ASX hits 3 months low, resources drag, tech’s bounce (EHL) **International Alert – Global ETF Portfolio – Buy QQQ US**

WHAT MATTERED TODAY

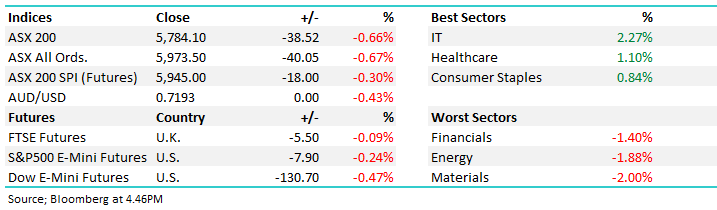

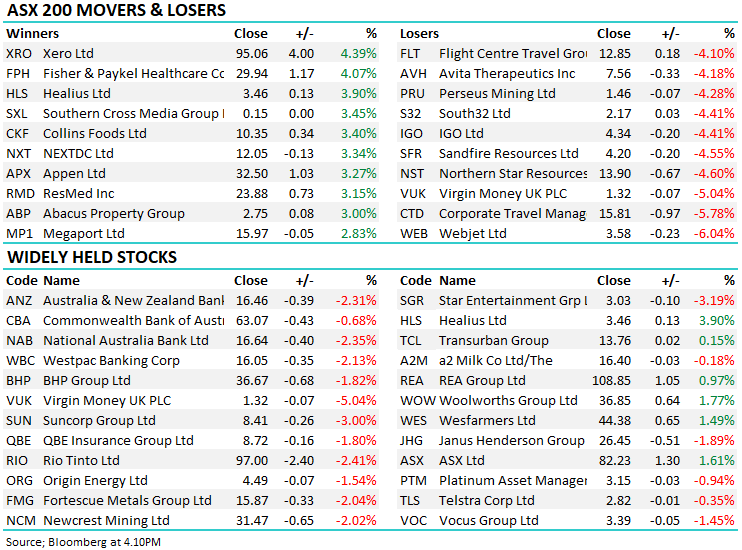

The majority of stocks closed lower today led by the Material Sector which fell 2% as recent strength was sold into. Concerns around the outlook for global growth as virus numbers spiral higher, especially in Europe the obvious catalyst however we’ve also seen strength in the $US which has provided another headwind. The sector has been strong in recent months and while we think it’s ‘due a rest’ in the short term, we remain positive on the outlook for commodities in the medium term. The IT stocks were the clear winners today, the sector up 2.27% following a strong reversal in the Nasdaq overnight, from a technical perspective, the Nasdaq / tech stocks now look bullish.

The ‘re-opening trade’ took a hit today, Webjet (WEB) the biggest drag in the ASX200 followed by Corporate Travel (CTD), both fell around 6% which highlights the volatility we’re likely to see around these names as outbreaks then containment ebb and flow. We were of the opinion that re-opening in Australia was a catalyst for some of these stocks to improve, however clearly there’s more to play out on the global stage.

Asian markets were mostly lower today while US Futures were higher early, before tapering off into our close. Our market actually did pretty well to close where it did, given our futures were off -57pts this AM + US Futures slide another 0.4% during our time zone. Still, the ASX closed at a 3 month low today, approaching the bottom of its trading range - which sits at 5700.

By the close, the ASX 200 was down -38pts / -0.66% to 5784. Dow Futures are trading down -130pts/-0.47%

ASX 200 Chart

ASX 200 Chart

CATHCING MY EYE

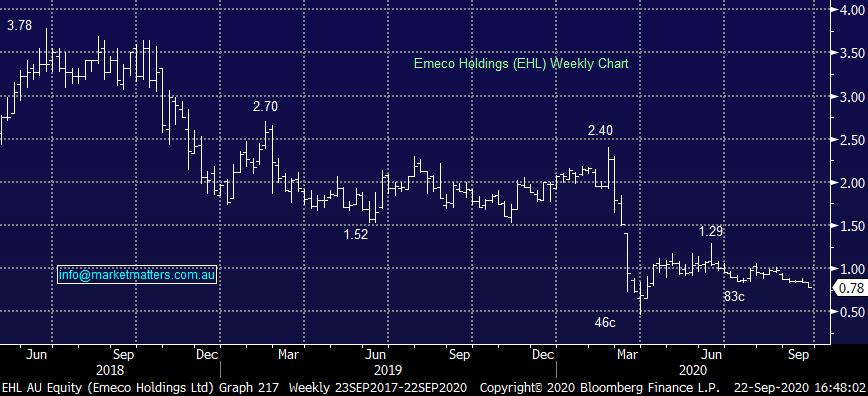

Emeco (EHL) -6.59%: traded below the placement offer price for much of the entitlement offer period, and as a result the company received applications for $6.5m worth of shares from retail holders. This has left the underwriters with an additional ~37m shares than they had hoped, and which look to be getting sold on market. It’s a pretty reasonable looking for a new home in a stock that trades around 3m a day so we suspect pressure will continue for now. We do still like EHL – the shares will wash through and the balance sheet is substantially improved as a result of the raise.

Emeco (EHL) Chart

BROKER MOVES

· Magellan Financial Raised to Add at Morgans Financial Limited

· Panoramic Resources Cut to Underperform at Macquarie

· Newcrest Raised to Neutral at Macquarie; PT A$35

· Australian Pharma Cut to Sell at Bell Potter

· AMP Raised to Buy at Morningstar

· Jumbo Interactive Cut to Neutral at Evans & Partners Pty Ltd

· Laybuy Group Rated New Speculative Buy at Bell Potter

OUR CALLS

Growth Portfolio: We sold Oz Minerals (OZL) & Macquarie (MQG) today, buying Appen (APX) and Megaport (MP1).

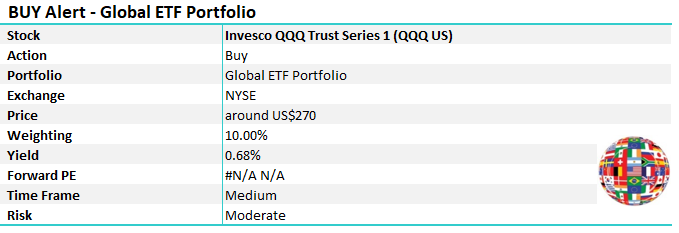

***International Alert – Global ETF Portfolio***

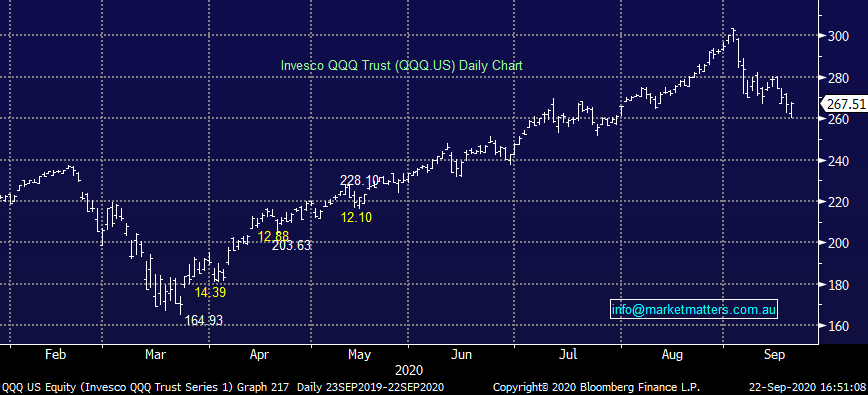

Invesco QQQ Trust (QQQ US) Chart

Major Movers Today

Have a great night

James / Harry & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.