- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

The ASX traded in two very different halves today, opening weaker as Financials extended yesterday’s selling pressure before a softer-than-expected CPI print sparked a broad rebound across the market. Once the inflation data hit, rate-sensitive sectors quickly caught a bid as traders pared back expectations of another near-term RBA hike, helping the index finish strongly into the close.

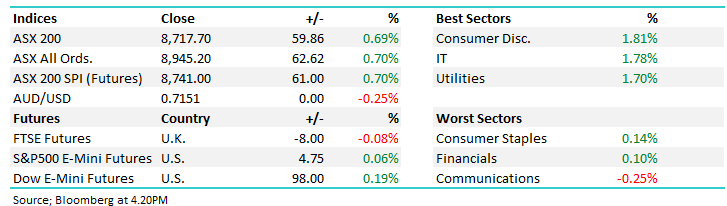

- ASX 200: 8,692 / +34.97pts / +0.40%

- AUD/USD: 0.7167 / +0.56%

- Best sectors: Consumer Disc. +1.81%, IT +1.78%, Utilities +1.70%

- Worst sectors: Consumer Staples +0.14%, Financials +0.10%, Communications −0.25%

- April CPI slowed to 4.2% (vs 4.4% consensus), aided by the government’s temporary fuel excise cut. The RBA’s preferred trimmed mean, however, ticked up to 3.4% from 3.3% in March – though that was inline with expectations.

- Money markets slashed the probability of a June hike from 12% to just 6%.

- Bond yields fell on the news, Aussie 3-year yields down 5.5bps to 4.5% – off around 20bps since recent employment data underwhelmed.

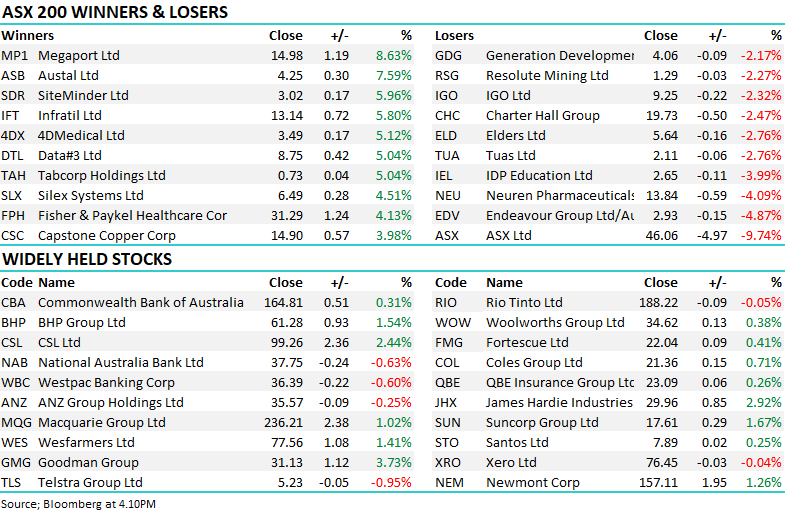

- Consumer Discretionary led the index (+1.81%) as rate relief sentiment flowed through to spending-sensitive names. Premier Investments (ASX: PMV) +3.81%, Nick Scali (ASX: NCK) +3.48%, Harvey Norman (ASX: HVN) +2.47%, JB Hi-Fi (ASX: JBH) +1.18% and Super Retail (ASX: SUL) +2.58% all participated.

- Tech was a strong performer (+1.78%) as rate-sensitive names responded directly to the CPI print and AI momentum in offshore markets continued. Megaport (ASX: MP1) +8.63%, SiteMinder (ASX: SDR) +5.96%, Data#3 (ASX: DTL) +5.04% and NextDC (ASX: NXT) +3.75% all finished strongly.

- Infratil (ASX: IFT) +5.80% — a notable recovery after yesterday’s weakness. Worth watching given the AI infrastructure exposure.

- Banks were the drag on the index, with Financials the second worst sector on the day despite the overall market being up. CBA (ASX: CBA) +0.31%, Bendigo Bank (ASX: BEN) +0.48% were up, while NAB (ASX: NAB) −0.63%, Westpac (ASX: WBC) −0.60% and ANZ (ASX: ANZ) −0.25% weighed. Westpac’s penalty added to the sector’s weight — the Federal Court ordered it to pay $26 million in civil penalties for financial hardship failures following ASIC legal action.

- Goodman Group (ASX: GMG) +3.73% — a strong recovery for the data centre and logistics REIT, aided by both the rate relief and continued AI infrastructure tailwind.

- ASX Ltd (ASX: ASX) −9.74% — a 10-year low, extending Tuesday’s record 13.3% sell-off. The two-day cumulative decline now sits at ~22%. UBS retained Buy (PT $62, cut from $65.20), framing FY27 expense guidance of 18–21% as a “cost rebase complete.” The market disagrees emphatically.

- Endeavour Group (ASX: EDV) −4.87% — announced plans to sell most of its vineyard and winery assets and target $300 million in cost savings as part of a restructure. Asset sales and cost-out programs rarely excite; the market needs evidence of margin recovery.

- Dicker Data (ASX: DDR) +8.64% rallied following a strong AGM trading update showing double-digit revenue growth, margin expansion and accelerating AI-related sales momentum.

- Coal names were stronger again, including Whitehaven Coal (ASX: WHC +2.22%) as supply disruptions in China continued to support metallurgical coal prices.

- Another solid session for the miners with BHP (ASX: BHP +1.54% to $61.28), South32 (ASX: S32 +3.46% to $4.79) while Rio Tinto (ASX: RIO) −0.05% to $188.22, as copper remained near record highs and aluminium pushed to fresh multi-year highs.

- Travel stock Web Travel Group (ASX: WEB +2.10%) gained after delivering a broadly in-line FY26 result, with margins ahead of expectations despite softer trading conditions linked to the Middle East conflict.

- Eagers Automotive (ASX: APE) +1.83%, recovering from a ~12% sell-off early after flagging supply constraints, though demand remains very strong.

- Oil (WTI): ~US$91.94/barrel / −2%

- Gold: US$4,489/oz / -0.4%

- Iron Ore: ~US$105.20/mt

- Asian Markets: China –1.05%, Hong Kong –1.05%, Nikkei –0.2%

- Global Futures: S&P500 E-Mini flat, Dow E-Mini +0.15%, FTSE +0.16%