Author: james Carter

Looking at the ASX200’s five best stocks of the last month

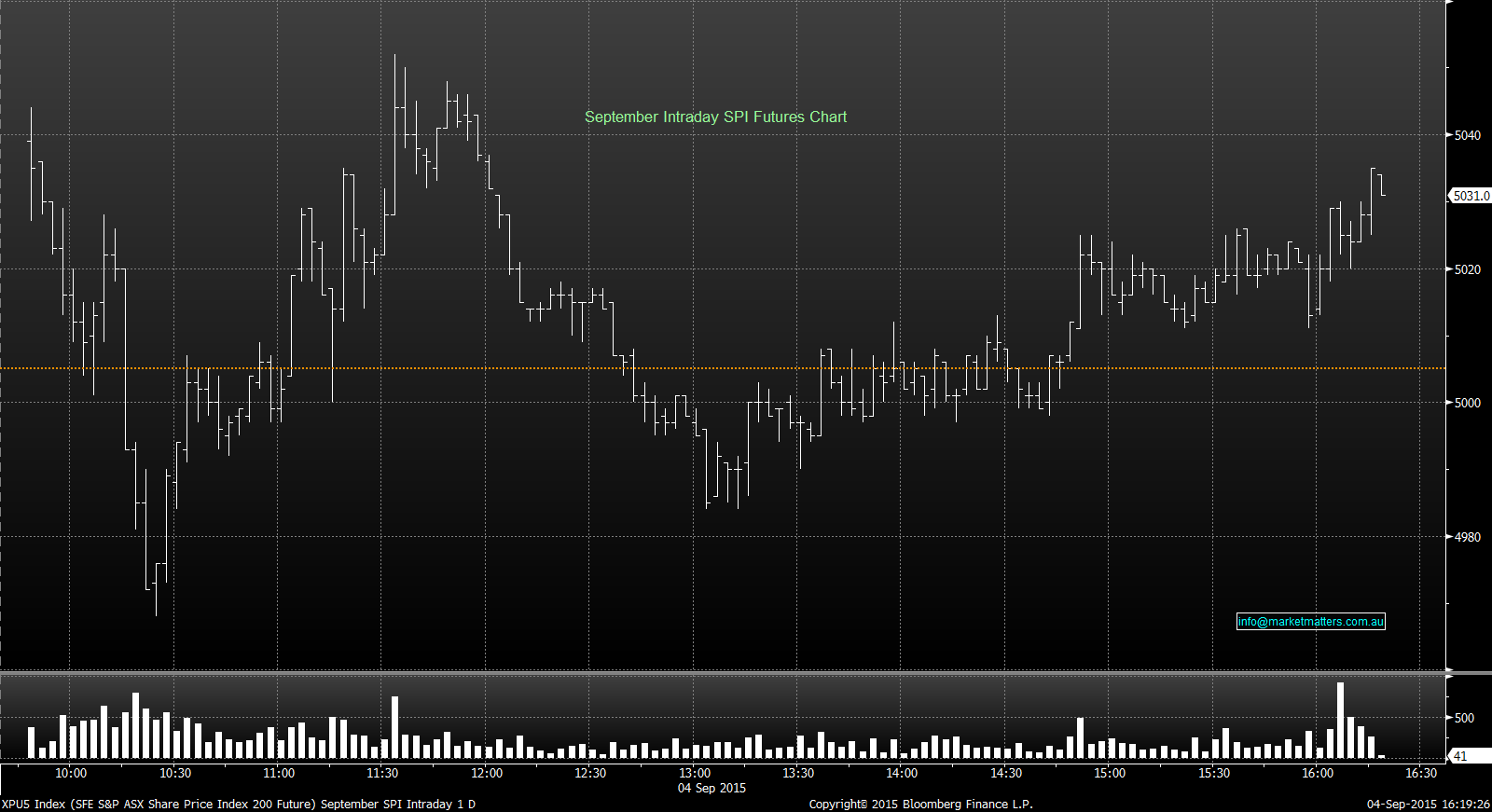

The ASX 200 had a quiet, but the usual roller coaster ride today finishing the day down 10 points (-0.2%) at 5,030, after trading as low as 4,973.

OverviewAs we have been pointing out, markets repeat themselves in many ways including chart patterns, price and time measures, and seasonal statistics. We have just experienced the worst month in over 3 years and now it’s September, historically the weakest month for US equities going back to 1927.We believe that US equity markets are now due for 4/5 weeks of choppy price action into October prior to forming a good bottoming pattern and a classic rally into Christmas. Whether the US Indexes or the ASX200 actually make fresh 2015 lows is uncertain but, as discussed in our weekend report, if we witness any fresh lows the likelihood is that they will be brief.

- A choppy and quiet session was experienced in the ASX 200 today as expected. The broader market had a solid open, though it weaved in and out of positive terrirory for the day, before it closed 13 points higher (+0.3%) at 5,040.

