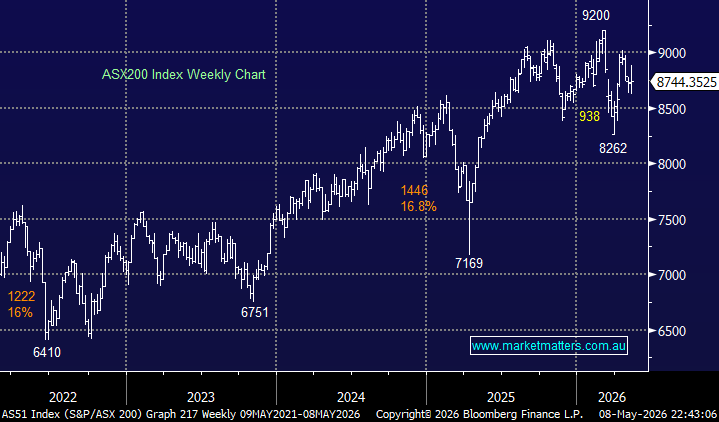

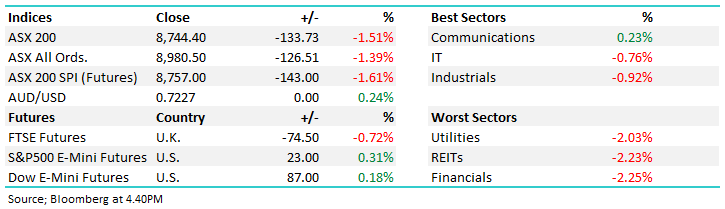

The ASX200 experienced a choppy week, ultimately closing up +0.2% following Fridays triple-digit loss as tensions between the US and Iran took a turn for the worse. The local index was threatening to break out toward fresh highs on Thursday before yesterday’s -1.5% sell-off, leaving the market stuck in the 8600-9000 trading range where it’s now looked comfortable for more than a month. The rate-sensitive stocks continue to weigh on the ASX with retail and real estate continuing to drag the local index back despite the best efforts of the miners which saw the materials sector gain +4.3% through the week, with more set to come on Monday.

- The ASX faces the budget on Tuesday that’s promising “Tax Reform” hopefully when it’s out of the way, the broader market can regain its mojo, we believe it ultimately will.

The winners’ and losers’ enclosures were a mixed bunch with earnings playing a major role while energy names were notably soft as optimism towards the war improved, bar the end of week hiccup. While the miners were the standout performers over the 5-days, the gold stocks in particular enjoyed a strong week as the US dollars “safety bid” lost traction.

Winners: IperionX (ASX:IPX) +26%, Infratil (ASX:IFT) +19%, Capricorn Metals (ASX:CMM) +16%, Greatland Resources (ASX:GGP) +10%, Megaport (MP1) +10%, Pinnacle Investments (ASX:PNI) +9%, NRW Holdings (ASX:NWH) +9%, and IGO Ltd (ASX:IGO) +9%.

Losers: Tabcorp (ASX:TAH) -35%, 4DMedical (ASX:4DX) -20%, IDP Education (ASX:IEL) -14%, Magellan (ASX:MFG) -13%, Yancoal (ASX:YAL) -13%, a2 Milk (ASX:A2M) -10%, Woodside Energy (ASX:WDS) -9%, and New Hope Corp (ASX:NHC) -9%.

The first full week of May was a tale of two markets. US indices surged on the AI build-out, but elsewhere—locally, in Europe, and even the Dow—the tone was far more muted with less influence from tech.

- On Tuesday the RBA hiked rate by 0.25% as largely was anticipated, the market took the 3rd consecutive hike in its stride advancing in the afternoon following the tightening.

- The market delivered a triple-digit gain on Wednesday with the US stepping up efforts to get a resolution with Iran, sending oil down ~2%.

- The ASX extended its advance on Thursday as oil fell sharply igniting the miners led by copper and gold names.

- Friday saw the aggressive sell off as hostilities again escalated between the US and Iran, we, like most subscribers will be glad when this subject fades from MM’s reports.

Overseas markets were mixed on Friday night with performance very different either side of the Atlantic. In Europe, the German DAX fell by -1.3% while the UK FTSE fared better, but it still slipped by -0.4%. In the US it was a very different story with stocks surging to record highs with signs of a strong jobs market demonstrating the US economy remained resilient despite the energy shock from the Iran war, the tech-based NASDAQ surged +2.4% while the broad-based S&P 500 closed up +0.8%.

- The SPI Futures are calling the ASX200 to open down -0.4% on Monday despite the strength on Wall Street and 50c gain by BHP in the US, with the futures keying off weakness across European bourse.