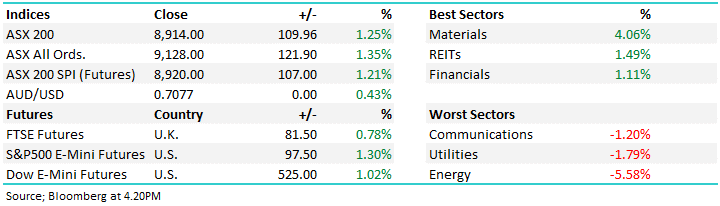

Yesterday, the building stocks caught our attention with Reliance Worldwide (ASX:RWC) and Reece (ASX: REH) rising in a falling market, while James Hardie (ASX: JHX), which we own, slipped 2.4% after announcing it would defend a Class Action in Victoria on 2025 forecasts. The news was no great surprise, but prompted us to consider whether JHX was the best vehicle for exposure to a construction recovery when at least part of their attention may be focused elsewhere.

- Over the last 12-months James Hardie (-23%), Reece (-11%), and Reliance (-24%) have all struggled, but at this stage, only Reliance (RWC) is down in 2026.

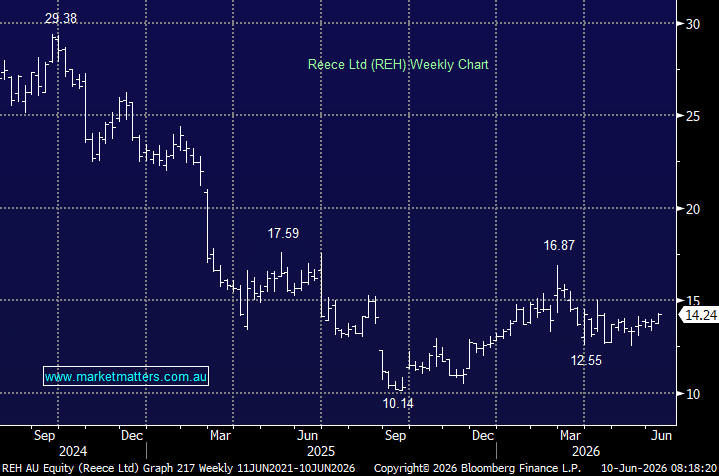

This morning, we briefly compared the three after Barrenjoey upgraded Reece (REH) to Overweight with a $16.50 price target. Broadly, James Hardie (JHX) remains the quality play, Reliance Worldwide (RWC) the more defensive exposure, and Reece the highest-risk, highest-reward recovery story.

If US mortgage rates ease and housing activity recovers into late 2026, REH arguably offers the greatest upside leverage, with its MORSCO footprint providing exposure to the attractive Sun Belt markets. However, Reece remains subscale relative to larger US peers, margins are still under pressure, and the stock is working through the valuation reset of recent years.

- The key catalyst for REH will be evidence that US margins have stabilised. If management can demonstrate that at its FY26 result on the 24th August, the scope for a meaningful re-rating from current levels is substantial.

However, over the last 18 months, all 3 have underperformed the ASX as housing headwinds weighed on the sector:

James Hardie (JHX): Hasn’t recovered from its unpopular $US8.75bn AZTEC takeover in early 2025, which the board pushed through without shareholder consideration. However, it has bounced ~30% from its 2025 low following savage earnings downgrades, and negative interpretations of the huge acquisition – cue the Class Action.

- JHX finally delivered some good news last month with solid 4th quarter earnings, positioning the company to hit $125mn run-rate revenue synergies from the AZTEC acquisition in FY27.

Reliance Worldwide (RWC): Conversely, RWC has endured a steady drip-feed of disappointment over the past 18 months rather than one major profit warning. Guidance was cut in 2025, the anticipated housing recovery has repeatedly been pushed back, margins have come under pressure from tariffs, and recent results have revealed weakness across multiple regions. The good news is that expectations are now low, which can often provide the foundation for future upside when housing activity eventually recovers.

- The repair/maintenance thesis is sound, and they should get tariff relief in FY27, but the market needs to see actual 2H 26 margin recovery before re-rating. The next earnings catalyst is the full-year FY26 result in August.

This hasn’t been a revenue issue; it’s all around margins, with revenue slowly climbing from $1.2bn in FY24 to an estimated $1.3bnn in FY26, but over the same period, the EPS is set to slip ~18%, similar to the decline in the share price. In other words, RWC is “cheap” for a reason, trading ~20% below its long-term average valuation.

- RWC also delivered some good news in April/May, with the company reaffirming guidance, sending the stock up ~9%, albeit off a low base.

Reece (REH): This plumbing business has endured a challenging few years, with increased competition in its mature ANZ operations and a sluggish US construction market weighing on earnings. However, the latest trading update was better than feared, raising the question of whether too much negativity is now reflected in the share price – it’s still trading well below its 5-year valuation. REH is controlled by the Wilson family, who own nearly ~70% of the business through various entities, with CEO Peter Wilson part of the dynasty, i.e. plenty of skin in the game, which MM always likes.

- We agree with Barrenjoey, REH is increasingly looking like a deep-seated turnaround story following its solid 1H result earlier this year – Here.

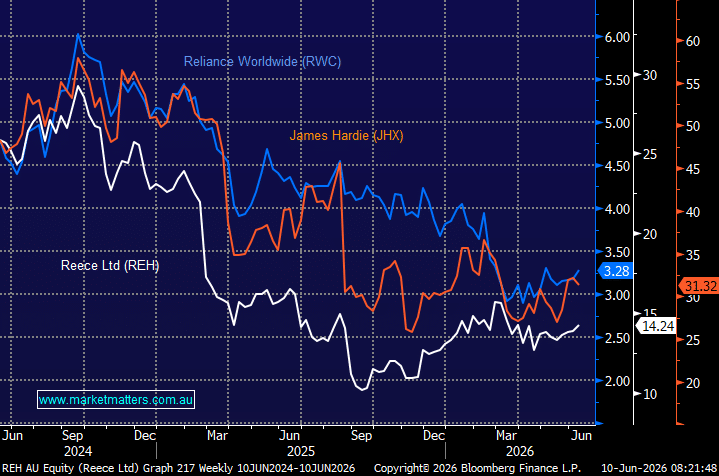

chart

Reece (REH) v James Hardie (JHX) and Reliance Worldwide Corp (RWC)

chart

Reece (REH) v James Hardie (JHX) and Reliance Worldwide Corp (RWC)

Theres a good argument for MM to switch our JHX position into REH, although we like both at current levels for exposure to a turnaround in the US housing market.

- We like the risk/reward towards REH with a test of $17-18 not out of the question in 2026 – we have added REH to our Hitlist.

MM is bullish towards REH around $14

Add To Hit List