- With no surprise, BHP outperformed the benchmark and closed 1.5% higher at $24.69. Its rival, RIO also outperformed the broader market, ending its day 1% higher to $49.76, whilst Fortescue Metals (FMG) lost 1.6% to $1.86.

- Santos (STO) continues to slide, down 3.3% to $4.38 for the day, making it down 17.2% for the week and down 40.1% since August. Concerns of a capital raising continues to mount with this company.

- In the Mergers and Acquisitions (M&A) area, Echo Entertainment rallied 2.2% higher to $4.74 after the NSW government approved its suitor Genting, to increase its current RGP stake from 6.6% to 23%.

- Please watch out for the weekend report.

The markets continue in their current state of uncertainty with few participants wanting to take significant overnight or new investment risk. The fading of our market yesterday and the US markets (although to a much lesser degree) overnight illustrates this risk aversion.

- A total reverse of yesterday was witnessed in the ASX 200 today, having opened strong and on its highs early in the morning, investors seemed to have lightened their positions and took risk off the table as the markets in China began their long weekend.

- The Banking sector was damaged in this volatile market; Commonwealth Bank lost 2.3% to $71.97 and National Australia Bank (NAB) down 2.5% to $29.93.

- Fortescue Metals (FMG) was the diamond in the Iron Ore Rough, having rallied 1.9% to $1.89, while BHP closed 1.3% lower at $24.32.

- Mergers and Acquisitions remain to be present in the Aussie market, with speculation that Woodside Petroleum (WPL) is looking to make a $10.2b play and merge with OilSearch (OSH). WPL closed 2.1% lower at $30.46, while OSH ended 3.6% higher at $6.89.

Best Sector – IT

Another fascinating day in the markets! Price action continues to support our belief that the Australian market is in a strong ‘buy’ zone. As reported on Tuesday, our analysis of past time cycles adds additional support to our current view of the market.

- The ASX 200 was surprisingly strong after an early downturn of 70 points this morning. The index finished 5 points higher at 5,101, a 1.7% rally from its day’s low.

- Following on from last night’s weakness, China didn’t disappoint and opened down 4.7%, but steadily recovered. By the lunchtime close, it was up 0.3% – It has been reported that China’s state-backed funds were stabilising the markets ahead of a major military parade due tomorrow. China will be on holiday for the rest of the week.

- Energy stocks were hit hard after the weakness last night. Origin Energy (ORG) was down 37c (-4.5%) to $7.81 and Woodside Petroleum (WPL) closed down 52c (-1.6%) to $31.10.

- The Australian GDP figures were released this morning which showed that the economy is growing at its slowest rate in four years. The ABS has said gross domestic product (GDP) grew 0.2 per cent in the three months to the end of June, compared with 0.9 per cent in the first quarter.

Best Sector – Health Care

Well, another large fall on the US markets overnight to continue the ‘fear element’ currently in investors’ mind. We mentioned recently that the complacency around the recent stock market plunge made us at Market Matters feel there was more to come. Certainly the extreme blow-out in volatility over the past 10 days or so takes time to work its way through the market with the probability of sometimes wild price oscillations. The ability to stand back from these often emotionally driven gyrations and properly assess the ‘position of the markets’ is what really matters right now!

- The ASX 200 had a great start, opening near its day’s high, only to fade gradually and lose 110 points (-2.1%) to 5,096 – a move that seems to be the new norm!

- Macroeconomic Highlights from today –

- The RBA voted well with consensus, leaving cash rates unchanged at 2% for September.

- China Manufacturing PMI in August in line with consensus and weaker from the previous month, at 49.7.

- The gaming sector, particular those exposed in Macau were weak as Official Beareau Stats reported a 26.4% dive in its 2Q GDP. Crown Resorts (CWN) lost 3.3% to $11.06.

- In the banking sector, the regionals underperformed, Bank of Queensland (BOQ) lost 3.1% at $12.28 and Bendigo & Adelaide Bank (BEN) down 4.2% at $10.51.

- Fortescue Metals (FMG) was the major underperformer in the Iron Ore sector, down 6% at $1.795.

- In the consumer discretionary sector, Myer (MYR) is currently in a trading halt, following its announcement of a profit 21% below last year’s and is currently underway for a share placement at 94c a share (28.7% below previous trade at $1.21).

- Qantas (QAN) was well bought today, following a broker report of a potential share buy-back of up to $1.5b over the next two years. QAN closed 3.3% higher $3.47.

Best Sector – Industrials

Really bullish, there's more to go in the reflation rally

Please enter your login details

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Enter and confirm your new password

Congratulations your password has been reset

Sorry, but your key is expired.

Sorry, but your key is invalid.

Something go wrong.

Only available to Market Matters members

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Smart Phone App

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.