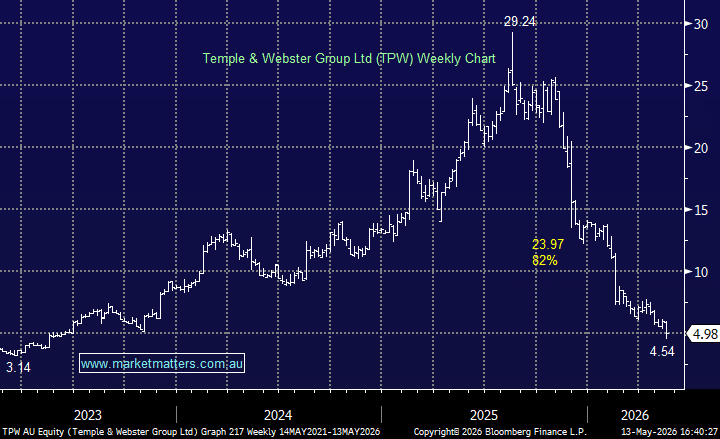

TPW –6.39%: Fell after issuing softer FY26 revenue guidance, with the market reacting negatively to slowing top-line momentum and a clear shift toward profitability over growth.

- FY26 revenue guidance: $665–675m, +11–12% y/y

- FY26 EBITDA guidance: $20–22m, +6–17% y/y

The update suggests management is prioritising margins and cash generation as macro conditions remain difficult, particularly across discretionary retail spending. While growth is stable, revenue outlook came in below expectations and points to softer momentum than the market had priced in.

On a positive note, the company highlighted that current margin run-rates could see FY27 EBITDA almost double to around $40m, even under a lower-growth scenario, suggesting the underlying profitability profile is improving materially, but at the expense of growth.

MM is now neutral on TPW ~$5

Add To Hit List