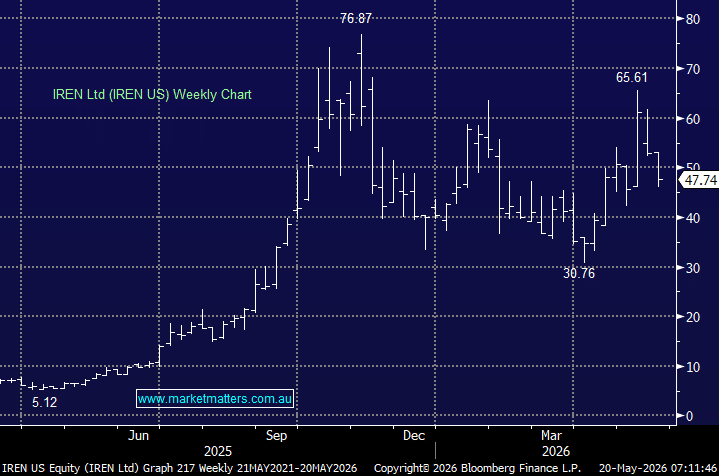

It has been a big couple of weeks for IREN after the company announced a five-year, US$3.4bn AI cloud contract with Nvidia, a deal that materially improves revenue visibility and gives its neocloud strategy a major endorsement. Nvidia has also been granted the right to buy up to 30 million IREN shares at $US70, representing a potential $US2.1bn investment. For a company still transitioning from bitcoin mining toward AI infrastructure, this is a significant validation point.

The deal was announced alongside IREN’s quarterly numbers, which were a lot messier and softer than we had hoped. However, the headline impact of such a large contract with Nvidia understandably overshadowed the weak result.

3Q highlights — released on the 7th of May:

- Fiscal 3Q revenue fell to $US144.8m, down from $US148.1m a year earlier and below expectations of $US219.7m.

- IREN reported an operating loss of $US233.5m, versus an operating profit of $US35.5m a year earlier.

- The weaker result reflected lower bitcoin prices, reduced mining capacity, the retirement of mining hardware ahead of GPU installation, and impairments linked to that retired equipment.

- The company signed a five-year AI cloud contract with Nvidia worth $US3.4bn, covering the deployment of air-cooled Blackwell GPUs within 60MW of existing data centres at Childress.

- Nvidia has a five-year right to purchase up to 30 million ordinary shares at SUS$70, representing a potential investment of up to $US2.1bn.

- IREN said its 2026 expansion to 480MW remains on schedule, with Childress Horizon 1-4 facilities expected online by year-end and already contracted.

- Longer term, IREN is targeting a scale-up to 1,210MW in 2027, with further ramp-up across its Texas and Oklahoma campuses into 2028.

The key point is that this result was not really about the reported quarter. The legacy bitcoin-mining business is being disrupted as IREN reallocates infrastructure toward higher-value GPU cloud workloads. That creates near-term noise in revenue, margins and earnings, but the Nvidia contract shifts investor focus from the messy transition to the potential scale of IREN’s AI infrastructure opportunity.

Nvidia is clearly not just another customer. It is a strategic endorsement from the most important company in the AI ecosystem. For IREN, the deal helps address one of the biggest questions around neocloud operators: can they secure high-quality customers, scarce GPUs and long-duration contracted demand? A five-year Nvidia-backed deal gives IREN materially better visibility into 2028 and strengthens its credibility versus peers.

- For those new to the term, neoclouds are specialist AI infrastructure providers that rent high-performance GPU capacity to customers needing AI compute. They sit between the chip suppliers, such as Nvidia, and traditional hyperscale cloud platforms, such as AWS, Microsoft Azure and Google Cloud. At their core, they are focused more on providing GPU capacity for AI training and inference than offering a full suite of cloud services.

The neocloud opportunity is enormous, but it’s also capital-intensive, execution-heavy and increasingly competitive. The challenge for IREN is to deploy capacity on time, fund the build-out without over-stretching the balance sheet, and prove that strong demand can translate into attractive returns on invested capital. Capex is likely to remain heavy, and free cash flow will likely stay under pressure while the business scales.

Following the Nvidia deal, IREN has a stronger market position, but the share price will now largely depend on how quickly annual recurring revenue builds and whether margins hold as competition intensifies.

- IREN’s latest result was weak at the headline level, but the Nvidia deal is potentially transformational. The company is moving from a more volatile bitcoin-mining model toward contracted AI cloud infrastructure, and Nvidia’s backing materially improves revenue visibility and strategic credibility. The stock is certainly not without risk, and it’s very volatile. However, we think the growth pathway ahead of it justifies a small ~3% position in the International Equities Portfolio.

MM remains long & bullish IREN ~$US48

Add To Hit List