On Monday, Tuas fell around 60% after Singapore’s regulator, IMDA, suspended its review of Simba’s proposed acquisition of M1. The issue is serious because IMDA raised concerns that Simba may have used unauthorised radio frequencies, and the M1 transaction cannot proceed until the investigation is resolved. Soul Patts has meaningful exposure to Tuas, owning 78.7m shares, equal to about 14.6% of Tuas. That is down from the much larger stake, where SOL previously held 116.5m shares / 25% of TUA.

While TUA shares bounced ~20% yesterday, this is a meaningful exposure and net negative for SOL, but not materially so. Mark-to-market, every $1 fall in Tuas reduces the value of SOL’s holding by ~$79m. TUA is down $3.30 from pre-selloff levels, which implies a $260mn pre-tax hit to SOL’s portfolio value.

- In the context of Soul Patts, that is painful, but in the context of their total portfolio worth $13.8bn at 1H26, it’s roughly 1.9% of pre-tax NAV – i.e. not a disaster

While not a good event, it’s a reminder of why we own shares in a diversified investment business. From here, the issue is whether the regulatory problem permanently impairs Tuas’s growth story, which would reduce one of SOL’s more successful emerging-company investments from recent years. If the issue is resolved and the operating licence remains intact, the damage will be short-lived. If the regulator takes a harsher stance, David Teoh’s Tuas could be in for a world of hurt, further impacting SOL.

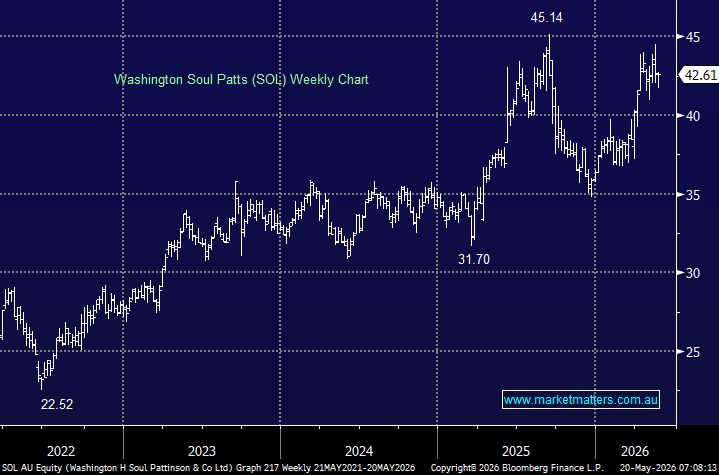

MM remains comfortable holding SOL despite exposure to TUA

Add To Hit List