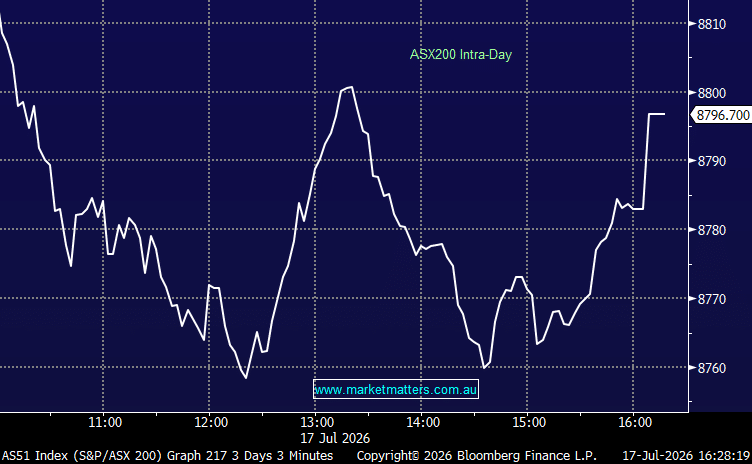

The ASX was lower today with a sharp sell-off across gold, copper and lithium stocks overwhelming solid gains in energy, utilities and communications. The index recovered from its session low but still ended the week marginally lower as renewed fighting in the Middle East, rising oil prices and the prospect of higher-for-longer interest rates weighed on risk appetite.

Materials were the clear pressure point, falling almost 3% as BHP declined for a second session and gold miners were hit by bullion slipping below US$4,000/oz. Asian markets were down 2-4% today, amplifying the negativity towards resources.

- ASX 200: -43.97pts / -0.50% to 8,796.70

- AUD/USD: 0.6990 / -0.10%

- Best sectors: Utilities +1.77%, Energy +1.66%, Communications +1.62%

- Worst sectors: Materials -2.91%, Information Technology -1.60%, Healthcare -0.34%

- AMP Ltd (AMP) +6.32% to $2.02 extended its strong run following Thursday’s earnings update, taking its five-day gain to more than 20%. The market continues to respond positively to guidance for first-half underlying profit of $170m–$180m, supported by its China partnerships and carried interest.

- Brambles (BXB) +3.46% to $19.44 was among the strongest large-cap performers, while Woodside Energy (WDS) +3.29% to $30.46 rallied as Brent crude climbed toward US$85/bbl.

- Coles Group (COL) +2.88% to $23.21 gained after ending discussions with TPG Capital over a potential acquisition of Greencross. The proposed deal had received negative investor feedback and arguing Coles’ balance-sheet strength could instead support capital management.

- Amcor (AMC) +2.84% to $63.77, Telstra Group (TLS) +2.65% to $5.04 and Bega Cheese (BGA) +2.52% to $6.10 also advanced as investors favoured defensive and domestically focused earnings.

- Domino’s Pizza Enterprises (DMP) +2.50% to $17.62 continued its recovery, taking its five-day gain to around 9.5%, while Ingenia Communities Group (INA) +2.39% to $4.29 and Generation Development Group (GDG) +2.30% to $3.56 also finished firmly higher.

- BHP Group (BHP) -2.71% to $57.54 declined for a second consecutive session as softer FY27 copper guidance, strike action at Port Hedland and valuation concerns weighed. UBS trimmed its target from $60 to $59 and retained a Neutral rating, arguing much of the strength in commodity markets is already reflected in the share price.

- Rio Tinto (RIO) -2.39% to $160.95 also weakened, while South32 (S32) -3.47% and Mineral Resources (MIN) -2.61% were caught in the broader materials sell-off.

- Gold stocks were heavily sold as bullion fell below US$4,000/oz. Westgold Resources (WGX) -7.05% to $4.35, Genesis Minerals (GMD) -7.18% to $5.56, Ora Banda Mining (OBM) -7.41% to $1.00 and Regis Resources (RRL) -8.44% to $5.64 all declined sharply.

- Regis Resources (RRL) -8.44% to $5.64 was pressured by FY27 guidance that fell short of expectations, while Evolution Mining (EVN) -4.27% to $10.73 and Northern Star Resources (NST) -4.14% to $19.24 were also caught in the sector-wide rout.

- Uranium and emerging-resource names remained under pressure. IperionX (IPX) -7.63% to $3.27, Paladin Energy (PDN) -8.28% to $8.42, Silex Systems (SLX) -4.46% to $4.73 and Deep Yellow (DYL) -5.75% to $1.32 extended recent losses.

- Lithium stocks also weakened as spodumene prices retreated from their May peak. Morgans said the sell-off had restored some valuation support, upgrading Pilbara Minerals to Hold and Liontown to Accumulate, with Liontown its preferred exposure. PLS Group (PLS) -3.13%, Liontown Resources (LTR) -4.66% and IGO Ltd (IGO) -3.34% finished lower.

- Mesoblast (MSB) -11.91% to $2.44 reversed sharply after being one of the market’s strongest performers earlier in the week.

- 4DMedical (4DX) -15.57% to $3.20 fell despite proposed US legislation directing the Department of Veterans Affairs to establish a pilot program using its lung-imaging technology, suggesting expectations had already moved well ahead of the announcement.

- Megaport (MP1) -8.48% to $18.23 and DroneShield (DRO) -7.76% to $2.14 were also heavily sold as investors reduced exposure to higher-beta technology and defence names.

- The major banks were mixed. Commonwealth Bank (CBA) -0.78% to $171.78, ANZ Group (ANZ) -0.41% to $36.06 and Westpac (WBC) -0.19% to $36.56 declined, while National Australia Bank (NAB) +0.23% to $39.85 edged higher.

- Brent crude: traded around US$85/bbl, on track for its strongest weekly gain since April as escalating US-Iran hostilities threatened Middle Eastern oil flows.

- Gold: fell below US$4,000/oz and was tracking its largest weekly decline since early June as inflation concerns increased expectations that the Federal Reserve may need to lift rates.

- Iron ore: weakened, adding to pressure across the diversified miners.

- Asian Markets were hit today: China -3%, Hong Kong -2% & Japan -4%

- S&P 500 E-mini futures: -62.50 points / -0.82%

- Dow E-mini futures: -356 points / -0.67%