- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

The ASX shook off a weak start to finish firmly higher today, extending its recent recovery as investors continued rotating out of energy and into resources, financials and growth exposures. The market opened lower before steadily improving through the session, with buying increasing into the afternoon as optimism around US-Iran agreements accelerated with a proper framework and further details of the deal expected imminently.

Materials again did the heavy lifting, with gold miners surging for a fourth consecutive session and BHP trading at fresh record highs. Technology and Healthcare also found support, while Energy was comfortably the weakest sector as Brent crude slid to a three-month low, extending its sharp decline.

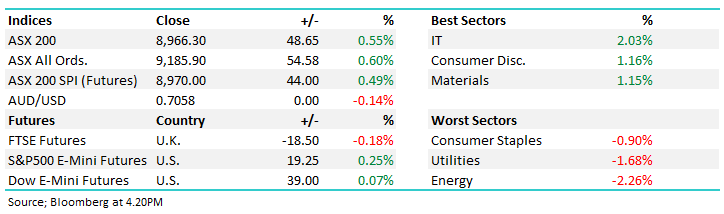

- ASX 200: 8,966.30 / +48.65pts / +0.55%

- AUD/USD: 0.7058 / −0.14%

- Best sectors: IT +2.03%, Consumer Disc. +1.16%, Materials +1.15%

- Worst sectors: Consumer Staples −0.90%, Utilities −1.68%, Energy −2.26%

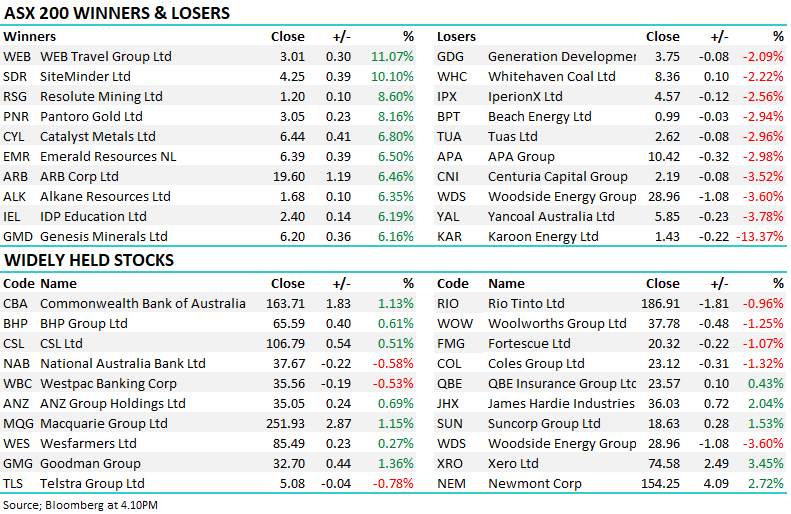

- BHP (ASX: BHP) +0.61% to $65.59 traded at fresh all-time highs, helping drive another strong session for Materials despite iron ore falling below US$100/t amid concerns around Simandou supply growth and softer Chinese steel production.

- Gold stocks continued their remarkable rebound, with Pantoro Gold (ASX: PNR) +8.16% to $3.05, Genesis Minerals (ASX: GMD) +6.16% to $6.20, Resolute Mining (ASX: RSG) +8.60% to $1.20 and Newmont (ASX: NEM) +2.72% to $154.25 all higher. The All Ords Gold Index has now rallied more than 20% in four sessions.

- Travel stocks enjoyed one of the strongest sessions on the market after the Federal Government removed “do not travel” warnings for several Middle Eastern countries — Web Travel Group (ASX: WEB) +11.07% to $3.01 and Qantas Airways (ASX: QAN) +0.20% to $9.98 both rallied strongly.

- Investors looked through a profit downgrade from Flight Centre Travel Group (ASX: FLT) +5.33% to $12.44, instead focusing on the Federal Government’s restriction removal and a new $200m buyback.

- Sims (ASX: SGM) +1.77% to $29.96 rallied after upgrading FY26 underlying EBIT guidance to $420–435m, up from $350–400m, citing stronger North American metals markets and ongoing data centre demand through Sims Lifecycle Services.

- A well-received acquisition helped Symal Group (ASX: SYL) +8.15% to $2.92 higher after agreeing to acquire Queensland-based contractor Shamrock Civil expanding Symal’s exposure to defence infrastructure, expected to be earnings accretive in FY26.

- ARN Media (ASX: A1N) +30.95% to 27.5c after settling legal proceedings with former broadcaster Kyle Sandilands. The agreement includes a cash payment of $12.1m and a revenue-sharing arrangement linked to Sandilands’ future ventures.

- Macquarie Group (ASX: MQG) +1.15% to $251.93 traded above $250 for the first time, closing at a fresh record high as Financials continued their recent recovery.

- The banks extended their recent run, with Commonwealth Bank of Australia (ASX: CBA) +1.13% to $163.71, ANZ Group Holdings (ASX: ANZ) +0.69% to $35.05 and Westpac Banking Corp (ASX: WBC) −0.53% to $35.56 mixed as Financials notched a fourth straight positive session overall.

- Karoon Energy (ASX: KAR) −13.37% to $1.43 remained under heavy pressure following yesterday’s production downgrade, taking losses to around 30% in recent sessions as concerns grow around the delayed restoration of production at Who Dat.

- Energy names were sold heavily again as oil prices continued to unwind their recent geopolitical premium. Woodside Energy Group (ASX: WDS) −3.60% to $28.96 fell to its lowest level since February, while Santos (ASX: STO) and Beach Energy (ASX: BPT) −2.94% to $0.99 also weakened.

- Oil (WTI): ~US$76.10/bbl / +0.1%

- Gold: ~US$4,325/oz / -0.1%

- Iron Ore: ~US$99.60/mt / −1.6%

- Asian Markets: China flat, Hong Kong −0.9%, Nikkei +1.1%

- Global Futures: FTSE −0.18%, S&P 500 E-Mini +0.25%, Dow E-Mini +0.07%