What you need to know about Sonic Healthcare Limited (ASX: SHL) acquisition and cap raise

Stock

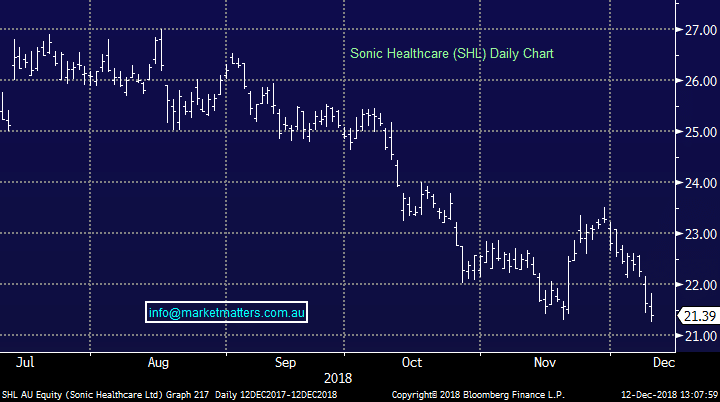

Sonic Healthcare (ASX: SHL) $21.39 as at 12/12/2018

Event

The largest ASX-listed diagnostic imaging facilities group (Sonic Healthcare (ASX: SHL)) is about to get bigger after it went into a trading halt to announce a US$540 million ($750 million) acquisition and a large capital raising this morning. Sonic Healthcare Limited (ASX:SHL) struck a deal to acquire US-based Aurora Diagnostics, which will make it the third largest player in the US market and expand the proportion of revenue from that country to 26% from 20%.Sonic Healthcare (ASX: SHL) Chart

The group has also announced it will undertake a fully-underwritten $600 million share placement to institutional and sophisticated investors along with a non-underwritten share purchase plan (SPP) for existing shareholders, which is aimed to raise a further $100 million for the deal.

The new share sale into the placement is priced at $19.50, or an 8.8% discount to Sonic’s share price on Tuesday, while shareholders participating in the SPP will get the lower of this price or the five-day volume weighted average price of the stock up to the closing date of the SPP (less a 2.5% discount).

The acquisition is expected to be 3% earnings per share (EPS) accretive even if you included the extra shares issued under the placement and doesn’t include any revenue or cost synergies from merging Aurora with Sonic.

Sonic believes it will have opportunities to cross-sell its clinical pathology services and Aurora’s anatomical pathology services but didn’t provide any details on the value of the synergies.

Management pointed out that Aurora generated a proforma revenue of US$310 million and an earnings before interest, tax, depreciation and amortisation (EBITDA) of $59 million.

The other investment metrics for the deal also appear appealing on first blush. The acquisition is tipped to generate an attractive return on invested capital (ROIC) of 9% to 10% in the first year and is priced on a 9.2 times pro-forma EBITDA.

The question is whether investors should be excited by the deal with SHL’s share price falling 12% over the past six months when the S&P/ASX 200 (Index:^AXJO) (ASX: XJO) index is down 7.5%.

The relatively defensive nature of the sector should provide some shelter during the market turbulence, although that doesn’t seem to have worked with shares in other health facilities operators also swept up in the recent market meltdown.

This includes the Ramsay Health Care Limited Fully Paid Ord. Shrs (ASX: RHC) share price, Healius Ltd (ASX: HLS) and Monash IVF Group Ltd (ASX: MVF) share price.

The group has also announced it will undertake a fully-underwritten $600 million share placement to institutional and sophisticated investors along with a non-underwritten share purchase plan (SPP) for existing shareholders, which is aimed to raise a further $100 million for the deal.

The new share sale into the placement is priced at $19.50, or an 8.8% discount to Sonic’s share price on Tuesday, while shareholders participating in the SPP will get the lower of this price or the five-day volume weighted average price of the stock up to the closing date of the SPP (less a 2.5% discount).

The acquisition is expected to be 3% earnings per share (EPS) accretive even if you included the extra shares issued under the placement and doesn’t include any revenue or cost synergies from merging Aurora with Sonic.

Sonic believes it will have opportunities to cross-sell its clinical pathology services and Aurora’s anatomical pathology services but didn’t provide any details on the value of the synergies.

Management pointed out that Aurora generated a proforma revenue of US$310 million and an earnings before interest, tax, depreciation and amortisation (EBITDA) of $59 million.

The other investment metrics for the deal also appear appealing on first blush. The acquisition is tipped to generate an attractive return on invested capital (ROIC) of 9% to 10% in the first year and is priced on a 9.2 times pro-forma EBITDA.

The question is whether investors should be excited by the deal with SHL’s share price falling 12% over the past six months when the S&P/ASX 200 (Index:^AXJO) (ASX: XJO) index is down 7.5%.

The relatively defensive nature of the sector should provide some shelter during the market turbulence, although that doesn’t seem to have worked with shares in other health facilities operators also swept up in the recent market meltdown.

This includes the Ramsay Health Care Limited Fully Paid Ord. Shrs (ASX: RHC) share price, Healius Ltd (ASX: HLS) and Monash IVF Group Ltd (ASX: MVF) share price.