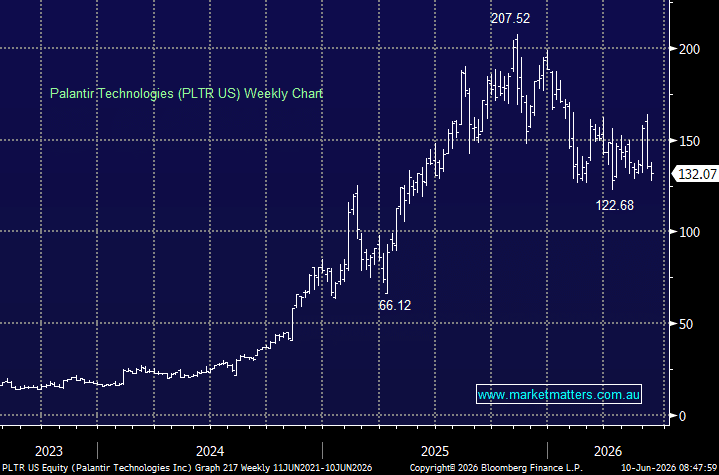

Palantir is one of the purest listed plays on operational AI. In simple terms, it builds software that helps governments and corporates pull together huge, complex and often messy data sets, then turn them into real-time decisions. Historically, it was best known for defence, intelligence and government work, but its commercial business has exploded as companies look to move AI from “experiment” to actual workflow.

It is now a very large company. At a share price of around US$136, Palantir is valued at roughly US$350bn, or more than A$500bn. To put that in an ASX context, it is larger than BHP by market value and more than 10x the size of WiseTech. That is a remarkable valuation for a company still expected to generate less than US$8bn of revenue in FY26.

There are some similarities between Palantir and TechnologyOne (TNE) listed on the ASX. Both are sticky enterprise software businesses selling mission-critical systems to large organisations, particularly government-related customers, and once embedded, they are difficult to remove. TechnologyOne does this through ERP software for councils, universities, government departments and corporates, while Palantir does it through data integration, analytics and AI operating platforms used by governments, defence agencies and large enterprises. However, TNE is a more traditional enterprise SaaS/ERP operator: highly predictable, profitable, founder-led and very well executed, but with a steady growth profile rather than an explosive one. Palantir is a higher-growth AI/data infrastructure platform, with greater upside, far more hype and, importantly, far greater valuation risk.

The valuation for Palantir is predicated on a rate of growth that very few software companies have ever achieved at this scale. Consensus is looking for revenue growth of around 73% in FY26 and another 45% in FY27, while margins and free cash flow are already excellent.

The latest numbers were very strong. Q1 revenue increased 85% year-on-year to US$1.63bn, US government revenue rose 84%, and US commercial revenue surged 133%. The company also raised FY26 revenue guidance to US$7.65–7.66bn, implying around 71% growth for the year. In other words, this is not simply an AI story stock — the numbers are backing up the narrative, at least for now.

Analysts are also broadly positive. Of the 32 analysts covering the stock, around 66% have Buy ratings, 28% are Holds, and only 6% are Sells, with the average 12-month target price around US$189, implying roughly 39% upside from the current price. That said, valuation is the key issue. Based on consensus estimates, Palantir is trading on around 94x FY26 adjusted earnings, 41x FY26 EV/revenue and 71x FY26 EV/EBITDA. Even looking out to FY28, the stock is still on around 45x earnings and 19.5x EV/revenue. These are extreme multiples, and they leave very little room for disappointment.

The debate, therefore, is not really about whether Palantir is a high-quality business — it clearly is. The question is what price investors should pay for that quality. If revenue growth remains above 50%, margins stay elevated, and the commercial AI opportunity continues to compound, the stock can continue to defy traditional valuation logic. However, any slowdown in commercial adoption, moderation in government spending, or broader de-rating of AI/software names would likely hit the stock hard.

- We are very impressed by the business and understand why brokers remain positive, but at current multiples, we would be reluctant to chase it aggressively. We would prefer to wait for volatility or a broader AI/software pullback before becoming more constructive.

MM is neutral PLTR for now, and would get interested ~$US100-110

Add To Hit List