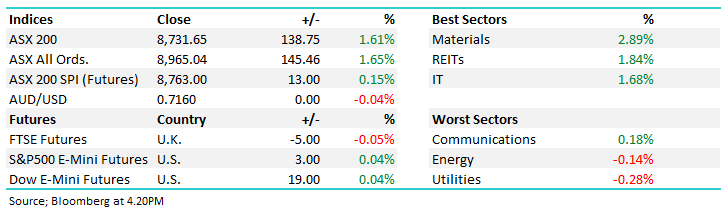

The ASX200 ended the week surging +1.6% higher on Friday, turning around the market’s fortunes to end the week up +0.9%, and up +0.5% for May – a clear demonstration that investors need to look through the volatile noise emanating from the US-Iran War. It was another week of sharp daily swings as markets rode the emotional roller-coaster of the conflict. However, sentiment improved into Friday after reports emerged that the US and Iran had agreed to a tentative 60-day ceasefire extension to allow further negotiations over Tehran’s nuclear program, raising hopes the three-month conflict may finally be moving towards de-escalation.

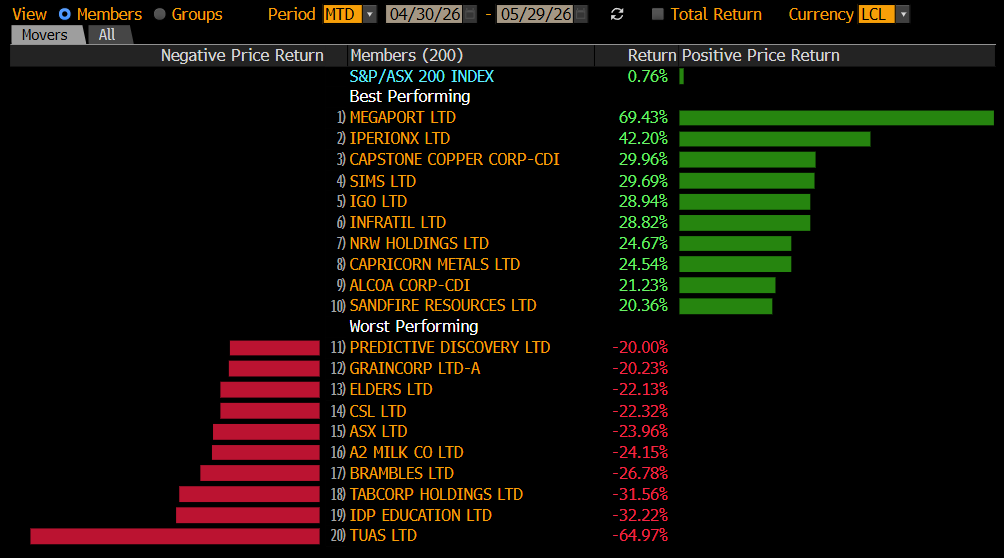

The month of May delivered some significant moves in both the winners’ and losers’ enclosures, with a whopping 8% of the ASX200 moving either up or down by 20% or more, in a month where the underlying index advanced by less than 1%. Moves were largely driven by company-specific news flow, although the Miners were the clear standout on the positive side of the ledger, needing little excuse to rally through the month.

Winners: Megaport (ASX: MP1) +71%, IperionX (ASX: IPX) +40%, Capstone Copper (ASX: CSC) +33%, Sims Ltd (ASX: SGM) +30%, IGO Ltd (ASX: IGO) +27%, Mineral Resources (ASX: MIN) +19%, and BHP Group (ASX: BHP) +16%.

Losers: Tuas Ltd (ASX: TUA) -64%, Tabcorp (ASX: TAH) -31%, IDP Education (ASX: IEL) -30%, Brambles (ASX: BXB) -25%, CSL Ltd (ASX: CSL) -23%, Elders Ltd (ASX: ELD) -22%, ASX Ltd (ASX: ASX) -20%, and GrainCorp (ASX: GNC) -20%.

Weekly snapshot: The main event of the week was Wednesday’s relatively soft local CPI, which reined in bets for further RBA rate hikes through 2026:

- The week commenced quietly as US markets enjoyed the Memorial Day long weekend and no fresh negative news crossed the wires around Iran.

- The markets reversed Monday’s moderate gains as the US hit some strategic Iranian targets, confirming there was no certainty in the volatile US-Iran negotiations.

- On Wednesday, the Australian CPI data offered some relief to escalating fears with the April CPI slowing to 4.2% (vs 4.4% consensus).

- Thursday was another triple-digit down day for May, on worsening tensions in the Middle East – again!

- Friday saw the ASX 200 bounce back strongly, delivering a triple-digit gain, as reports of a tentative 60-day ceasefire extension between the US and Iran sparked a broad risk-on rally.

In the week ahead, markets are likely to remain highly sensitive to developments in the US-Iran conflict, with geopolitical headlines continuing to drive large swings in sentiment across equities, energy and bond markets. Locally, attention will turn to Tuesday’s RBA meeting, where the cash rate is widely expected to remain unchanged at 4.35%, followed by Wednesday’s Q1 GDP release, which could prove pivotal for rate expectations. A weak print would reinforce the view that the economy is slowing sufficiently to keep the RBA on hold, while a strong result would likely reignite concerns that further policy tightening may still be required.

Overseas markets were mixed on Friday night ahead of further war uncertainty over the weekend. In Europe, the EURO STOXX 50 and the UK FTSE retreated by 0.1% and 0.2%, respectively. In the US, the S&P 500 finished enjoying its ninth consecutive weekly gain, closing up +0.2% on Friday, while the small-cap Russell 2000 slipped 0.6%.

- The SPI Futures are calling the ASX200 to open marginally lower on Monday following a soft session by copper overnight.