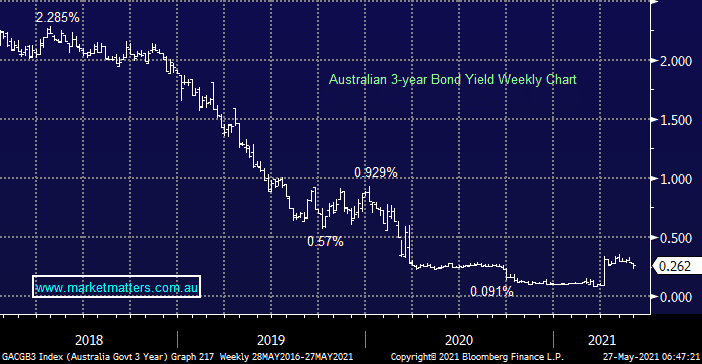

The post COVID picture for interest rates is very clear, it’s a case of when not if they are going to start rising. We believe the evidence is clear on many levels, locally we already have the large banks edging their 3 & 4-year fixed mortgage rates higher while the critical 3-year bond yield has doubled since February. Overseas we’ve seen the likes of New Zealand and Canada signal their intention to raise rates next year although central banks do feel very nervous about slowing the recovery, often implying a little inflation is preferable to turning off the stimulus taps too early. The elephant in the room is always the Fed when it comes to rates and markets are expecting them to start hiking a year earlier than they were just a few months ago, again no great surprise when we consider the Bank of England for example has switched its rhetoric from rate cuts into 2022 to hikes.

Initially the aggressive bond buying and other related stimulus will be turned off first with significant rate hikes probably still a few years away but markets look into the distance, as opposed to the present. July is D-day for the RBA as they decide whether to extend their bond buying spree (QE) either way the clock is ticking, Canada has already reduced its purchases and that’s my “Gut Feeling” for Phillip Lowe’s direction into next financial year. Some less followed countries such as Iceland are further down the path having already started hiking while Norway is close, portfolio construction must remain cognisant that rates are going up into 2022/23 even if its bordering on old news.