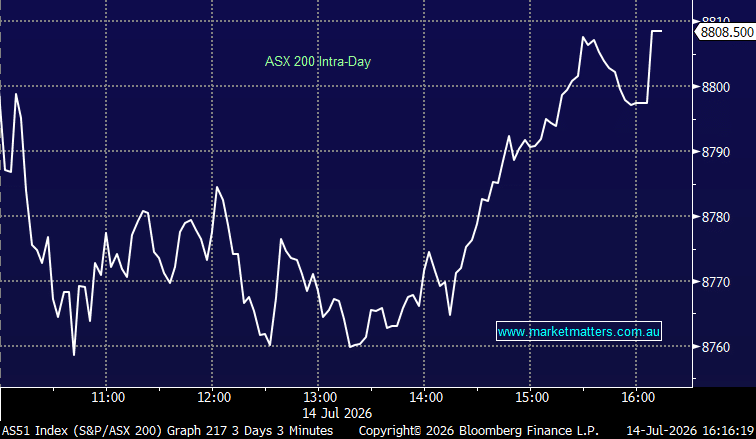

Another session where stocks were hit early before a spirited fightback saw the index little changed, recovering ~50pts from the session low. It certainly seems the market wants to go up; it just can’t get any clear air out of the Middle East. The ASX 200 finished virtually unchanged as weakness in the banks, consumer staples and property stocks was offset by strong gains across energy and materials.

Brent crude traded around US$84.30/barrel, having rallied sharply overnight, while markets moved to price roughly a 50% chance of another US Federal Reserve rate hike this month. Iron ore futures moved back above US$100/t for the first time in a couple of weeks.

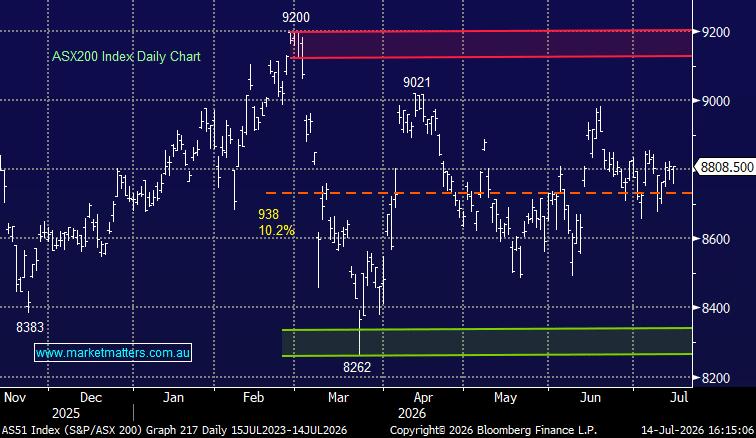

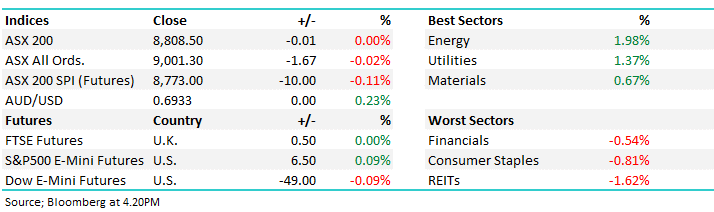

- ASX 200: flat / 0.00% at 8,808.50

- AUD/USD: 0.6933 / +0.23%

- Best sectors: Energy +1.98%, Utilities +1.37%, Materials +0.67%

- Worst sectors: REITs -1.62%, Consumer Staples -0.81%, Financials -0.54%

- Australian consumer sentiment improved in July, with the Westpac-Melbourne Institute index rising 4.1% to 83.9, although confidence remains extremely weak by historical standards. The improvement largely reflected relief that the worst-case outcomes for fuel prices, interest rates and employment had not materialised, helped by lower petrol prices.

- Likewise, Australian business confidence improved for a third straight month in June, with NAB’s confidence index rising 9 points and recovering much of March’s sharp decline. However, confidence remains below both February levels and its long-run average, while business conditions were unchanged at a subdued 3 points.

