Author: james Carter

Our Investing Journey Together, Clearly got Tougher, but also VERY Exciting!We started writing this report before 6am this morning, after basically no sleep, courtesy of an amazing night in the markets. The Dow closed down 588 points, BUT over 500 points above its intra day lows – yes the Dow was down over 1000 points at one stage last night! Clearly the news is full of all the reasons why equity markets are “collapsing”, but often context is forgotten for a good story. The Dow had rallied for over 3 years without a 10% correction, that is statistically extremely unusual, as opposed to what we are experiencing now, which is actually common, just more dramatic than usual. Very importantly, we believe this is a sharp correction within a bull market, NOT the start of a bear market – similar but more dramatic to what we experienced in 2011. We believe the market is simply punishing investors who were greedy / too optimistic and forgot that markets move in cycles and the odds were clearly in favour of this current corrective move.

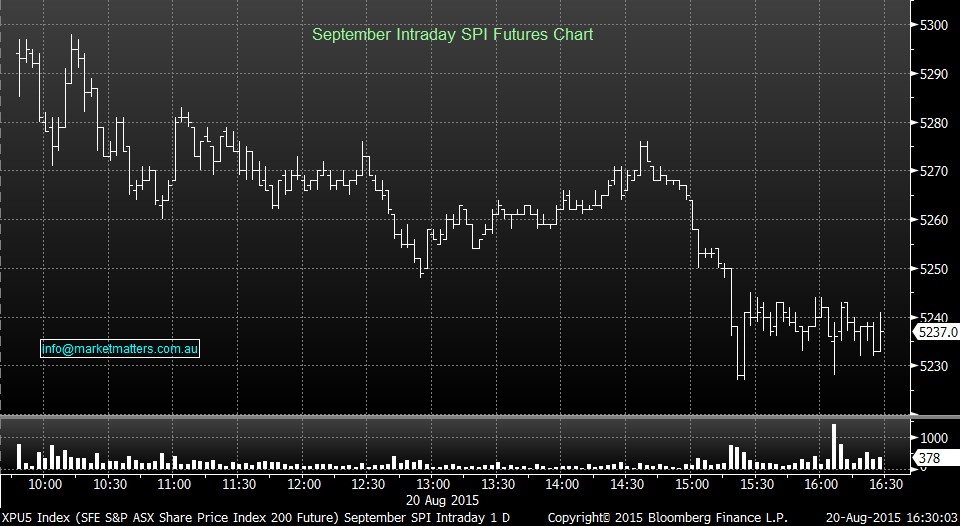

- An extremely tough day for everyone in the market today.

- The market has now fallen lower than our predicted level of 5100, due to concerns around emerging markets.

- We think the market is good value for the longer term now, and stocks like ANZ which we got more of today are good value.

- The ASX200 felt as if it was in a bottomless pit, ending on its lows, down 213 points (-4.1%) at 5,001 and wiping ~$50bn from the market.

- Not a sight of green was seen across the market map, the utilities sector, although in the red, outperformed most, in particular the Energy sector, where Santos (STO) was down 11.3% at $4.97 by close.

- At the start of the day we were considering buying STO but the momentum behind the selling kept us well and truly on the sidelines.

- As discussed in this morning’s report our target for the US S&P500 is now about 5% below today’s price (chart 1) hence no rush to chase stock today.

- We believe the banks are representing great value at these levels with ANZ paying an anticipated yield of 6.7% / 9.6% grossed up.

- Westpac (WBC) was the weakest link out of the ‘big 4’ banks, ending its day down 6.1% to $29.45.

- Bluescope Steel (BSL) blind-sided investors today, with positive earnings and rallied 8.6% to $3.67.

1 S&P500 Active contract Monthly Chart

Are the 13-year Low Commodities Close to the Bottom? Disappointing manufacturing data of China last week was the catalyst for accelerated selling in equities last week, what will this week bring? The CRB Index (Commodities Index) reached levels not seen since 2002, with oil amazingly experiencing its longest run of weekly falls in almost 30 years – see charts 1 & 2. With no fresh news since the “Weekend Report”, we thought today was an ideal time to focus closely on our aggressive trading idea of buying Santos (STO) and secondly, to look closer at our view for the US stock market over coming months. 1 Santos reported last week:

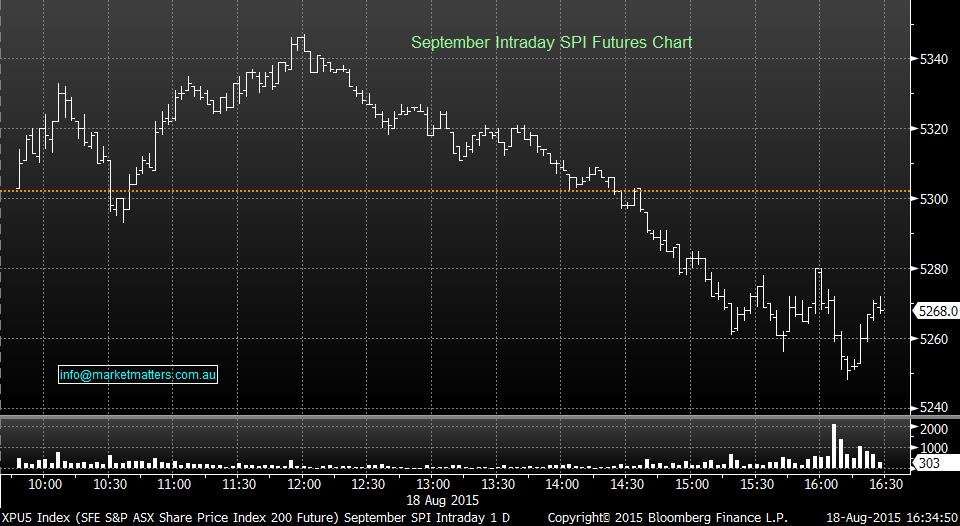

- Another shocking day with the ASX 200 in full retreat. The index finished down 74 points (1.4%) to 5,215, down 2.7% for the week.

