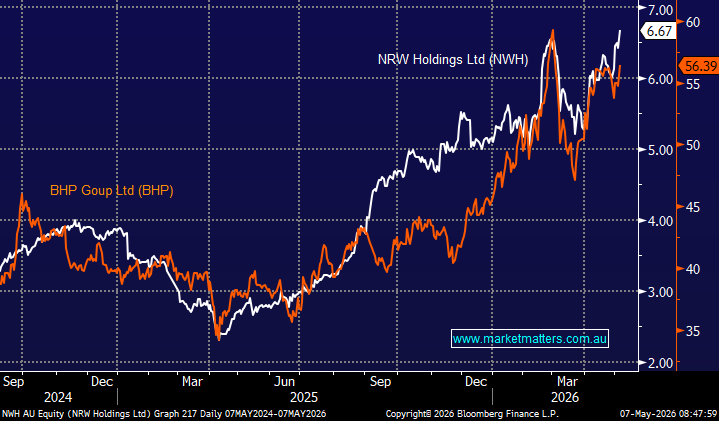

Yesterday was a fascinating session for two ASX200 correlated stocks:

- NRW Holdings (ASX:NWH) which popped over 4% to new all-time highs, extending its 2026 gain to +29%.

- BHP Group, the “Big Australian”, the world’s largest copper (Cu) miner, surged more than +3%, as CFO Vandita Pant talked up Cu demand for AI and global electrification at the Macquarie conference.

The question we asked ourselves following these 2 moves is, where does MM think we are in the miners/ mining services cycle?

Firstly, let’s look at what history tells us:

Miners lead. Mining services follow.

Rising commodity prices lift miners’ margins and confidence, driving investment decisions and capital budgets, which then flow through to contractors. Mining services benefit with a typical 6–18 month lag to earnings.

Implication: Own miners early—they move first and fastest. Rotate into services as the cycle matures, offering a steadier, lagged exposure. Order books and pipelines are key signals – weakening inquiry points to miners quietly pulling back on capex.

On the way down, the sequence reverses. Miners roll first as prices peak, with capex cuts and deferred projects eventually hitting services. Earnings in services often peak late, supported by legacy contracts even as forward work thins.

Implication: Services can look strongest at the top, making them vulnerable to late-cycle disappointment. Watch for “capital discipline” language from miners – it’s typically a precursor to lower spending.

We are seeing no warning signs at the moment. While it varies by commodity, BHP is still planning a meaningful increase in capex, from $9.4bn in FY25 to around $11bn in FY26, in its case for Cu and Potash. At this stage, MM believes we have a confirmation signal, not a leading signal, as NRW makes new highs. For example, NRW’s earnings book is full and high quality, supported by multi-year contracts and, importantly, a deep tender pipeline. This is a classic mid-cycle setup with strong visibility and momentum. Mining services are seeing solid contract flow (confirmation of activity), but not yet the kind of broad-based new project cycle that would signal a true early-cycle surge. The current advance in both miners and their service providers is only 12 months old, and at least a continued advance into Christmas feels likely to MM.

- MM believes we are mid-cycle → with new highs in mining services, a green light, the cycle is here, and momentum is building.

This morning we’ve briefly touched on 2 major mining services stocks, and 2 heavyweight miners we own, paying attention to our upside targets, a question often asked by subscribers.