A deeper dive into the Woolworths (WOW) Buy Back

Woolworths (WOW) is a popular income stock even though it’s expected to yield just 3.19% in FY19 and trades on a relatively expensive est. P/E of 25x. Investors generally pay a high multiple for either growth in earnings, predictability / visibility on earnings or a combination of both. In the case of Woolies, earnings are forecast to grow at a steady 6% for the next 3 years which shows some growth and of course they sell mostly staples, things that we need to buy each week so the predictability of earnings is high. Factoring in the implied 6% growth it means WOW trades on around 23x 2021 earnings.

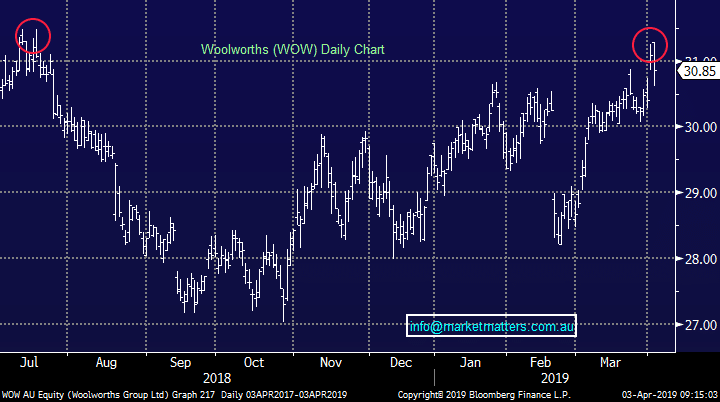

To put those P/E multiples into perspective, over the past 5 years WOW has traded on an average P/E of 18.1x and at no time during that period has WOW been more expensive than it is today. The obvious question being, is this P/E premium justified?

On Monday they issued a market update and within it there were two bits of positive news, and the share price rallied more than 2% on the day.

1. They announced the closure of ~30 BIG W stores out of their 183 strong network along with two distribution centres. The reason being that BIG W’s turnaround is taking longer than expected with WOW expecting an EBIT loss of $80-$100m in FY 19 which is above market expectations and only down marginally from the $110m loss in FY18. The costs to exit these stores will be about $370m. While the underlying reasons for the closures are not positive - the decisive action is, while it also reduces the likely losses in outer years which prompts earnings upgrades.

2. They announced a $1.7 billion off-market buy-back

In terms of the buy-back, Shareholders who own Woolies shares, or buy them before the close of trade, Thursday 4th April, can participate and the buy-back closes after the 45 day rule allowing for the benefits of franking to be accrued. Just to recap that rule, a SMSF must hold company shares for at least 45 days (plus the day of purchase and day of disposal) to be entitled to franking credits, however this rule does not apply to individuals where the total franking credit entitlements for that financial year are below $5,000.*As always, consult with your accountant*

Shareholders have the option to tender stock into the deal at between a 10-14% discount to the market price – the deal will most likely be priced at a 14% discount comprising a $4.79 capital component and the rest paid out as a fully franked dividend.

If we assume a 14% discount is applied to Tuesday's close of $30.85, the buy-back would be priced at $26.53 consisting of a $4.79 capital component and a $21.74 fully franked dividend. A $21.74 fully franked dividend is worth $31.05 in a zero tax environment plus the $4.79 capital component, or a total value of $35.85 – which equates to a $5 / 16.2% uplift. The impact on other tax rates are shown below.

Source: Market Matters

WOW trades ex-entitlement on today. The offer period opens on the 16th April and closes on the 24th May, all tenders need to be submitted by 7pm on the 24th May before the buy-back price and scale-back are completed on the 27th May. Proceeds would be paid on the 30th May.

In short, the offer looks good for those holders in a zero tax environment, or those with large capital gains embedded in current holdings.

In reality, there is likely to be a large scale back applied to tendered shares meaning that we have to be comfortable holding Woolies from here.

While the action taken on Big W is a positive, and the buy-back is good for some, this doesn’t change the fact that sales are struggling, not just in WOW but also for Coles. The 1H results for Woolies showed they are going backwards in nearly every division, while both Woolies and Coles are experiencing higher costs in an environment of falling prices. WOW now trading on a very ritzy PE premium to the market of >45% leaving very little room for error.

Both Supermarket operators (WOW/COL) have now made it crystal clear themselves via bearish commentary that things are getting tougher with consumer sentiment and the retail landscape facing a number of headwinds. At MM we don’t expect a lagging Coles to sit back, nor Aldi and IGA for that matter. Worth also considering that Australia is the second most concentrated grocery market in the world behind NZ and competition is likely to become more aggressive with all players investing further, especially Coles, and ALDI, Costco, IGA, AMZN, Kaufland and potentially Lidl.

Woolworths (WOW) Chart

Source: Market Matters

WOW trades ex-entitlement on today. The offer period opens on the 16th April and closes on the 24th May, all tenders need to be submitted by 7pm on the 24th May before the buy-back price and scale-back are completed on the 27th May. Proceeds would be paid on the 30th May.

In short, the offer looks good for those holders in a zero tax environment, or those with large capital gains embedded in current holdings.

In reality, there is likely to be a large scale back applied to tendered shares meaning that we have to be comfortable holding Woolies from here.

While the action taken on Big W is a positive, and the buy-back is good for some, this doesn’t change the fact that sales are struggling, not just in WOW but also for Coles. The 1H results for Woolies showed they are going backwards in nearly every division, while both Woolies and Coles are experiencing higher costs in an environment of falling prices. WOW now trading on a very ritzy PE premium to the market of >45% leaving very little room for error.

Both Supermarket operators (WOW/COL) have now made it crystal clear themselves via bearish commentary that things are getting tougher with consumer sentiment and the retail landscape facing a number of headwinds. At MM we don’t expect a lagging Coles to sit back, nor Aldi and IGA for that matter. Worth also considering that Australia is the second most concentrated grocery market in the world behind NZ and competition is likely to become more aggressive with all players investing further, especially Coles, and ALDI, Costco, IGA, AMZN, Kaufland and potentially Lidl.

Woolworths (WOW) Chart