- Following on from the selloff in the U.S. and Europe, our market was sold down. After the weak opening this morning, buying started to come back in until the Chinese PMI numbers were released: 47.1 on an expectation of 47.7.

- From there, the market collapsed on further confirmation that China was slowing.

- The banks were annihilated, but came off their lows towards the close. Commonwealth Bank (CBA) was down 56c to $75.59 after a low of $74.16. Australia & New Zealand (ANZ) closed down 79c (2.7%) to $28.34 after a low of $28.00. National Australia Bank (NAB) closed down 88c (2.8%) to $31.66 after having hit $30.80. Lastly, Westpac (WBC) closed down 83c (2.6%) to $31.37; their low for the day was $30.91.

- The Resources were mixed on the close after being slightly stronger in the morning. BHP Billiton (BHP) was down 28c to $24.10 after breaking below the $24.00 level during the day at $23.93; its low since 2009 on an adjusted basis. RIO Tinto (RIO) was stronger and finished up 11c to $49.52. It had a low on the day of $48.98 which just broke in low it had in July this year.

Best Sector – Consumer Staples

Worst Sector – Financials

Last night US equities fell over 2% as the predicated 15% correction appears to be finally underway courtesy of a trifecta of bad news – concerns over world economic growth starting with China, ongoing uncertainty with US interest rates and yet another Greek tragedy unfolding. At Market Matters we have been looking for the this correction for over 6 months and actually thought there was a good possibility of fresh 2015 highs prior to any decline but last night’s breakdown feels significant with a further 10% decline likely. The S&P500 is amazingly in its tightest trading range since 1927 so a 10% move as it breaks out of this range is very realistic – see chart 1. Today’s report title mentions “profit taking” for a specific reason because last night heavy declines in the “Fab Five” led equities lower, the strong performers of 2015 got hit hard as investors actually did lock in some profits. Growth stocks were sold, erasing $44bn from the value of these market favourites – Amazon, Apple, Facebook, Google and Netflix. Usually journalists are being very optimistic when they write “profit taking led the stock market lower” but for once its accurate. Identifying our equivalent stocks to the US’s “Fab Five” is far harder but some stocks that catch our eye which have been strong this year to-date, while the ASX200 is down over 2%, are:

- A sea of red was experienced in the ASX200 today, losing 91 points (-1.7%) to 5,288.

- The banking sector led the way in today’s weakness, Commonwealth Bank (CBA) remained to be the weakest link post trading ex-dividend, finishing the day down 2.7% lower at $76.15.

- In the Resources front, BHP Billiton (BHP) lost 3.1% to $24.38, following further weakness with our neighbour, China.

- A preference was established between the major supermarkets today – where buying was seen in Wesfarmers (WES) +1.2% at $40.86 and Woolworths (WOW) sold off, down 2.5% at $26.57.

Best Sector – Consumer Staples

Worst Sector – Energy

The ASX200 has corrected 11.6% since the dizzy heights of March, when investors were simply chasing stocks for yield without any thought to capital depreciation. Most of this move has unfolded exactly as we anticipated and fortunately we maintained significant cash holdings during this correction. Yesterday we started deploying some of these funds back to work. Inevitably when holding any stocks during a significant correction, the likelihood is some positions will be underwater and we are experiencing this with some stocks below, but overall our cash position and stock selection still has us way ahead of the crowd. A number of points must be clearly addressed as an investor on a regular basis:

We are Liking 2 out of 3 “Panic Areas” at Current Levels

• The ASX 200 was hit with the proverbial ‘4 b 2’ this afternoon, finishing the day down 65 points (-1.2%) to 5,303.

• The catalyst this time was the selling in the banks, after ratings agency, Fitch issued a statement which read in part that they consider a further increase in capital will be required by Australian Banks.

• Commonwealth Bank (CBA) was ex dividend $2.22 today and closed down $4.36 to $76.91. National Australia Bank (NAB) closed down 50c to $31.76, Westpac Bank (WBC) was down 28c to $31.66 and Australia New Zealand Bank (ANZ) closed down 55c to $28.97.

• Fortescue Metals (FMG) continued its rally, despite media speculation of an asset sale was watered down. FMG closed 7.9% higher at $1.985, where we took profit in selling our option position today.

• Challenger Group (CGF) reported its earnings and was well received, ending its day up 2.5% at $7.08.

Really bullish, there's more to go in the reflation rally

Please enter your login details

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Enter and confirm your new password

Congratulations your password has been reset

Sorry, but your key is expired.

Sorry, but your key is invalid.

Something go wrong.

Only available to Market Matters members

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Smart Phone App

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.