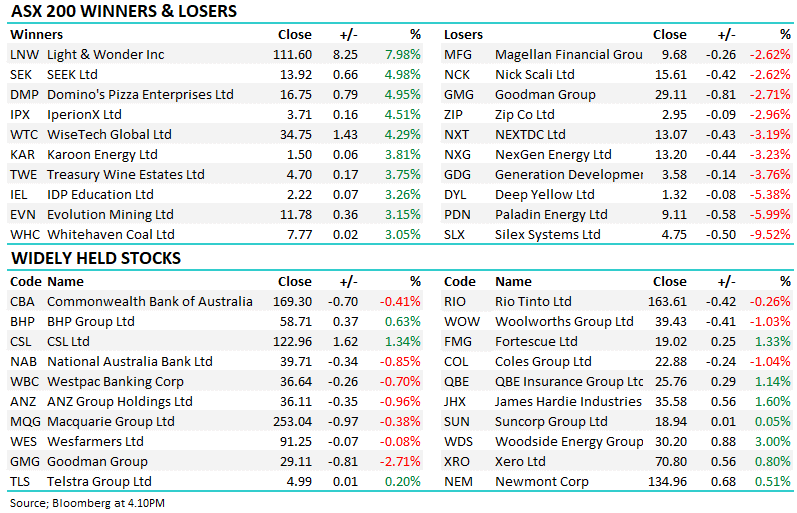

- Light & Wonder (LNW) +7.98% to $111.60 was the standout performer after reaffirming its FY26 guidance. The gaming company remains on track to deliver mid-to-high single-digit EBITDA growth, while management also reiterated its balance-sheet targets despite completing further share buybacks during the quarter. Citi retained its Buy rating and $149 price target, with the update helping ease investor concerns following recent share-price weakness.

- SEEK (SEK) +4.98% to $13.92 rallied strongly as investors returned to selected growth stocks following a difficult period for the employment marketplace. There was no major company-specific announcement driving today’s move.

- Domino’s Pizza Enterprises (DMP) +4.95% to $16.75 bounced almost 5%, extending its recovery from heavily sold-down levels. Investors continue to weigh the potential benefits of restructuring, store rationalisation and cost reductions against a still-challenging operating backdrop.

- IperionX (IPX) +4.51% to $3.71 continued its strong run as investor interest remains elevated around its US titanium production and recycling strategy.

- WiseTech Global (WTC) +4.29% to $34.75 was among the strongest large-cap technology names, rebounding sharply following recent weakness. The move appeared primarily driven by bargain hunting rather than fresh company news.

- Treasury Wine Estates (TWE) +3.75% to $4.70 rallied as buyers returned to the consumer name following a difficult period for the stock. The market continues to assess the outlook for premium wine demand and the performance of its US operations.

- Genesis Minerals (GMD) +2.04% to $6.00 and Vault Minerals (VAU) +1.43% to $4.98 both finished higher after agreeing to a $12.6bn merger, which will create one of Australia’s largest domestic gold producers. The combined group is targeting annual production of around 600,000–700,000 ounces.

- Origin Energy (ORG) +2.15% to $13.07 gained despite agreeing to refund more than $270,000 to over 4,500 customers following an ACCC investigation into its “Ongoing Saver” electricity plan. The average refund is expected to be around $60 per customer, making the financial impact immaterial for the group.

- Magellan Financial Group (MFG) -2.62% to $9.68 remained under pressure alongside weakness across the listed fund managers. GQG Partners (GQG) -2.44% to $1.40, Pinnacle Investment Management (PNI) -1.90% to $17.53 and Netwealth Group (NWL) -2.15% to $24.08 also declined.

- Higher global bond yields weighed on long-duration growth and infrastructure assets. Goodman Group (GMG) -2.71% to $29.11 and NEXTDC (NXT) -3.19% to $13.07

- Uranium-linked names were hit hard, with selling accelerating across the sector. Deep Yellow (DYL) -5.38% to $1.32, Paladin Energy (PDN) -5.99% to $9.11 and Silex Systems (SLX) -9.52% to $4.75

- Brent crude: up 2% to US$85.14/bbl on fresh US strikes targeting Iran’s ability to disrupt Hormuz shipping.

- Gold: Spot last up +0.6% to US$4025.18/oz (recovered partially from overnight weakness)

- Iron ore: up +1.7% to $US100.15/mt

- Asian Markets: China +1%, Hong Kong +0.9% & Japan +0.9%

- S&P 500 E-mini futures (US): +0.04%, Dow E-mini futures (US): -0.2% Nasdaq Futures (US) +0.41%