- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

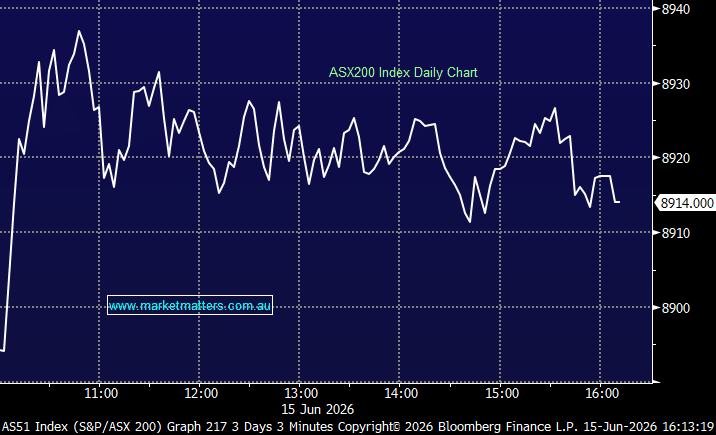

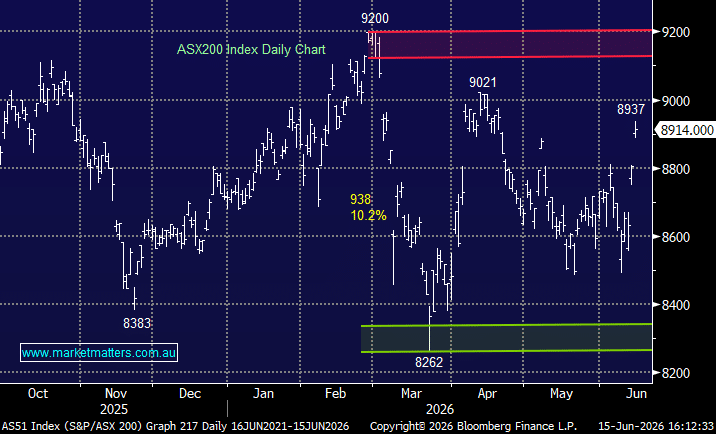

The ASX built on Friday’s strength and rallied again today, with the local bourse embracing news of a US-Iran agreement to reopen the Strait of Hormuz and removing the biggest macro risk hanging over markets in recent months.

The rally was broad, but Materials did the heavy lifting. Copper, gold and bulk commodity names all moved higher as the market focused back towards improving demand expectations, particularly around AI infrastructure and electrification. At the same time, lower energy prices helped ease fears around inflation pressures moving forward, highlighted by the move lower in bond yields. Just a week ago the market was rotating to supermarkets, utilities and energy stocks as oil surged and conflict dominated headlines. Today those same areas were sold to fund a rotation back into miners, banks and growth exposures.

