- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

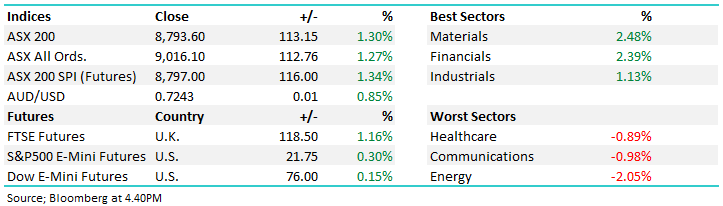

The ASX bounced strongly today, shaking off recent weakness, leaning into improving sentiment around the Middle East, with the Whitehouse now clearly seeking an off-ramp from the Iran conflict. The tone improved as the day wore on, suggesting a degree of confidence returning to the market despite the still-challenging macro backdrop. The heavyweight Materials and Banks drove most of the gains after a few weeks of consistent selling while Energy names dragged as oil prices edged lower. Sentiment is shifting, though the extent of the rally will hinge on whether the Middle East situation continues to de-escalate.

- ASX 200: 8,793.60 / +113.15pts / +1.3%

- AUD/USD: 0.7145 / −0.31%

- Best sectors: Materials +2.48%, Financials +2.39%, Industrials +1.13%

- Worst sectors: Energy -2.05%, Communications -0.98%, Healthcare -0.89%

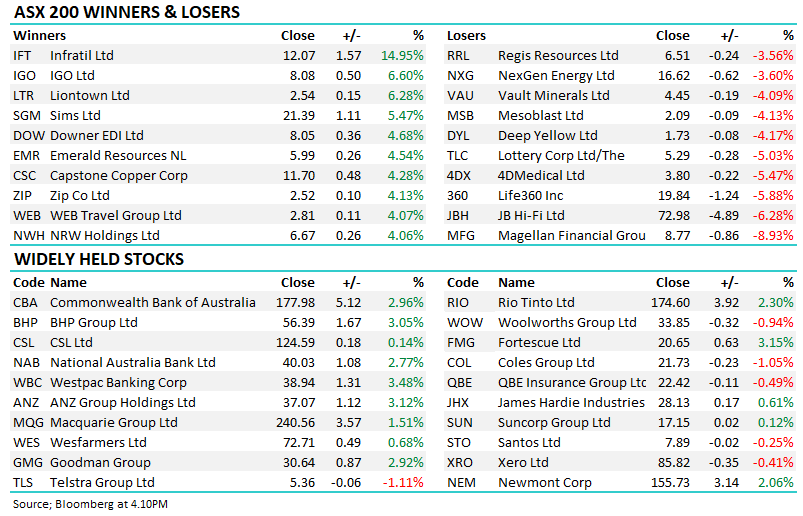

- A sharp reversal for the banks with Commonwealth Bank (ASX: CBA) +2.96%, Westpac (ASX: WBC) +3.48%, ANZ (ASX: ANZ) +3.12% and National Australia Bank (ASX: NAB) +2.77% all rallying strongly, as investors rotated back into the sector following sustained weakness.

- AGL Energy (ASX: AGL) +0.42% edged higher after lifting the lower end of FY26 guidance, driven by stronger thermal generation performance. Not a huge uplift in net terms.

- Atlas Arteria (ASX: ALX) +0.63% saw modest support after rejecting IFM’s takeover bid, saying it materially undervalued the business.

- Energy stocks struggled as oil prices eased, with Woodside Energy (ASX: WDS) −2.66%, Santos (ASX: STO) −0.25% and Ampol (ASX: ALD) −1.24% all finishing lower.

- A big move higher from the data centre thematic, with DigiCo (ASX: DGT) +25% surging after announcing the ~$1bn sale of its Chicago asset, while HMC Capital (ASX: HMC) +17.06% also rallied on its ~20% exposure to the deal alongside a broader strategy reset.

- Regis Resources (ASX: RRL) −3.56% and Vault Minerals (ASX: VAU) −4.09% were both whacked following their merger announcement yesterday.

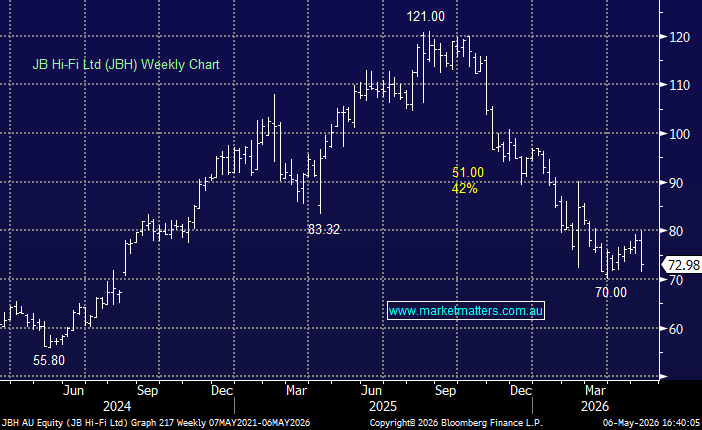

- JB Hi-Fi (ASX: JBH) −6.28% dropped after flagging rising supplier costs and stock shortages driven by data centre demand for certain electrical components.

- Capral (ASX: CAA) +2.66% downgraded FY26 earnings guidance, citing aluminium supply disruption tied to the Middle East conflict, higher LME prices and rising freight costs.

- Oil: trading around $US100.5/barrel (WTI) −1.75%

- Gold: trading around $US4665/oz around our close, +$106/2.36% on the day

- Iron Ore: $110.15/mt / +1.5% for the day

- Asian Markets: China +1%, Hong Kong +1% and the Nikkei +3%.

- Global Futures: S&P 500 E-Mini +0.14%, Dow E-Mini −0.02%, FTSE −1.11%

- US Earnings Tonight: Novonordisk (NVO US), Walt Disney (DIS US), Uber (UBER US), Albemarle (ALB US).