Following a question a week or so ago on infrastructure ETFs, we have taken a deeper look at the Lazard Global Listed Infrastructure Active ETF, which gives investors access to a concentrated portfolio of global listed infrastructure companies. It is the active ETF version of Lazard’s Global Listed Infrastructure strategy, which has been running since 2005 and now has around A$2.5bn in assets under management.

Infrastructure is often described as a defensive growth asset class, and for good reason. The companies typically own or operate assets that are essential to daily life: electricity networks, toll roads, airports, rail assets, water utilities, pipelines and communications infrastructure. The appeal is that many of these assets have long lives, high barriers to entry and revenues linked to regulation, contracts or inflation.

GIFL is not a passive index-tracking ETF. Lazard runs it as an actively managed, benchmark-unaware portfolio, generally holding 25 to 50 securities. The focus is on companies that own physical infrastructure, or concessions and long-term contracts linked to infrastructure, with assets predominantly located in OECD countries. The fund also substantially hedges foreign currency exposure back to the Australian dollar, which reduces the impact of currency moves for Australian investors.

The fund’s objective is to deliver total returns, including income and capital growth, that exceed Australian CPI by 5% per annum over rolling five-year periods, before fees and taxes. That makes it more of a real-return, inflation-aware strategy than a simple yield product. The fee is higher than a broad passive ETF, which is expected given the active approach. The current management fee and costs are estimated at 0.98% p.a., with no performance fee.

Why are we considering it for the Income Portfolio?

The attraction of GIFL is that it provides exposure to a global universe of infrastructure assets that are difficult to access directly. For Australian investors, it can also help diversify away from the local equity market, which is heavily weighted to banks and resources.

The strategy should appeal to investors looking for:

- Exposure to essential-service assets with relatively predictable earnings.

- A potential inflation hedge, given many infrastructure revenues have explicit or implicit inflation linkage.

- Lower volatility than broader global equities over time.

- A more defensive allocation that still has growth and income characteristics.

- Active management in a sector where asset quality and valuation discipline matter.

The ETF still invests in listed equities, so it is not immune from share market volatility. Infrastructure stocks can be sensitive to bond yields and interest rates, particularly when investors compare their yields with fixed income. Regulatory risk is also important, especially for utilities, toll roads, airports and other monopoly-style assets. The fund is concentrated, so stock selection matters.

- We think GIFL is a useful way to access global infrastructure through an experienced manager with a long track record in the asset class, generating a ~5% (unfranked) yield. We like the defensive characteristics of listed infrastructure, particularly in an environment where inflation may remain stickier for longer, plus portfolio diversification is important.

We do already own two high quality infrastructure stocks directly in the Income Portfolio – notably, APA Group (APA) and Dalrymple Bay Infrastructure (DBI) and we remain positive on both. When considering GIFL, the key trade-off is cost. At 0.98% p.a., GIFL is not cheap compared to going direct or investing via a passive infrastructure ETF, but investors are paying for Lazard’s active process, valuation discipline and narrower definition of what qualifies as “preferred” infrastructure.

- For those wanting a more curated exposure to global infrastructure rather than simply buying the index, GIFL is definitely a credible option.

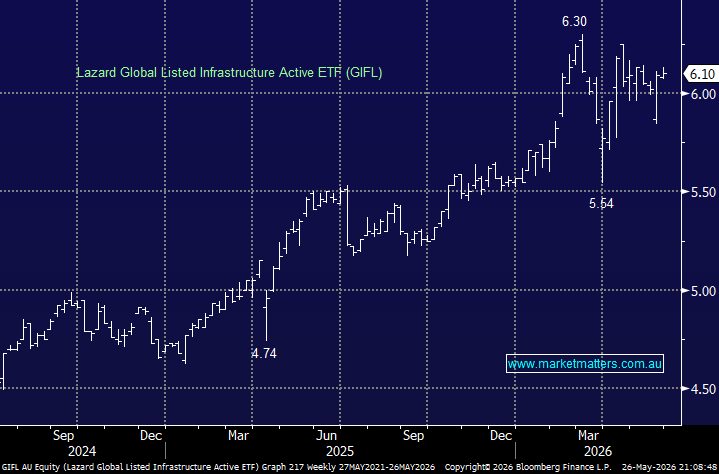

MM is bullish on GIFL

Add To Hit List

chart

Lazard Global Listed Infrastructure Active ETF (GIFL)

chart

Lazard Global Listed Infrastructure Active ETF (GIFL)