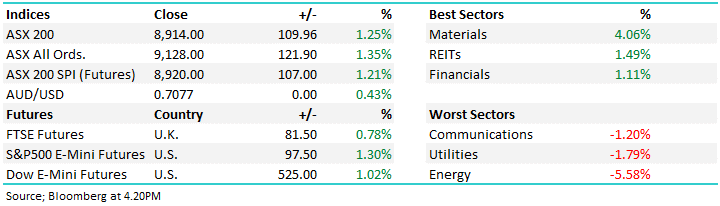

- ASX 200: 8,914.00 / +109.96pts / +1.25%

- AUD/USD: 0.7077 / +0.43%

- Best sectors: Materials +4.06%, REITs +1.49%, Financials +1.11%

- Worst sectors: Communications −1.20%, Utilities −1.79%, Energy −5.58%

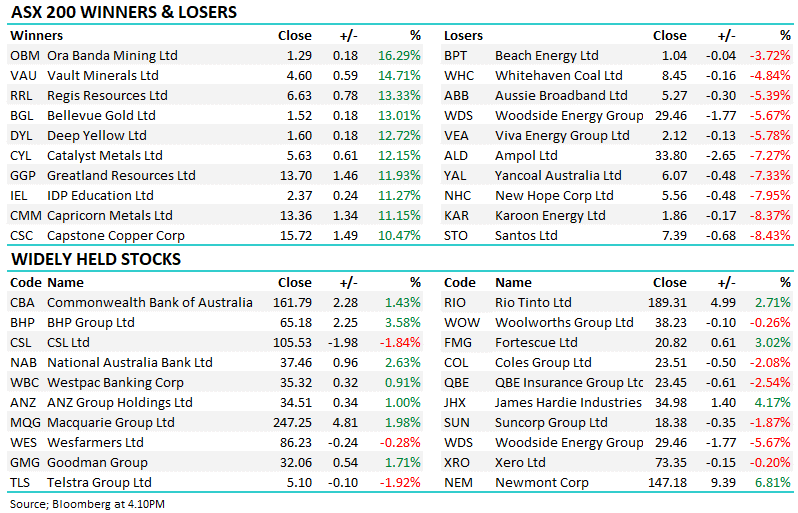

- Gold stocks were back in favour as bullion bounced sharply, with Ora Banda Mining (ASX: OBM) +16.29% to $1.29, Regis Resources (ASX: RRL) +13.33% to $6.63, Bellevue Gold (ASX: BGL) +13.01% to $1.52, Genesis Minerals (ASX: GMD) +8.46% to $5.77 and Newmont (ASX: NEM) +6.81% to $147.18 all enjoying a strong session.

- Vault Minerals (ASX: VAU) +14.71% to $4.60 surged after throwing in a production upgrade on an already strong day for gold stocks, now guiding to 332,000–360,000 ounces in FY27.

- Copper names also found buyers after the metal rallied with the US-Iran agreement supporting global growth expectations — Sandfire Resources (ASX: SFR) +5.24% to $20.87, 29Metals (ASX: 29M) +5.9% and BHP (ASX: BHP) +3.58% to $65.18 were among the beneficiaries, with BHP closing at fresh record highs.

- Deep Yellow (ASX: DYL) +12.72% to $1.60 and Paladin Energy (ASX: PDN) +7.72% to $10.46 jumped as uranium stocks moved higher across the board.

- After walking away from a potential bid for UK pharmacy chain Boots, Sigma Healthcare (ASX: SIG) +6.06% to $2.80 rose with investors welcoming management’s decision to avoid a large and potentially complex offshore acquisition.

- oOh!media (ASX: OML) +7.3% confirmed revised takeover proposals had been received from Pacific Equity Partners, I Squared Capital and Oaktree Capital Management following a due diligence process — not the last we’ll hear of this bidding war!

- ASX Ltd (ASX: ASX) +2.56% to $50.46 gained despite agreeing to a $20.5m penalty to settle ASIC proceedings relating to statements made during the failed CHESS replacement project.

- Southern Cross Electrical Engineering (ASX: SXE) was placed into a trading halt, announcing a $165m capital raising alongside upgraded earnings guidance, lifting FY26 EBITDA expectations and flagging a significant step-up in FY27 earnings driven by strong data centre and infrastructure demand.

- Accent Group (ASX: AX1) +12.6% rallied after Frasers Group launched an unconditional on-market offer, although the board urged shareholders to take no action, arguing the bid materially undervalues the business — the bid is now well below the last traded price.

- Woodside Energy (ASX: WDS) −5.67% to $29.46 was among the weakest large caps as oil prices slumped. The company also denied media speculation regarding a potential transaction involving ExxonMobil.

- The broader energy complex struggled as crude retreated sharply, with Karoon Energy (ASX: KAR) −8.37% to $1.86, Viva Energy (ASX: VEA) −5.78% to $2.12, Santos (ASX: STO) −8.43% to $7.39, Ampol (ASX: ALD) −7.27% to $33.80 and Beach Energy (ASX: BPT) −3.72% to $1.04 all weaker.

- Oil (WTI): ~US$80.60/bbl / -4.9%

- Gold: ~US$4,306/oz / +2%

- Iron Ore: ~US$101.60/mt / flat

- Asian Markets: China +1.8%, Hong Kong +0.5%, Nikkei +4.9

- Global Futures: FTSE +0.78%, S&P 500 E-Mini +1.30%, Dow E-Mini +1.02%