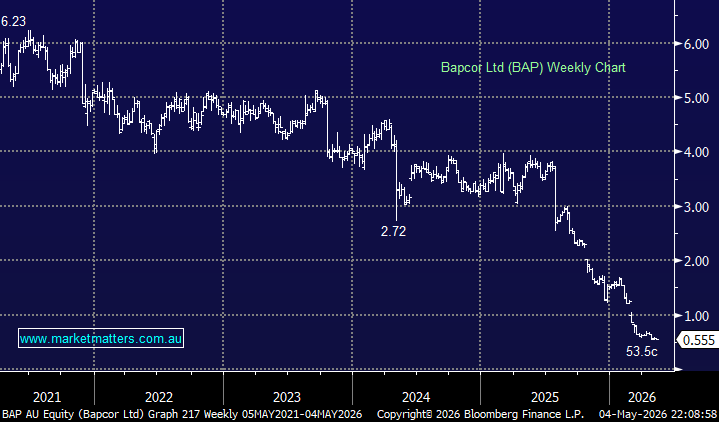

We last discussed Bapcor in December, following another downgrade, Here, at the time when the stock was trading at $1.85, we said: “It’s looking like a value trap rather than a value play until management can prove they’re capable of navigating the increasingly competitive environment.”

The wealth destruction has been huge with BAP, a stock that was trading above $6 after COVID, has plunged ~90% over the last 5 years, as revenue remains around $2bn, but margins have been hammered. There’s definite turnaround potential in the numbers as people continue to shop/use the likes of Autobarn and Midas.

This is a business that attracted a $5.40 private equity bid in early 2024, from Bain Capital, which the board, in its wisdom, rejected. Bapcor owns impressive automotive aftermarket infrastructure, more than 900 locations employing ~5,000 people across Australia and New Zealand, operating under Burson Auto Parts, Autobarn, Autopro, Midas, ABS, and BNT brands. The vehicle aftermarket is a structurally resilient business; cars need parts regardless of the economic cycle, and Bapcor’s network scale is essentially impossible to replicate from scratch. We can see a private equity buyer with operational expertise, exactly the Bain Capital playbook, backing themselves to fix the margin issue.

- Bapcor screens as the classic private equity target: a quality underlying business, a destroyed share price, a discredited board, irreplaceable network assets, and a proven prior bid that demonstrates interest in their model.

MM is cautiously bullish towards BAP around 55c

Add To Hit List