Fisher & Paykel Healthcare, the New Zealand-based respiratory and sleep-care device maker, rallied more than +9% on Tuesday after delivering a strong result and reasonable outlook – nothing spectacular, but it was certainly embraced by the market.

- Operating revenue NZ2.31bn, +14% YoY, estimates NZ2.3bn.

- Net Income of NZ$468.5mn, +24% YoY, in line with estimates of NZ$467.2mn.

- Final dividend of 33 NZ cents v 24 NZ cents, up +38% YoY.

Their 2027 forecast was ok, but the market seemed happy with the underlying direction:

- FPH sees net income of NZ500-550mn, estimates were at NZ$538.1mn – up +12% YoY at the mid-point

- Anticipates operating revenue of NZ2.45-2.57bn, estimates were at NZ$2.56bn - up +9% YoY at the mid-point

Gross margin improved, reflecting continued benefits from the company’s operational efficiency initiatives, despite absorbing an estimated ~90 basis point impact from US tariffs on hospital products sourced from New Zealand. Looking ahead, management still expects overall gross margin expansion in FY27, even after factoring in an estimated ~50 basis point headwind from US tariffs and disruption linked to the Middle East conflict. In other words, FPH is successfully evolving from the headwinds the Trump administration has thrown at it. As we said before, this was a good result, with investors appearing to focus on the lack of negative surprises, supported potentially by this week’s contrarian call from UBS to increase healthcare exposure from todays depressed levels.

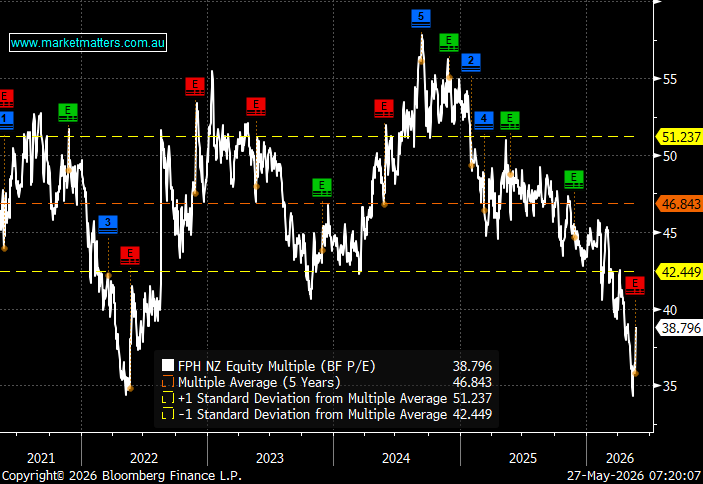

- One supportive factor for the FPH share price is its valuation, with it trading more than 1-standard deviation below its 5-year average, cheap in our minds for a company delivering steady growth in the face of adversity.

chart

Fisher & Paykel Healthcare Corp (FPH) valuation – source Bloomberg

chart

Fisher & Paykel Healthcare Corp (FPH) valuation – source Bloomberg

With almost 10% of adults projected to be on GLP-1 weight loss drugs, in Australia and the US, by 2030 the impact on FPH’s earnings is clearly important. The GLP-1 boom is surprisingly a near-to-medium term tailwind for FPH, not the headwind many expected. However, the long-term question of whether a slimmer population needs fewer CPAP machines is a genuine 10-year thesis to monitor, but it’s nowhere near the earnings numbers right now. Today’s reality is that the estimated 15-20 million Americans on GLP-1 drugs are generating more hospital interactions, more airway management requirements, and more sleep apnoea diagnoses, helping FPH sell product.

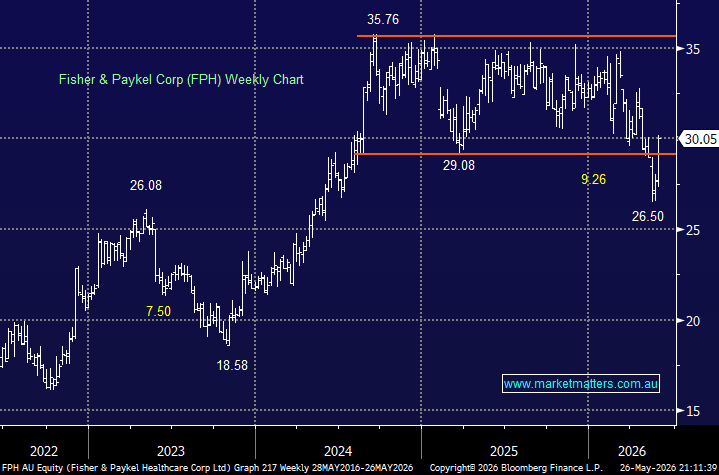

- We are bullish towards Fisher & Paykel, targeting new highs through 2026, at least +20% higher.

MM is bullish towards FPH around $30

Add To Hit List