- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

The ASX edged higher to close out a mildly positive week, helped by improving reports on the Middle East and softening expectations for Australian interest rates. Miners and Energy stocks led the line today, though it’s been a particularly volatile week, with several triple digit moves, even though we’ve ended only +0.3% above where we started.

- ASX 200: 8,657.00 / +35.26pts / +0.41%

- AUD/USD: 0.7139 — down 0.2% on the day

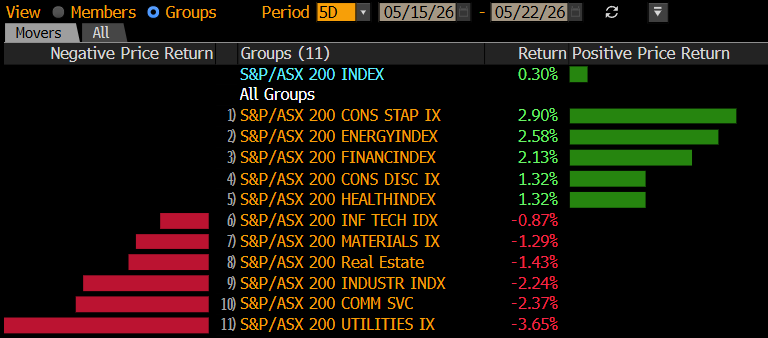

- Best sectors: Materials +1.27%, Energy +1.01%, Industrials +0.51%

- Worst sectors: Communications −1.86%, Utilities −1.09%, REITs −0.93%

- Oil rebounded — Brent crude back to ~$US105/bbl (+2%) after three days of declines.

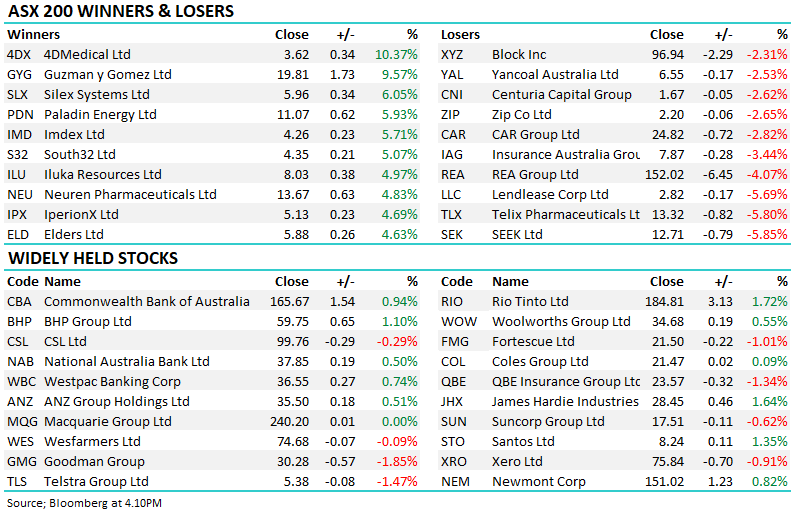

- Materials led — BHP (ASX:BHP) +1.10% to $59.75, Rio Tinto (ASX:RIO) +1.72% to $184.81 and South32 (ASX:S32) +5.07% to $4.35

- UBS upgraded its copper price forecasts — driving a wave of broker upgrades across the sector; Sandfire (ASX:SFR) +3.50% raised to Neutral at UBS with a $20 price target on copper exposure; Evolution Mining (ASX:EVN) +3.14% raised to Buy at UBS with a $14 price target as the gold/copper miner benefits from both the rate narrative and the commodity upgrade.

- Paladin Energy (ASX:PDN) +5.93% to $11.07 — Macquarie upgraded to Outperform with a $13.25 price target; uranium names broadly finding buyers as the energy security narrative strengthens alongside the Iran conflict; Boss Energy (ASX:BOE) also raised to Neutral at Macquarie with a $1.30 price target

