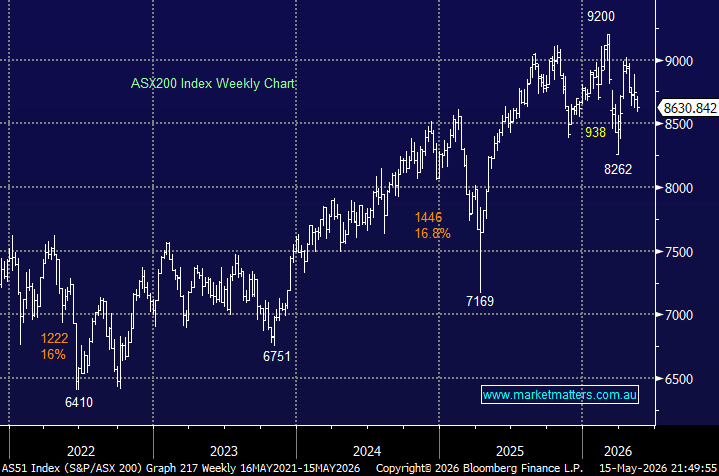

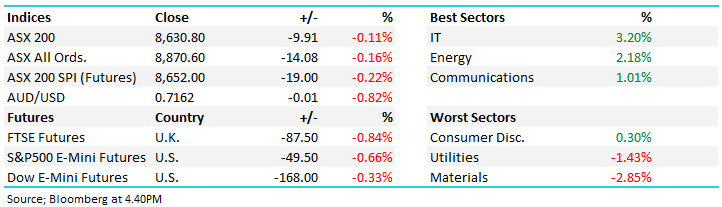

The ASX200 fell 1.3% last week, with market sentiment softened by Tuesday’s Budget and disappointing trading updates from ASX heavyweights CBA and CSL – as the saying goes, the trend’s your friend, with the previous market darling CSL, now down -43%, in 2026. As we all know, the budget played a dominant role last week, with the influential “Big Four Banks” retreating by an average ~6% on fears around Australia’s pivotal housing market. It’s a good job the big miners enjoyed a great week, despite surrendering some of their gains on Friday. BHP Group (ASX: BHP) and RIO Tinto (ASX: RIO) posted fresh all-time highs, both advancing +4% by Friday’s close.

Refreshingly, the winners’ and losers’ enclosures were dominated by earnings updates, both good and bad:

