Author: james Carter

*NB There will be no report tomorrow as we celebrate Australia Day

- A better day in the Australian market after a good lead last night, especially with the strong move up in oil. The ASX 200 closed today up 52 points (+1.1%) to 4,916. For the week we managed to scrape up 23 points or 0.5%.

- As mentioned previously the oil price sparked a revival in resources and energy stocks. BHP Billiton (BHP) showed signs of recovery with its price reaching a high of $15.44 and closed up $1.06 (+7.5%) to $15.26. Market Matters were happy to see this rally given our buy alert yesterday predicting this recovery . RIO Tinto (RIO) had a high of $39.95 but closed slightly lower at $39.65 however still up $1.29 or 3.4%.

- The banks were again on the sell side, with perhaps funds selling to pay for the switch into resources. Commonwealth Bank (CBA) closed down 25c to $76.56, Australia New Zealand Bank (ANZ), which had been suffering all week on suspicion the bank could be cutting its dividend, managed to pick up and closed at $23.35, up 24c or 1%. National Australia Bank (NAB) was quiet, up 10c to close at $26.92. Finally Westpac (WBC) closes up just 4c to $29.93.

- On the news front, Medicare (MPL) surprised the market with an upgrade to its full year profit forecast. Medibank Private says its full year operating profit is expected to exceed $470 million, $100 million above its previous guidance. The price jumped on the opening to a high of $2.71 however it slipped back to close up 26c (+11%) to $2.50.

Best Sector – Energy

Worst Sector – Prop Trusts

Today we have restructured how we present the morning report so will look forward to your feedback.

- The World today seemed a better place with the ASX 200 index managing to lift itself out of the gloom for a while this morning. At its best, the index was up 87 points with all sectors firing. Towards the end of day however, we received the customary weakness and the market closed only 22 points higher (+0.5%) at 4,864.

- The resources were better during the day, however they also succumbed to the weakness in the market in the afternoon. RIO Tinto (RIO) had a high of $39.25 early on, but finished the day up 61c to $38.36. BHP Billiton (BHP) however finished down, but only 1c lower at $14.20.

- Origin Energy (ORG) was buoyed by a report from the company Managing Director Grant King “Origin is confident that its robust financing arrangements and cash flows from existing businesses position the company well to withstand a prolonged period of low oil prices,” The stock rose to a high of $3.98 before finishing the day up 23c (+6.7%) to $3.69.

- The banks were sold down in afternoon trade with CBA closing down 80c to $76.81, after reaching a high of $79.16. ANZ continued to be the weakest, with the stock closing down 39c to $23.11 after briefly touching $23.95 earlier the weakness was the follow on effect from a bank analyst -Morgan Stanley forecasting a cut to its full year dividend.

Best Sector – Telcos

Worst Sector – Financials

Four stocks / markets that are catching our eye today

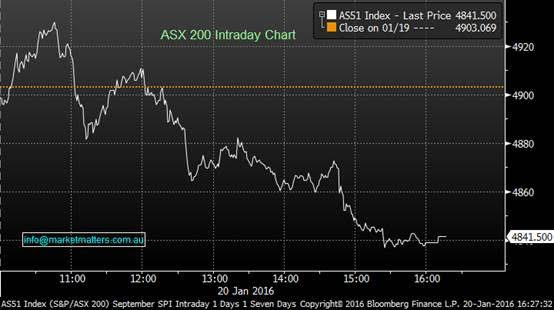

- A poor session on the ASX today with the index getting hit after the first hour of trade to close down -61pts or -1.26% to 4841. Overseas selling, particularly in the US Futures market seemed to be the catalyst while we also had some ongoing chatter about Chinese growth after the IMF lowered their forecast overnight.

- ANZ closed at its lowest level since 2013 as Morgan Stanley questioned the sustainability of their current dividend. ANZ was off -4.43% to $23.50

- BHP released Q4 2015 production numbers this morning, missing analysts’ expectations. The stock was down -3.53% at $14.21

- On the flip side, Credit Corp (CCP) had a good day, adding 4.31% – proving its defensive qualities

Best Sector – Consumer Staples

Worst Sector – Energy

Are we heading for a worldwide recession is a question that nobody knows the answer to, but there is no doubt as an investor if you read today’s press; concerns must be growing rapidly.

- It was a pleasant breath of fresh air today, as investors saw the broader market close in positive territory, ending up 44 points (+0.9%) at 4,903.

- It was a soft start earlier in the session however, volatility subsided after the China GDP being released with no major surprises, just off from analysts’ expectations and helped push some buying today.

- Macquarie Group (MQG) rallied well for the financial sector, up 2% to $73.91, while WBC closed 1.3% higher at $31.18

- The Gold sector outperformed the broader market, with Regis Resources (RRL) rallying 7.1% higher at $2.56 and Newcrest (NCM) up 3% at $13.24.

- In the Consumer discretionary sector, Woolworths (WOW) gave back some of its losses down 1.3% to $23.35, along with Wesfarmers ending 1.1% lower to $39.70.

Best Sector – IT

Worst Sector – Energy

Again looking closely at one of the market “keys” – oil.

- It was no surprise the underperformance witnessed in the ASX 200 today, although the broader market rallied well from its lows of 4,803 to end the day at 4,858.

- Both the banks and miners were the contributors to lead the ASX200 into the red sea, NAB was the weakest link of the big 4, ending 1.1% lower at $26.69, while BHP lost further ground today, down 2.9% at $14.63.

- The consumer staples sector was the hot topic of the day, with Woolworths (WOW) announcing it plans to cut its underperforming asset, Masters. WOW closed 4.4% higher at $23.65.

- This week on specific stocks, will likely focus on the Iron Ore sector, with RIO releasing its fourth quarterly production tomorrow morning and BHP with its result this Friday.

Best Sector – Consumer Staples

Worst Sector – Energy

Really bullish, there's more to go in the reflation rally

Please enter your login details

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Enter and confirm your new password

Congratulations your password has been reset

Sorry, but your key is expired.

Sorry, but your key is invalid.

Something go wrong.

Only available to Market Matters members

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Smart Phone App

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.