Gold a standout, Property joins in as house prices rise 6.2% for the year (NST)

WHAT MATTERED TODAY

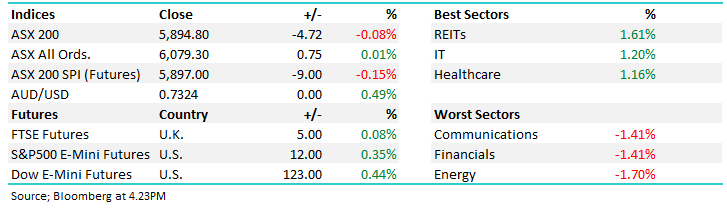

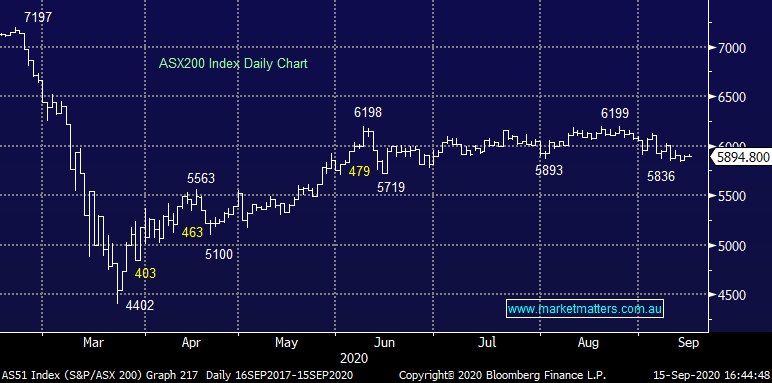

A fairly lacklustre session today with the market oscillating in a +/-35pt trading range before closing down a few ticks. A bounce back in some of the technology stocks one obvious trend however the biggest influence from an index perspective was weakness across the banks, the big 4 taking 14points from the index. Gold also strong ahead of a number of central bank meetings this week, a theme Harry covers below while it was the property sector than really shone thanks to decent / less bad housing numbers.

Asian markets were mostly higher today, ditto for US Futures which did okay during our time zone.

By the close, the ASX 200 was down -4pts / -0.08% to 5894. Dow Futures are trading up +123pts

ASX 200 Chart

ASX 200 Chart

CATHCING MY EYE

Gold Stocks: buying returned to the gold names today after they had, for the most part, tracked lower over recent weeks. Silver Lake (SLR) was the best of the large caps adding more than 8%, but some of the more speculative names enjoyed larger moves. The buying comes despite a strong Aussie dollar which continues to see support, trading near 12 month highs – given gold prints in USD, a strong AUD weighs on earnings for local producers. Gold is back in the spotlight though as a number of central banks around the world meet this week – Bank of Japan, Bank of England and most importantly the US Fed will all make calls while the RBA printed the minutes from their meeting 2 weeks ago. The view remains that central banks have been given almost free reign to drive inflation higher – rates will remain at or near 0 over the medium term while a number of other measures are being deployed in an attempt to kickstart inflation. Gold enjoys negative real rates (when inflation runs above bond yields) and with the near-term news flow expected to be positive for the commodity, equities benefitted. We own a small position in Newcrest (NCM) in the Growth portfolio, with plans to add to it.

Northern Star (NST) Chart

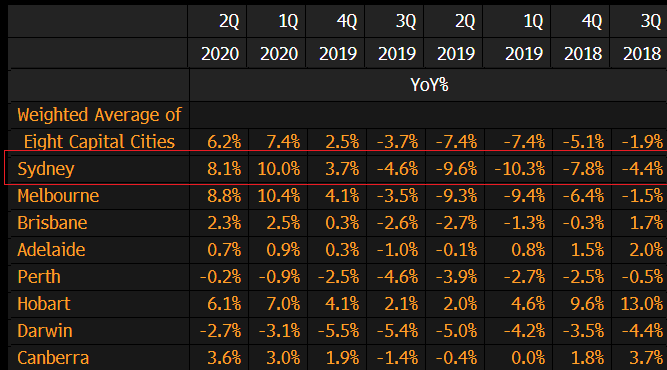

House Prices: Data out today showed that house prices fell in all capital cities apart from Canberra in the June quarter, however looking at the year on year stats below they show prices actually rose 6.2% through the year to the June quarter with prices higher in all capital cities except Perth and Darwin. Obviously, Job Keeper / mortgage holidays are having an influence here however looking at the data below, it’s not that concerning at this stage, although we’ll more clarity around the real state of housing in the months ahead.

Source: Bloomberg

BROKER MOVES

· Credit Corp Cut to Neutral at Macquarie; PT A$18.50

· BHP Raised to Buy at Goldmans; PT A$40.10 **They increased their Iron Ore Forecasts** as an aside Macquarie are No 1 on BHP and have a Outperform (Buy) and $44.00 PT

· Harvey Norman Raised to Outperform at Credit Suisse; PT A$5.01

· Wesfarmers Raised to Outperform at Credit Suisse; PT A$51.59 – first analyst above $50 I can see for WES (Jefferies at $50 even)

OUR CALLS

No changes to the portfolios today.

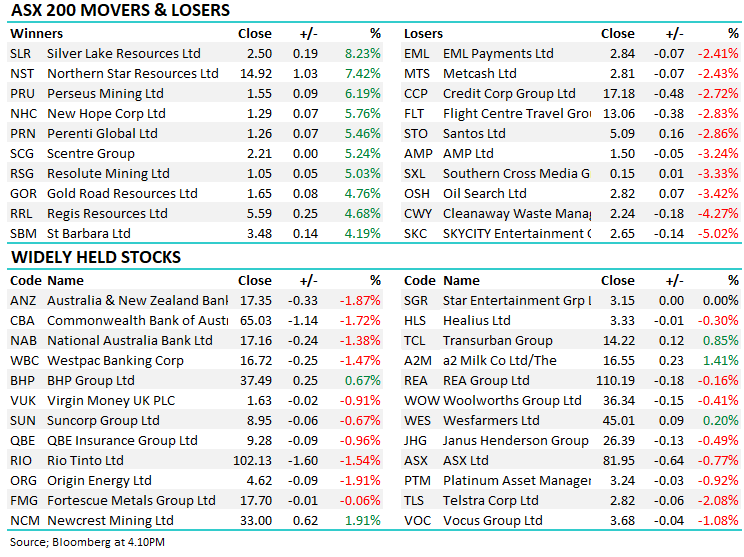

Major Movers Today

Have a great night

James / Harry & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.