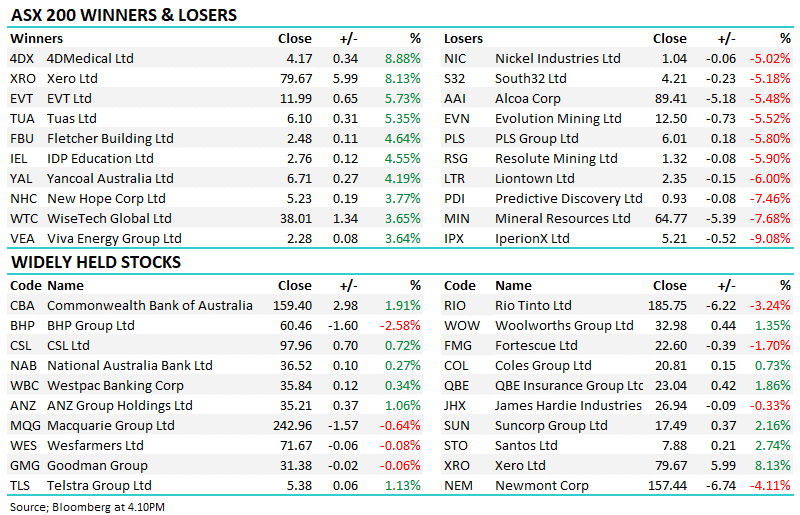

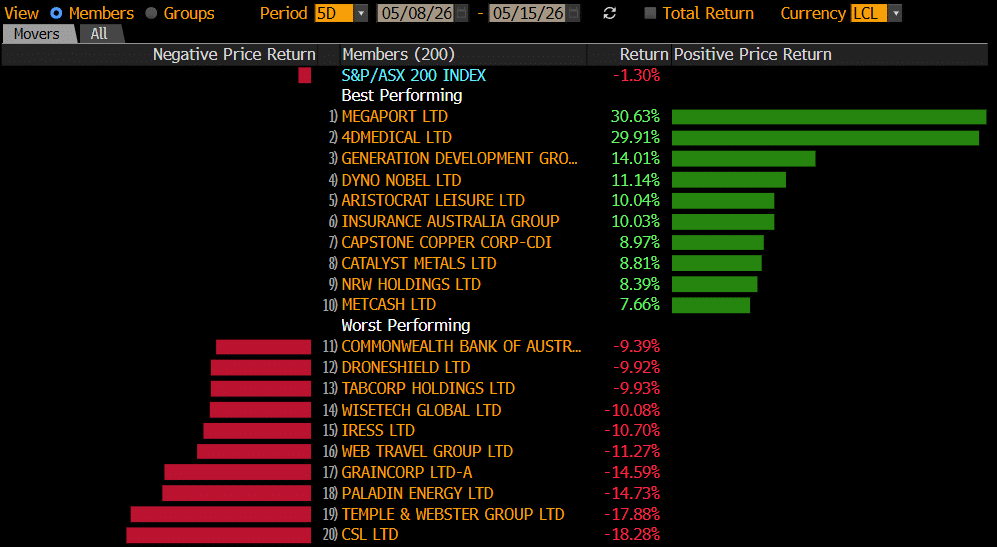

Winners: Megaport Ltd (ASX: MP1) +31%, Generation Development (ASX: GDG) +30%, Dyno Nobel (ASX: DNL) +14%, Aristocrat Leisure (ASX: ALL) +10%, Insurance Australia Group (ASX: IAG) +10%, Capstone Copper (ASX: CSC) +8%, and Metcash (ASX: MTS) +8%.

Losers: CSL Ltd (ASX: CSL) -18%, Temple & Webster (ASX: TPW) -18%, Paladin Energy (ASX: PDN) -15%, GrainCorp (ASX: GNC) -15%, WiseTech Global (ASX: WTC) -10%, Tabcorp (ASX: TAH) -10%, DroneShield (ASX: DRO) -10%, and Commonwealth Bank (ASX: CBA) -9%.

Locally, the budget dominated the news before the baton was passed to US inflation following the hot US PPI on Thursday night:

- Monday set the week’s soft tone after President Trump rejected the latest peace deal from Iran, and healthcare behemoth (just) CSL delivered its 4th downgrade.

- The ASX fell both into and after the Federal Budget as investors found little to cheer in the changes to the likes of CGT and negative gearing, with the banks bearing the brunt of the selling.

- Thursday finally saw the ASX snap a 4-day losing streak, albeit just as banks found support and the heavyweight miners continued to post fresh all-time highs.

- Profit-taking hit the miners on Friday as the $US dollar rallied after the strong US PPI stoked fears around inflation, with more expected on Monday.

- The week closed on the back foot on global bourses with the Dow falling over 500-points as inflation and interest rate fears resurfaced as oil pushed over 3% higher.

Overseas markets retreated on Friday as a selloff in global bonds halted a rally in stocks, with concerns increasing that central banks will be forced to raise rates to keep inflation in check due to persistently elevated oil prices. In Europe, the German DAX tumbled -2.1%, closely followed by the UK FTSE, which ended the session down 1.7%. In the US, the tech-heavy NASDAQ retreated 1.5%, while the more rate-sensitive Russell 2000 fared worse, closing down 2.4%.

- The SPI Futures are calling the ASX200 to open down 0.4% on Monday following the weak session on overseas bourses.