- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

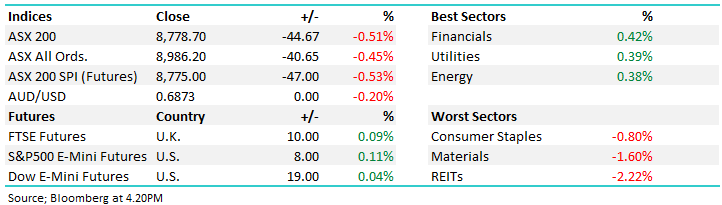

The ASX spent most of the session churning in a relatively tight 20-point trading range, with strength in the banks and technology sector largely offset by another weak day for the miners. The market looked comfortable drifting sideways for much of the afternoon before that balance broke down into the close, with the index accelerating lower in what looked like end-of-financial-year tax-loss selling. There were few buyers willing to absorb the selling pressure, leaving the index to finish well off its intraday highs. Despite the weak close, today’s price action looked more like portfolio positioning than a deterioration in the macro backdrop.

Materials were again the weakest part of the market as gold extended its sharp pullback below US$4,000/oz and iron ore remained under pressure. The major banks helped cushion the index for most of the day, while Technology continued to recover from last week’s selloff.

- ASX 200: 8,778.70 / −44.67pts / −0.51%

- AUD/USD: 0.6873 / −0.20%

- Best sectors: Financials +0.42%, Utilities +0.39%, Energy +0.38%

- Worst sectors: Consumer Staples −0.80%, Materials −1.60%, REITs −2.22%

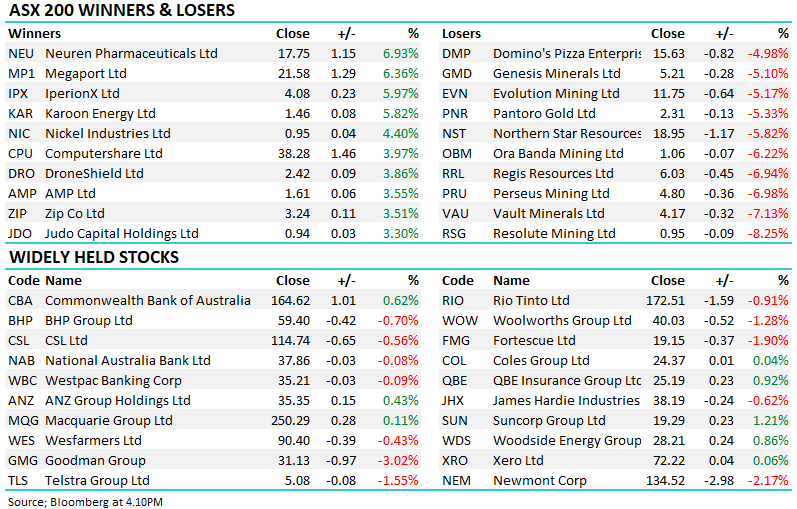

- Neuren Pharmaceuticals (ASX: NEU) +6.93% to $17.75 was once again a top performer, extending yesterday’s 36% rally after Europe’s medicines regulator backed approval of Daybue for Rett syndrome.

- Euroz Hartleys (ASX: EZL) +8% $1.35 rallied after agreeing to sell its Capital Markets business to Bank of Montreal’s BMO Financial Group for $145m in cash, with proceeds expected to be returned to shareholders.

- Collins Foods (ASX: CKF) −2.51% to $8.15 gave back early gains despite delivering a modest earnings beat on domestic strength in the KFC segment, as investors focused on softer early FY27 trading across Germany and the Netherlands, with management declining to provide formal FY27 margin guidance.

- Life360 (ASX: 360) +1.64% to $26.70 continued its recovery, breaking above its 200-day moving average for the first time since December — the stock has now rallied more than 50% from its May lows as buying interest returns to quality technology names.

- HMC Capital (ASX: HMC) −1.33% to $2.97 eased after unveiling Illuma Energy, a new platform combining its renewable energy investments and development assets following the integration of StorEnergy and Neoen’s Victorian portfolio.

- Atlas Arteria (ASX: ALX) +0.20% to $5.10 edged higher after IFM Investors lifted its stake to 55%, increasing pressure on remaining shareholders ahead of the close of its $5.10 per share takeover offer.

- Gold miners endured another difficult session as bullion slipped below US$4,000/oz. Resolute Mining (ASX: RSG) −8.25% to $0.95, Vault Minerals (ASX: VAU) −7.13% to $4.17, Regis Resources (ASX: RRL) −6.94% to $6.03, Ora Banda Mining (ASX: OBM) −6.22% to $1.06 and Evolution Mining (ASX: EVN) −5.17% to $11.75 all posted heavy losses.

- Karoon Energy (ASX: KAR) +5.82% to $1.46 remained in focus after successfully restarting the SPS-92 well at Baúna. While the operational update was positive, brokers remain divided on valuation, with Morgans upgrading to Buy while RBC highlighted higher capital expenditure and free cash flow risks.

- Arafura Rare Earths (ASX: ARU) +4.26% to 24.5c signed another binding rare earths offtake agreement with an Indian industrial group, while confirming construction at Nolans remains on track to commence in September following final financing approvals.

- BHP Group (ASX: BHP) −0.70% to $59.40 and the broader mining sector remained under pressure as investors continued reassessing the outlook for copper prices. Schroders cautioned the AI thematic has driven significant inflows into copper-exposed miners and warned valuations are starting to look stretched.

- Morgan Stanley became the latest broker to cut its oil price forecasts, citing a faster-than-expected reopening of the Strait of Hormuz alongside resilient US production and softer Chinese demand.

- Oil (WTI): ~US$69.90/bbl / +-1.16%

- Gold: ~US$4,012/oz / −0.1%

- Iron Ore: ~US$98.70/mt / −0.1%

- Asian Markets: China +0.1%, Hong Kong -0.85%, Nikkei +0.9%

- Global Futures: FTSE +0.09%, S&P 500 E-Mini +0.11%, Dow E-Mini +0.04%