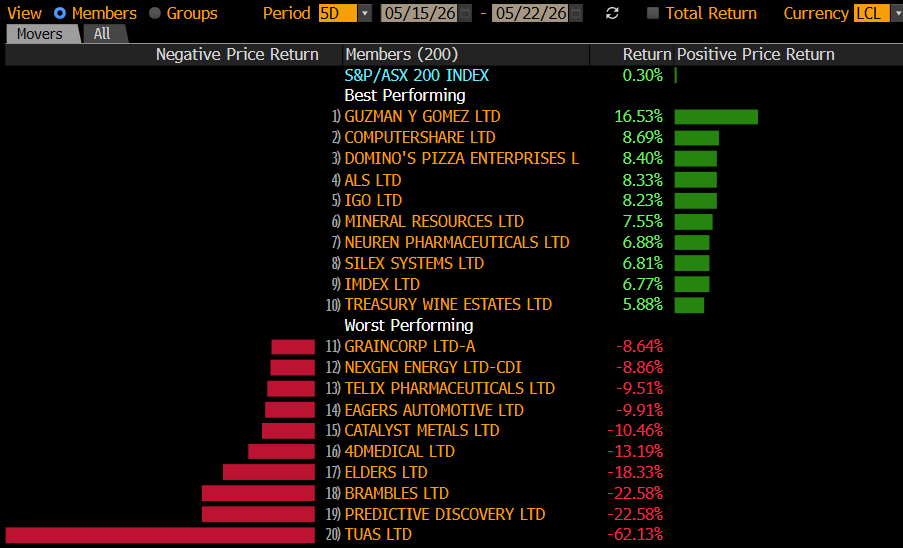

- Guzman y Gomez (ASX:GYG) +9.57% to $19.81 — rocketed after announcing the immediate exit from the US market, closing Chicago restaurants after failing to meet financial performance hurdles. One-off exit cost of $US30-40m but FY26 dividend unaffected. ECP Asset Management backed the call — “what’s left is a simpler, healthier business with the US distraction gone.” Stock is now up ~25% for the week.

- Insurance Australia Group (ASX:IAG) −3.44% to $7.87 — biggest large-cap laggard after Citi warned it could face material claims linked to failed financier Greensill; a significant overhang until the quantum of exposure is clarified

- Banks were mixed to firmer — Commonwealth Bank (ASX:CBA) +0.94% to $165.67, Westpac (ASX:WBC) +0.74% to $36.55, ANZ (ASX:ANZ) +0.51% to $35.50, NAB (ASX:NAB) +0.50% to $37.85

- James Hardie (ASX:JHX) +1.64% to $28.45 — a third consecutive day of gains as investors continued to warm to the full-year result; stock up ~14% over three sessions since the result

- 4DMedical (ASX:4DX) +10.37% to $3.62 — top of the winners board for the day

- Silex Systems (ASX:SLX) +6.05% to $5.96, Paladin Energy (ASX:PDN) +5.93% to $11.07 — uranium names finding buyers

- Tuas (ASX:TUA) flat — terminated its $1.5bn agreement to acquire Singapore-based M1; stock is down ~60% for the week following the Singapore regulator’s investigation into its Simba brand; extraordinary destruction of value in five sessions

- Appen (ASX:APX) +12.5% — reaffirmed 2026 revenue guidance of $270-300m at its annual meeting

- Mayne Pharma (ASX:MYX) +2.8% — won $13.27m in legal fees from US pharma giant Cosette after wrongful cancellation of its proposed acquisition

- Monadelphous (ASX:MND) +2.28% to close firmer after securing ~$120m in new construction and maintenance contracts across mining and renewables, including work with Rio Tinto and Fortescue

- REITs retreated — Goodman Group (ASX:GMG) −1.85% to $30.28, Mirvac (ASX:MGR) −1.17% — gave back some of Thursday’s rate-driven gains as oil’s rebound pushed bond yields slightly higher today.

- Lendlease (ASX:LLC) −5.69% to $2.82, SEEK (ASX:SEK) −5.85% to $12.71, Telix Pharmaceuticals (ASX:TLX) −5.80% to $13.32 — notable large-cap losers

- REA Group (ASX:REA) −4.07% to $152.02 — remains out of favour on concerns around lower listing volume’s, which we think is very valid. We are not fans of REA here.

- Technology One (ASX:TNE) +1.17% — partial recovery after Thursday’s post-results pullback

- Japan CPI — core inflation slowed to 1.4% YoY in April, four-year low; complicates BoJ rate hike timing but policymakers remain wary of broadening price pressures from the Iran energy shock

- Oil: Brent ~$US105/bbl — rebounded after three-day decline.

- Gold: down $US17/oz to $US4526/oz

- Iron Ore: $US106.25/mt – up 0.4% on the day

- Global Futures: S&P 500 E-Mini +0.29%, Dow E-Mini +0.28%, FTSE +0.32%