 before ending the day 23 points lower (-0.4%) at 5,674.

Yesterday as expected, the Reserve Bank of Australia (RBA) left interest rates unchanged at an historically low 2% (see chart 1), but they also signaled to the market that they are happier with the lower $A. The RBA dropped their rhetoric around requiring a lower $A, implying strongly to the market that interest rate cuts may be over, sending the $A back over 74c from the mid 72c region (see chart 4). What’s far more important for local equities and especially the “yield play” as we witnessed in April, is the next major move for the bond markets. When 3 year bonds fell 66 points this year (rates up 0.66%), the banking Index corrected over 18% – see charts 2 & 3.

• An early rally in the ASX 200 was witnessed from the morning trading as high as 5727, as traders were betting for the RBA to announce an interest rate cut this afternoon at 2.30pm. The hopes turned sharply when the interest rate was left at 2%, and traders closed their ‘short’ bets, losing ~20 points in 10 minutes. The ASX 200 closed 18 points (+0.3%) higher at 5,698.

• The Australian Dollar rallied 1c higher at the same time, currently trading at US73.74c.

• CSL Limited won the race to hit the golden century this year, ending its day 2% higher at $100.77, beating Cochlear (COH) and Commonwealth Bank (CBA) in the race.

• The Banking sector closed mixed; however investors continue to allocate funds to higher yielding stocks, compared to the current low yielding Australian government bonds. Commonwealth Bank (CBA) ended 0.8% higher at $88.03.

• June Retail Sales beat analyst expectations, sending Myer (MYR) up 3.2% at $1.30 and Harvey Norman (HVN) up 6.1% at $4.72.

Really bullish, there's more to go in the reflation rally

Please enter your login details

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Enter and confirm your new password

Congratulations your password has been reset

Sorry, but your key is expired.

Sorry, but your key is invalid.

Something go wrong.

Only available to Market Matters members

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Smart Phone App

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.